Every year, Weatherly posts an updated Key Financial Data Sheet. While it may appear overwhelming at first glance, it remains one of our most frequently referenced tools as advisors.

In this blog, we provide a fresh look at the 2026 Key Financial Data Sheet and highlight several of the figures that can play an important role in planning this year. As tax laws continue to evolve (including recent changes introduced through the One Big Beautiful Bill) the U.S. tax code has only become more complex. Staying informed on these updates can help investors make more thoughtful decisions.

-

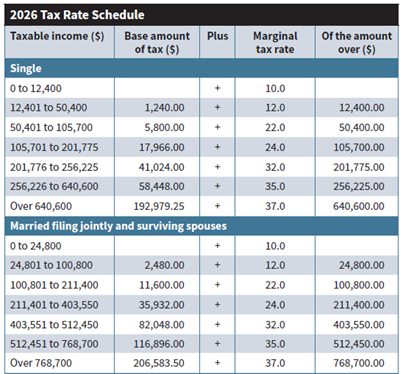

Personal Tax Brackets

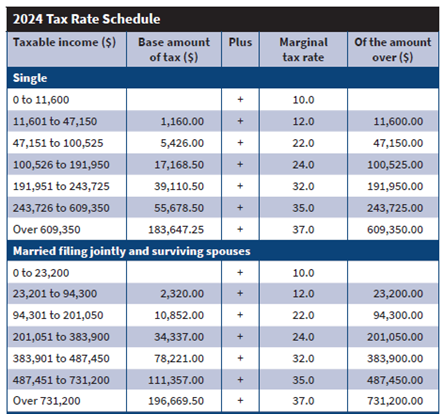

Federal Income Tax Brackets make up the bulk of the annual revenue collected by the IRS each year. Determining your filing status and marginal tax bracket is the first step in tax planning. Majority of taxpayers file as Single or Married Filing Jointly (MFJ).

Source: Key Financial Data Sheet 2026

Individuals who are unmarried, have a qualifying dependent, and pay the majority of household expenses may qualify for the Head of Household (HOH) filing status. This status often provides more favorable tax brackets and deductions compared to filing as Single.

Married Filing Separately (MFS) is another option available to married couples. While many couples choose this status to keep finances separate, others may find tax advantages in doing so depending on their circumstances. Although the tax code generally favors joint filers, there are situations where filing separately may help maximize certain deductions or limit liability.

Strategies to Consider

- Roth Conversion – In years when taxable income is lower than usual, converting funds from a traditional IRA to a Roth IRA may allow you to take advantage of lower tax brackets.

- Engage a Tax Professional – A qualified tax professional can help determine the most appropriate filing status and assist with navigating complex tax planning considerations. Here at Weatherly, we often collaborate with our client’s CPAs to evaluate strategies to help manage taxable income such as splitting tax years and charitable giving.

-

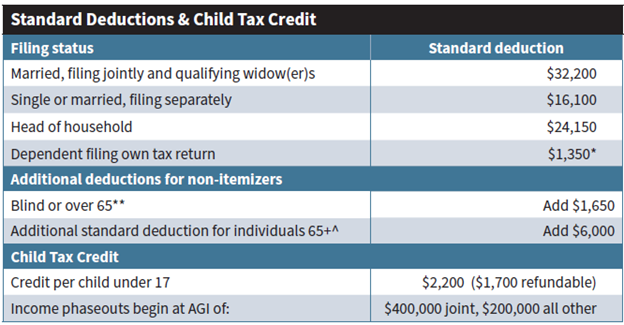

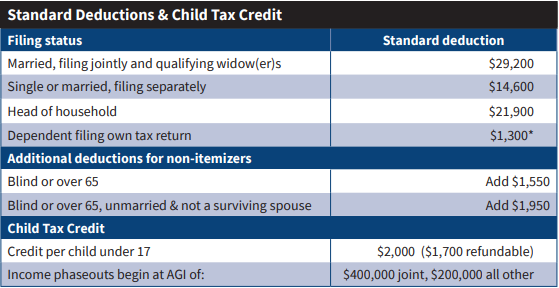

Standard Deductions, Temporary Changes & Child Tax Credits

Each year taxpayers must determine whether to itemize deductions or take the standard deduction. In 2017, The Tax Cuts and Jobs Act nearly doubled the standard deduction and put a limitation of $10K on State and Local Tax (SALT) for those who itemize. Because of this, the majority of American’s have been taking the standard deduction in recent years.

With the 2025 passing of the One Big Beautiful Bill Act, new legislation introduced several temporary changes that may cause more taxpayers to revisit itemizing. One of the most notable updates is the increase to the SALT deduction cap, which has been raised to $40K annually through 2029, subject to income phaseouts.

The bill also includes updates to the Child Tax Credit and introduces an Enhanced Senior Deduction of up to $6,000 for individuals age 65 and older. Similarly, this deduction is scheduled to remain in place through 2028 but phases out at higher income levels.

Source: Key Financial Data Sheet 2026

While many will continue to use the standard deduction, A bunching strategy (particularly around medical expenses and charitable giving) may allow taxpayers to benefit from itemizing in certain years.

Strategies to Consider

- A Donor Advised Fund (DAF) – can be utilized for a tax efficient way to derisk portfolios with flexibility to grant to charities over time. For those itemizing, a tax deduction can also be claimed, but now subject to a 5% AGI Floor.

- Qualified Charitable Distribution (QCD) – may be a great option for those over age 70.5 to give to charity directly from their IRA. The distribution is considered nontaxable and often utilized to help satisfy Required Minimum Distribution (RMD) obligations.

- For those claiming the standard deduction, you can now claim a small deduction for cash gifts directly to qualified 501(c)(3) charities up to $1,000 for single filers or $2,000 for married couples filing jointly.

-

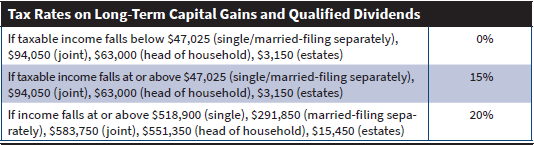

Long-Term Capital Gains and Qualified Dividends

Weatherly’s investment philosophy has an emphasis on long term tax efficiency, particularly within our client’s taxable accounts. Key consideration goes to the federal tax treatment of long-term capital gains and qualified dividends, which generally receive more favorable tax treatment than ordinary income.

For 2026, long-term capital gains tax rates fall between the 0%, 15%, and 20% brackets as shown below based on taxable income.

Source: Key Financial Data Sheet 2026

Strategies to Consider

- Tax Loss Harvesting – As we review and rebalance portfolios throughout the year, we look for opportunities to realize losses that may help offset capital gains. We also review prior year tax returns for any loss carryforwards that can reduce current year gains. For clients in the 15–20% long-term capital gains bracket, this approach can allow us to raise cash for spending needs, reduce concentrated positions, and maintain diversification while helping limit overall tax liability.

- Tax Gain Harvesting – When taxable income falls within the 0% long-term capital gains bracket, investors may be able to sell appreciated assets and realize gains without incurring federal capital gains tax.

-

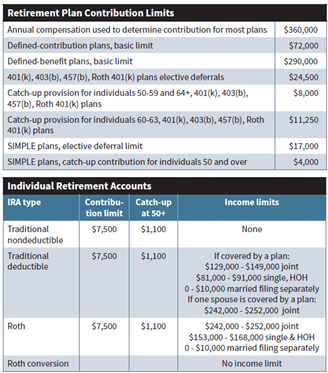

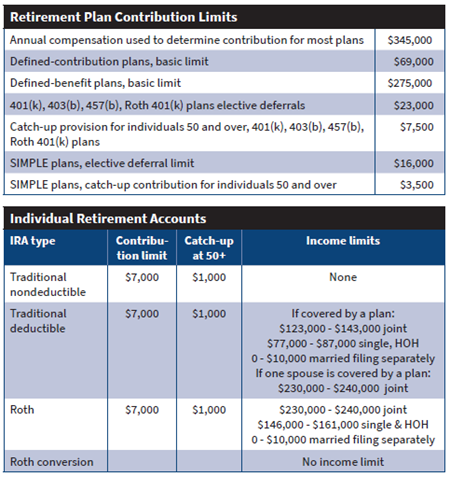

Retirement Contributions

Source: Key Financial Data Sheet 2026

For our clients earning income, strategizing retirement contributions is an effective way to build long term wealth while potentially reducing current taxes. Many taxpayers have access to employer sponsored retirement plans, such as a 401(k), 403(b), or 457 plan. In addition to such plans, individuals may also be eligible to contribute to Traditional or Roth IRAs (depending on their income and other factors).

This time of year, it is important to review annual contribution limits with your advisor to ensure you are taking full advantage of these tax-advantaged opportunities.

Strategies to Consider

- Traditional vs Roth Contributions – For high earners, contributing to a tax deferred retirement plan would allow more money saved given their current high tax bracket. For those in low tax brackets, contributing to a Roth account could limit higher taxes in the future. If you currently have earned income, certain prior year contributions can be made up until the tax return deadlines.

- Self-Employed 401K – Small business owners have an opportunity to significantly increase annual retirement savings through a self-employed 401(k). These accounts allow both employee and employer contributions to maximize retirement contributions year over year. Small differences will go into effect in 2026 for all 401(k) employee contributions- individuals may defer up to $24,500 as the employee, with an additional $8,000 catch-up contribution for those age 50 or older or $11,250 for those 60-63.

-

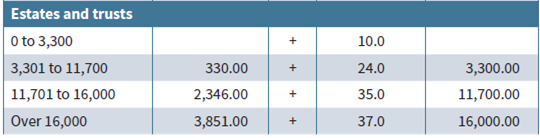

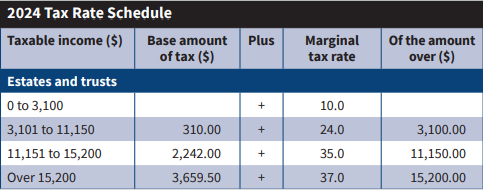

Estates, Trusts and Planning for the Future

Individuals and families often use trusts and estate planning documents as part of a broader strategy to transfer assets to the next generation. While these tools can be powerful, they also introduce additional tax considerations.

It is important to understand how income taxes apply to your specific trusts and estate plan. Certain trusts have compressed tax brackets in comparison to individual tax brackets. In 2026, the top 37% federal tax bracket applies to trusts and estates once income exceeds just $16,000 (vs $768,700 for MFJ in 2026). Intentional planning around trust distributions and asset locations can help reduce unnecessary tax exposure.

Source: Key Financial Data Sheet 2026

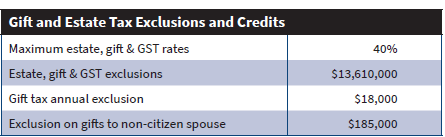

While the above tax brackets are a major factor, it is not the only consideration when it comes to wealth transfer. A question we get often- what is the annual gift tax exclusion amount? For 2026, it is $19,000 (the same amount as 2025). This is how much one person may gift to another person without needing to file a gift tax return (Form 709) and reduce their Lifetime Gift Exclusion Amount ($15M). Annual gifting can be a simple yet effective way to gradually transfer wealth to the next generation while reducing the size of a future taxable estate.

Source: Key Financial Data Sheet 2026

In addition to the annual gifting allowance, individuals also have a lifetime estate and gift tax exemption. For 2026, the federal lifetime exemption is $15 million per person. Recent legislation, including provisions discussed in our blog 10 Ways the OBBBA Could Affect You made significant changes to the estate’s exemption landscape. As tax policy evolves, these thresholds will continue to shift, which makes proactive and ongoing planning an important consideration.

How Weatherly Can Help

Given the complexity of today’s tax code, understanding how these numbers apply to your personal financial situation is important. Here at Weatherly, we are here to support you in the journey by regularly reviewing tax returns and financial information to help identify planning opportunities.

Using the updated 2026 Key Financial Data Sheet, we work with clients to evaluate strategies around taxes, retirement contributions, charitable giving, investment management, and estate planning. By combining this data with ongoing conversations about your goals and circumstances, we can help determine which strategies may be most impactful for you.

With the tax deadline approaching and new changes to estate and tax laws, it is a great time to revisit your financial plan, gifting goals, and overall tax strategy. Please reach out to schedule time with your advisor if you would like to review how the 2026 Key Financial Data Sheet may apply to your financial situation in the year ahead.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

On July 4, 2025, President Trump signed the One Big Beautiful Bill Act (OBBBA) into law just six months before key provisions of the 2017 Tax Cuts and Jobs Act (TCJA) were set to expire. While the bill’s 887 pages include many non-financial provisions, it carries broad implications for taxpayers, making several TCJA-era tax law changes permanent and introducing new rules moving forward.

Due to the quantity and speed with which these tax changes are being rolled out, the IRS is still working to update its tax forms accordingly and will likely release additional guidance on some items over time. In this blog post, we break down the 10 most broadly relevant tax law changes for our client base while acknowledging this blog could have been titled “101 Ways the New OBBBA Could Affect You”.

Many of the new changes have small nuances; pay attention to whether they are: temporary vs permanent, what kicks in for 2025 vs 2026, and whether certain provisions have income phaseouts.

Three 2017 TCJA Changes The OBBBA Made Permanent With Tweaks

1. Extended Standard Deduction

- Permanent

- 2025+

Taxpayers will receive a boost in the standard deduction across all filing statuses starting in 2025. The chart below outlines the new, increased amounts from the OBBBA in comparison to the previously anticipated TCJA limits for 2025.

Refer to the recently updated 2025 Key Financial Data Chart for more information.

Additional Source Material

What this means for you? With a higher standard deduction in place, the hurdle to benefit from itemizing deductions becomes even greater than in previous years. We’re evaluating strategies that allow clients to group itemized deductions, such as bunching charitable donations into a single tax year, to maximize itemized deductions.

2. Estate (& Gift/GST) Tax Exclusion

- Permanent

- 2026+

Beginning in 2026, the new tax law changes will make the estate exemption permanent and increase the base exclusion to $15,000,000 per individual, with annual inflation adjustments starting in 2027. The generation-skipping transfer (GST) and gift tax exemption will also match the updated estate exclusion.

Additional Source Material

What this means for you? Without the OBBBA, the federal estate tax exemption would have reverted back to nearly half (~$7M) beginning in 2026. Creating an urgency for high net worth individuals to use their exemption before it expired. Starting in 2026, married couples will be able to transfer up to $30,000,000 free of estate and gift tax, which significantly extends planning flexibility. This change reduces near term estate tax exposure for many clients and allows for thoughtful multi-generational planning with the understanding future legislation can always shift the landscape. We’ll continue monitoring updates and encourage clients to review their estate plans in light of these new thresholds.

3. Tax Brackets

- Permanent

- 2026+

The TCJA-era tax brackets have been made permanent with some slight adjustments starting in 2026. The 10% and 12% brackets will expand modestly, providing relief to lower and middle income earners with the 22% bracket narrowing to offset those changes.

What this means for you? Since the US has a progressive tax system, the overall dollar impact of these adjustments will be somewhat diluted. Although it is interesting to note, for the first time next year it is expected the 12% tax bracket for married couples filing jointly could reach six figures.

Five OBBBA Changes with Income Phase Outs

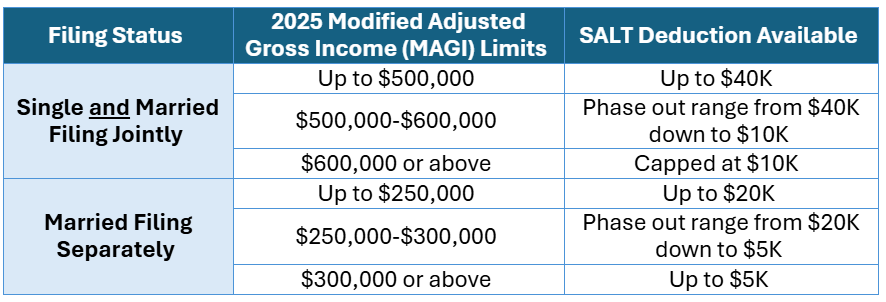

4. State and Local Tax (SALT) Deduction

- Temporary

- 2025-2029

- MAGI Phase Outs

One of the headline provisions in OBBBA is the temporary expansion of the SALT deduction limit. From 2025 through 2029, the cap increases significantly from $10K to $40K (with a 1% annual inflation adjustment). Based on current law, the SALT will revert back to the $10K limit in 2030. We anticipate this provision will impact our clients who live in high tax states and whose sales or property taxes were previously capped at $10K.

Refer to the chart below for 2025 MAGI limits for eligibility.

For additional resources on the SALT Deduction.

Additional Source Material

What this means for you? High earners should be cautious of the steep phaseout, which can quickly reduce the tax deduction available while realizing additional income. Additionally, notice the same income phase outs apply to both Single and Married Filing Jointly, this presents an opportunity for some and a “marriage penalty” to others. If your income falls below the phaseout thresholds, the expanded SALT deduction presents a planning opportunity to bunching other itemized deductions into one tax year to maximize your benefit.

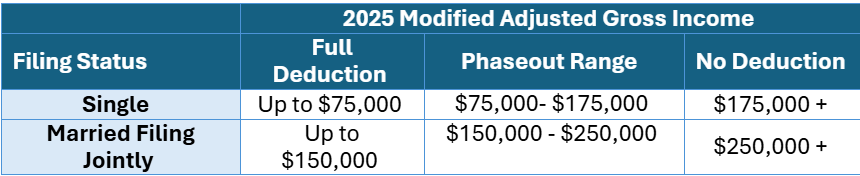

5. Enhanced Senior Deduction

- Temporary

- 2025-2028

- MAGI Phase Outs

The OBBBA introduced an additional $6,000 deduction per person age 65 or older from 2025 until 2028. This deduction is available regardless of whether you claim the standard deduction or itemize but is phased out based on your Modified Adjusted Gross Income (MAGI).

For more information on the Enhanced Senior Deduction.

Additional Source Material

What this means for you? This temporary provision was designed to mimic no tax on Social Security for certain retirees and is separate from the existing over 65 additional amount tied to the standard deduction.

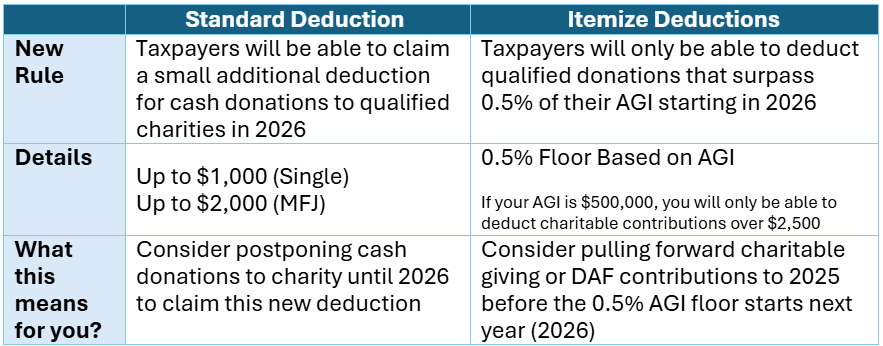

6. New Charitable Rules

- Permanent

- 2026+

Starting in 2026, there are two new rules relating to charitable giving depending on whether you take the standard deduction or itemize. We outline both in the chart below.

Going forward, taxpayers should consider bunching strategies to maximize charitable deductions or strategically utilize QCDs once they qualify at age 70.5.

For more information on the new charitable rules.

Additional Source Material

7. Itemized Deduction Limitation

- Permanent

- 2026+

A cap on the value of itemized deductions for top earners will come into play in 2026. For taxpayers in the 37% bracket, itemized deductions will be limited to 35 cents on the dollar. This means that for every $1 in deductions, only $0.35 will reduce taxable income. Those in the 35% bracket and below will see no impact from this change.

For more information on the Itemized Deduction Limitation.

Additional Source Material

What this means for you? This rule is a targeted limitation on high-income earners and may significantly reduce the benefit of itemized deductions. If you are in the 37% bracket, consider accelerating charitable giving, property tax payments, or deductible medical expenses into 2025 since this rule doesn’t go into effect until 2026.

8. Child Tax Credit (CTC)

- Permanent

- 2026+

- MAGI Phase Out

Starting in 2025, the Child Tax Credit (CTC) is increasing to $2,200 per qualifying child under age 17. These updates increased the CTC by $200, made the income phase-outs permanent, and adjusted the refundable part of the credit for inflation. For 2025, the maximum portion of the credit that can create a refund is $1,700 per child.

For more information on the Child Tax Credit.

Additional Source Material

Two Next-Gen Saving Vehicle OBBBA Changes

9. Trump Account

Starting in 2026, a new tax-deferred saving account will be available for qualifying children born after December 31, 2024. These accounts are essentially restricted until the child turns 18, at which point it is presumed to follow traditional IRA rules. While the opening, funding, and distributions from these account are still being clarified, please reference the following article for more information.

What this means for you? Parents have yet another vehicle to save for their child’s future. Consideration should be placed on what the goal is of the account. For example, if college saving is the priority, then perhaps a 529 plan makes sense as outlined in this comparison article.

10. 529 Plan Enhancements

529 college savings plans will have expanded flexibility starting in 2026. Most notably, the annual K-12 tuition limit for tax free withdrawals will double from $10K to $20K per student and qualified expenses will expand to include books, tutoring, test fees, and a few more educational expenses. To maximize your 529 benefits, take a look at the following article from Saving For College or ask your Weatherly advisor which changes could benefit you.

What this means for you? With a broader list of qualified education expenses and the ability to front load five year’s worth of contributions using the super funding strategy- 529 plans have become an even more compelling tool for education gifting to children or grandchildren.

Other Notable OBBBA Changes

- Auto Loan interest deductible – For qualified vehicles, a temporary deduction of up to $10K in auto loan interest will be available from 2025 to 2028, with a MAGI limit of $100K Single and $200K MFJ.

- No Tax on $25K in Tips and $12.5K/$25K in Overtime Pay – This will be a temporary change from 2025 to 2028 and will only be eligible to those within the corresponding phase-out limits.

- Alternative Minimum Tax (AMT) Changes – In 2026, AMT exemption levels are permanently changing with phaseout thresholds set to $500,000 for Single and $1 Million for Married Filing Jointly (indexed for inflation starting 2027). Phase outs will now happen twice as fast as before with a higher phase-out rate of 50%, up from 25% in 2025.

- Small Business Changes – A number of new laws impact small businesses such as Section 179, expensing of research and development costs, bonus depreciation and more.

- Real Estate Changes – The OBBBA includes several provisions to benefit real estate investors or developers with some additional offsetting changes.

- Health Savings Accounts (HSAs) – Similar to 529 accounts, HSAs will see expanded flexibility through eligibility requirements and expansion to cover telehealth services.

- 3 Clean Energy and Vehicle Tax Credits Ending Soon – Be sure to complete any clean energy home improvement projects by end of year and eligible vehicle purchases by 9/30/2025.

What are the Tradeoffs?

While the new bill has implemented sweeping tax relief and planning opportunities, it comes with notable tradeoffs. The OBBBA made significant cuts to Medicaid and increased the requirements for access to Supplemental Nutrition Assistance Program benefits. Estimates from the CBO, non-partisan budget office, estimate it will add $2.8 trillion to the US deficit between 2025 and 2034. As a result, the federal debt is projected to reach 124% of GDP by 2034, up from 117% under prior law. The long-term budgetary implications of the bill’s provisions will continue to shape fiscal policy in the United States. For more on the Federal Deficit please look at our previous Weatherly blog.

How WAM Can Help?

The OBBBA not only builds on the Tax Cuts and Jobs Act (TCJA) but also introduces a wide range of new provisions that will affect taxpayers in different ways. These updates take effect on varying timelines, with several new-phase outs impacting deductions and credits. Because some provisions are temporary (set to expire in four years) strategic tax and estate planning is essential. We encourage you to work with your Weatherly advisor to review your most recent tax return, identify opportunities under the new law, and develop a plan that positions you for years to come.

Additional Source Material:

- CONGRESS.GOV

- Holistiplan Webinar

- Kiplinger OBBBA Article

- Tax Foundation Blog

- HR Block Article

- Smart Asset – Trump Tax Plan Impact Article

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

Investing in real estate ranks among the most significant financial decisions most individuals will make in their lifetime. Whether investing in a primary residence or an investment property, there are several critical factors that must be considered. Selling a property, especially one held for a long time or a property that has significantly appreciated in value brings substantial tax implications. These consequences often influence the decision to sell. This blog explores key tax considerations and strategies to potentially reduce your tax burden when selling real estate.

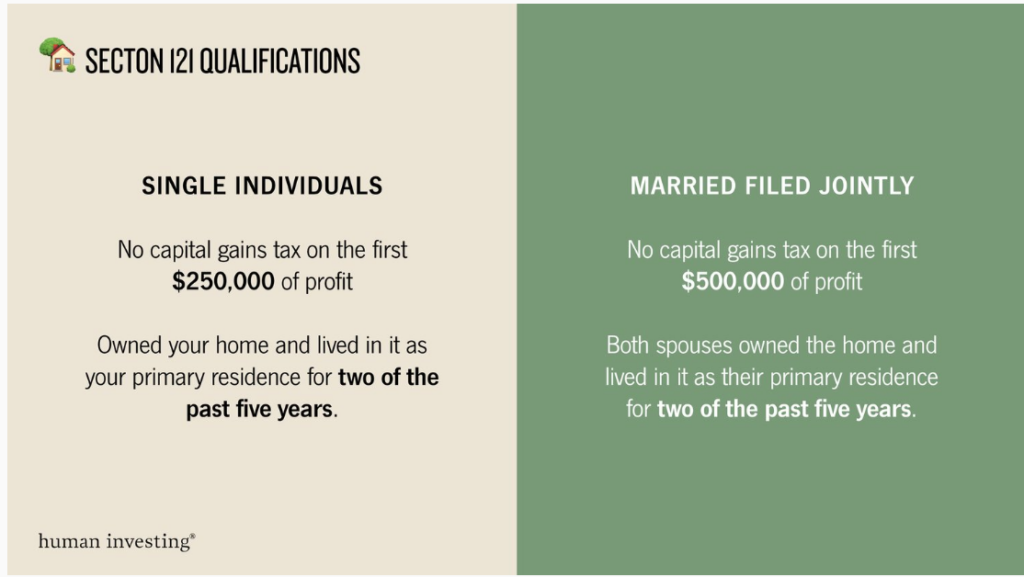

Section 121 Exclusion:

For those looking to sell their primary residence, the first strategy that could assist in easing your tax burden is taking advantage of the Section 121 exclusion as outlined by the IRS.

The IRS’s Section 121 exclusion allows homeowners the ability to exclude a substantial portion of the gain on their home from their taxable income. For individuals, this amount is $250,000 and for those filing jointly, this amount increases to $500,000. We would also note that the cost basis of a primary residence is the purchase price plus any additional upgrades, so it is important to keep track of upgrades overtime as the basis is a very important figure in determining your capital gain exposure.

To qualify, sellers must meet the ownership and use tests – owning and residing in the home as their primary residence for at least two of the last five years.

Ownership and Use Test:

- Ownership Test: The seller must have owned the home for at least two years.

- Use Test: The home must have been the seller’s primary residence for at least two years within the five-year period ending on the sale date.

This exclusion does not apply to investment properties, second homes, or vacation homes, unless these properties are converted into primary residences that meet the specific criteria.

The Section 121 exclusion can be a great tool to assist homeowners that have a low basis in their primary residence or have seen substantial appreciation in the value of their home. While this provision does primarily apply to a primary residence, there are strategies that can be applied to investment properties to assist with tax burdens.

Below is a summary of the tax benefits and requirements to utilize the Section 121 exclusion:

Source: https://www.humaninvesting.com/450-journal/is-it-time-to-sell-your-home

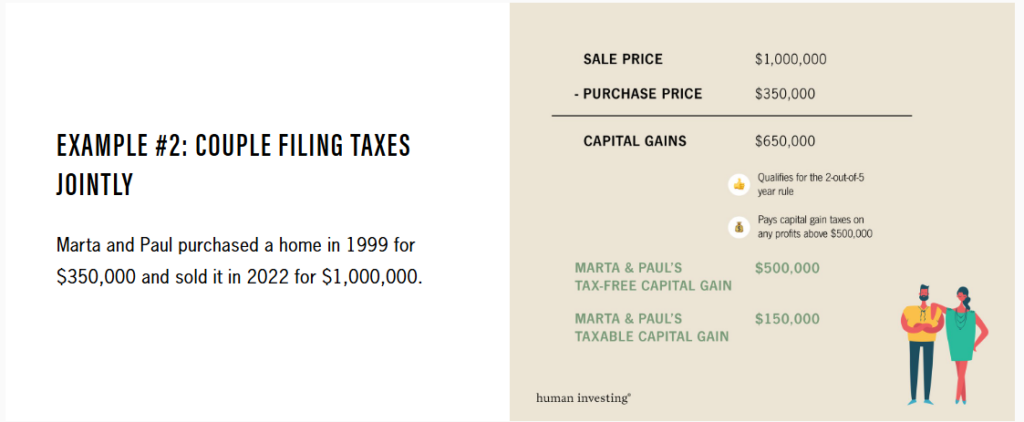

Below is a great example of the Section 121 exclusion in practice. The scenario assumes a couple purchased a home for $350,000 and later sold the home for $1,000,000. The taxable gain on the home would have been $650,000 without the exclusion, but because they met the ownership and use tests, they were able to exclude $500,000 from their capital gain and now are only taxed on $150,000 as opposed to $650,000.

https://www.humaninvesting.com/450-journal/is-it-time-to-sell-your-home

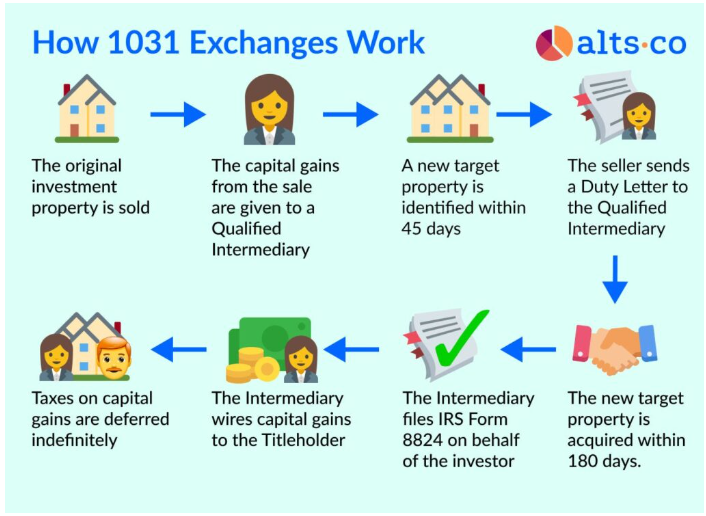

1031 Exchange:

For individuals that have investment properties (second homes, vacation homes, etc.) a 1031 exchange can be a powerful tool to defer capital gains taxes and manage a potential tax burden. Since these types of properties do not qualify for the Section 121 exclusion, sellers would be subject to the full capital gain imposed on the sale of the property and may be subject to depreciation recapture upon the sale if they have been deducting depreciation expenses on these properties. The 1031 exchanges allow for the tax-free exchange of one “like-kind” property to another and can help defer capital gains taxes into the future.

How it works:

The section 1031 exchange process is fairly straightforward but there are some important things to know and timelines to understand. This strategy allows for the exchange of one investment property to another with a broad interpretation of the term “like-kind” property. For example, if you exchanged an apartment building for a commercial building, this would still qualify under the rules of a 1031 exchange since both properties are categorized as investments.

Generally, an exchange is a simple swap of one property for another, however, finding your suitable replacement property may require some time. That is why the majority of 1031 exchanges are what are referred to as delayed exchanges. The mechanics of a delayed 1031 exchange are important to note:

- Sale of investment property

- Qualified Intermediary: Upon selling your investment property, the proceeds must be transferred to a qualified intermediary rather than directly to you to avoid disqualification.

- Identification Rule (45-day rule): From the date of the sale of your investment property, you have 45 days to identify a replacement property in writing to the intermediary. The IRS allows you to designate three properties as potential exchanges as long as you eventually close on one of them.

- Completion Rule (180-day rule): You must close on the new property within 180 days of the sale of your old property.

It is important to note that if there is any cash leftover from the sale of your previous property upon closing on the replacement property, there could be tax implications on the surplus. As an example, if you sold a property for $1,000,000 and bought a property for $900,000, the $100,000 difference would be subject to taxes.

Below is a great illustration of the steps involved in a 1031 exchange:

Source: https://alts.co/1031-exchanges-the-biggest-little-secret-in-real-estate

Benefits and Estate Planning Considerations:

The ultimate benefit of implementing this strategy is that the 1031 is a tax-free exchange of one property to another, so if you have an investment property with a low-cost basis or a property that has significantly appreciated this can be a very powerful tool in managing your tax burden. From an estate planning perspective, utilizing the 1031 exchange strategy can be even more beneficial for your heirs. During your lifetime you can defer taxes on investment properties and then upon your passing, your heirs will inherit these assets with a step-up in cost basis which can significantly reduce the tax burden your heirs will have to manage upon inheriting the assets.

Investors may find themselves in a situation where they no longer want the day to day responsibilities of managing property, would like to defer their capital gains, but remain invested in real estate. Luckily, there is a strategy that could allow you to accomplish all these goals.

Delaware Statutory Trusts:

Delaware Statutory Trusts (DSTs) provide an attractive option for investors who prefer not to manage properties directly. These trusts, established by professional real estate companies known as DST sponsors, allow individuals to invest in significant real estate ventures, typically valued between $30 million and $100 million. This investment structure diversifies into various property types, including multifamily units, office spaces, industrial sites, retail locations, and niche markets such as senior living facilities and self-storage.

Advantages of DST Investments:

Tax Efficiency: DSTs are eligible for 1031 exchanges, offering investors the ability to defer capital gains taxes by reinvesting the proceeds from sold properties into new real estate holdings within the trust.

Access to Premium Assets: Investors gain access to institutional-grade real estate, which would typically be out of reach due to high entry costs.

Passive Investment Opportunity: Investors are not required to manage the properties directly, which is ideal for those who prefer a hands-off investment.

Efficient Transactions: DSTs can facilitate quicker property exchanges, minimizing the risk associated with a traditional 1031 exchange deadlines.

Estate Planning Perks: DSTs allow for a step up in basis for heirs, simplifying the inheritance process and potentially reducing future tax burdens.

DST to an UPREIT: An additional benefit/strategy that could be pursued is the 721 exchange which allows investors to further defer capital gains by converting their DST ownership into an UPREIT where they receive Operating Partnership Units (OP Units). This allows investors access to potentially more liquidity since the OP Units can be converted to REIT shares. REIT shares tend to offer more liquidity compared to a DST investment and typically create a passive income stream to the shareholders.

Considerations of DST Investments:

Investor Qualifications: To invest in a DSTs, individuals must meet the criteria of an accredited investor, defined by having a net worth exceeding $1M (excluding primary residence) or an annual income surpassing $200,000 ($300,000 for joint filers) over the last two years.

Control and Liquidity: While DSTs offer a passive investment model, this also means investors have minimal control over the day-to-day management and decisions. Additionally, DSTs are typically illiquid with investment terms ranging from 3 to 10 years, requiring a long-term commitment.

Market Exposure: Like all real estate investments, DSTs are subject to market fluctuations and interest rate risks, which could affect profitability and cash flow.

Operational Costs: It’s important to understand the fee structure of DSTs, as management and operational fees can vary and impact overall returns.

Delaware Statutory Trusts and UPREITs can be an excellent way for investors to stay in the real estate market without the responsibilities of direct management, offering tax deferral benefits and estate planning advantages. However, potential investors should conduct thorough due diligence and consult with financial advisors to ensure that DST/UPREIT investments align with their overall financial and estate planning objectives.

How Weatherly Can Help:

At Weatherly, our advisors have extensive experience with real estate transactions and their integration into clients’ broader financial plans. We collaborate with clients and other professionals to tailor strategies that align with individual financial goals. Our team is ready to provide guidance on optimizing real estate transactions and planning for future financial stability.

For more details on the strategies mentioned above and how we can assist you, visit our website or contact our team directly.

*Disclosures:* The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

Blog content is human-generated by the Weatherly team members. AI was used to assist with generating titles and subtitles.

By now, we have all likely heard several New Year’s Resolution enthusiasts say, “New Year, New Me!” Per Forbes, one of the most popular 2024 New Year resolutions is improving finances. Since we certainly don’t want to see this resolution drop off, we are sharing our updated 2024 Key Financial Data Sheet to assist you in your financial goals today and all year long.

The 2024 Key Financial Data Sheet is a useful tool that highlights tax brackets, contribution limits, deductions, credits, exclusions and more. In reviewing the history of US taxes, you’ll find how complex our tax code has become over time and the importance of staying up to date with current tax law. In this blog post, we outline the Keys to our Key Financial Data Sheet and potential strategies to help fulfill 2024 resolutions and beyond.

Personal Tax Brackets –

Federal Income Tax Brackets make up the bulk of the annual revenue collected by the IRS each year. Determining your filing status and marginal tax bracket is the first step in tax planning. The majority of US citizens file as Single or Married Filing Jointly (MFJ).

Source: Key Financial Data Sheet 2024

If you are single or considered unmarried, have a qualifying dependent and pay the bulk of the household bills then you may be a candidate for the Head of Household (HOH) filing status. These brackets and deductions are typically more favorable than the Single filing status.

Married Filing Separately (MFS) is also a filing status for married individuals. While some couples simply prefer to keep finances private, others choose to file separately for Federal and State tax benefits. While the tax code generally favors joint filers, in certain instances, it can behoove taxpayers to file separately such as to maximize deductions and/or limit certain liability risk.

Strategies to Consider –

- Roth Conversion – In low taxable income years, consider a Roth conversion strategy to maximize the lower tax rates.

- Engage a Tax Professional – they can help determine which filing status to use and can assist with various tax items.

Standard Deductions & Child Tax Credits –

A common exercise takes place during tax season to determine if someone should itemize deductions or take the standard deduction. With the Tax Cuts and Jobs Act of 2017, the standard deduction nearly doubled, so the number of people that itemize deductions significantly declined. However, planning can be done with charitable giving to maximize deductions in certain years.

Source: Key Financial Data Sheet 2024

Strategies to Consider-

- Donor Advised Fund (DAF) – contributing to a DAF for individuals who itemize may provide a tax deduction as well as flexibility in granting to charities over time.

- Furthermore, a bunching strategy can be utilized or front loading a DAF in a high-income year can be even more effective.

- Qualified Charitable Distribution (QCD) – individuals over the age of 70.5 have a unique opportunity to give directly to charity from an IRA while excluding the distribution from taxable income. With the recent passage of Secure Act 2.0, the 2024 QCD limit is indexed for inflation ($105k) and also allows for a one-time donation of up to $53k to a Charitable Remainder Trust (CRT) or Charitable Gift Annuity (CGA).

- This strategy can help fulfill Required Minimum Distributions (RMD) for taxpayers who are at least age 73 and is a tax efficient way to facilitate charitable giving for those who take the standard deduction.

Capital Gains on Long-Term Capital Gains and Qualified Dividends

Weatherly’s investment philosophy focuses on Long-Term Federal Capital Gains and Qualified Dividend tax rates, specifically within taxable account types.

Source: Key Financial Data Sheet 2024

Strategies to Consider –

- Tax Loss Harvesting – this is part of Weatherly’s ongoing portfolio management services. As we review and rebalance portfolios throughout the year, we analyze prior year tax returns for loss carry forwards that may help reduce current year capital gains. When clients fall in the 15-20% Long Term Federal Capital Gains rate, our team attempts to offset realized gains with losses. This allows us to raise for cash flow needs and/or limit concentrated positions while limiting overall tax liability.

- Tax Gain Harvesting – those with low taxable income may fall within the 0% category and additional gains can be realized without incurring any capital gains tax.

Retirement Contributions:

Source: Key Financial Data Sheet 2024

Taxpayers who are working and receive earned income may be able to contribute to an employer sponsored retirement plan like a 401K. They may also be eligible for a deductible IRA or Roth IRA contribution. Knowing the contribution limits above can allow an individual to maximize their retirement contributions which can reduce their overall taxable income for the year.

Strategies to Consider –

- Traditional vs Roth Contributions – for high earners, contributing to a tax deferred retirement plan would allow more money saved given their current high tax bracket. For those in low tax brackets, contributing to a Roth account could limit higher taxes in the future.

- Self-Employed 401K – can allow certain business owners to contribute as both an employee and employer to further maximize annual deferrals.

Estates, Trusts and Planning for the Future –

Estate planning has become a growing part of financial planning, due to the inevitable Great Wealth Transfer. Individuals and families often utilize trust documents to effectively transfer assets to their heirs. However, income tax rates on estates and certain trusts are the most dramatic as they reach the highest tax bracket the quickest.

Source: Key Financial Data Sheet 2024

While this is a major factor, it is not the only consideration when it comes to wealth transfer.

A question we get a lot is, what is the annual gift tax exclusion amount? For 2024, it is $18,000, which is an important figure as this is how much one person may gift to another person without needing to file a gift tax return (Form 709) and reduce their Estate Exclusion Amount.

Source: Key Financial Data Sheet 2024

Under current law, we are given a lifetime estate exclusion amount ($13.61M per person in 2024), which you can utilize while alive or at your time of death. For taxable estates/gifts over the exclusion amount would incur a 40% tax hit.

The tax Cuts and Jobs Act of 2017 made significant changes to the estate exclusion amount. This law more than doubled the exclusion amount until its sunsets January 1st, 2026 and reverts back to prior amounts (after adjusting for inflation). Without an extension from Congress, most analysts are predicting the estate exclusion amount will drop to $6M – $7M per person.

Strategies to Consider –

- Financial Plan – if gifting is of interest to you, it is important to first have a financial plan completed for your own financial situation. If your personal plan is successful, there are various estate planning/annual gifting opportunities to explore.

- Annual Gifting – a gift up to the annual exclusion amount would sidestep the need to file tax form 709 and would not reduce your lifetime estate exclusion amount.

- Consider gifting appreciating assets or funding an investment account.A 529 college savings plan can be superfunded by forward gifting up to 5 years worth of the annual exclusion amount in the current year.

- Our 5 Estate Planning Strategies to Consider blogpost highlights a few different strategies to consider with your team of professionals.

- Leverage the Current High Estate Exemption Amount – Gifting a high amount of assets to take advantage of the higher lifetime estate exclusion amount.

- Asset location and type of accounts should be considered to further enhance this strategy.

Engaging an estate planning attorney in tandem with your Weatherly advisor is vital to properly plan for your asset transfer.

How Weatherly Can Help-

Given the uniqueness of our tax code, Weatherly likes to gather your tax return to help identify planning opportunities. Based on our conversations with you and data we gather, we can then outline which strategies could be most impactful to you. With January 1st, 2026 right around the corner, it is a great time to revisit your estate plan and gifting goals prior to the revision of the estate exclusion amount.

Please reach out to schedule a call with your advisor to see how the Key Financial Data Sheet may improve your finances this year and the decades to come.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

If you find taxes confusing, then you are not alone. Albert Einstein once said, “the hardest thing in the world to understand is the income tax.” While we outline many useful tax details in our Key Financial Data Sheet and even observed the US history of taxes in a prior blog post, it is truly the IRS’ job to fully understand and enforce the tax code. We also find the tax return essential to our services and we like to receive a secure copy each year.

Within your tax return is a wealth of information that we utilize to support our two core competencies – financial planning and investment management. Our goal is to get to know your full financial picture so we can tailor our advice to your specific situation to increase overall tax-efficiency. While we prefer to analyze your full tax return, the following sections give us specific insights into how we can best serve you.

1040

The 1040 gives our team a summary of your full tax picture. Numbers on your 1040 that are of particular interest to our team are your Adjusted Gross Income (AGI) and your Taxable Income. Your Taxable Income, in conjunction with your Filing Status, help us determine your Marginal Federal Tax Bracket. Your tax bracket drives the types of securities we purchase for your taxable portfolio, like a Trust or individual account. For example, a person in a very high marginal tax bracket may benefit from tax-exempt municipal bonds. Alternatively, a person in a low tax bracket has less of a need for tax-free income and may benefit from an allocation to taxable corporate bonds. Weatherly always looks at the Taxable Equivalent Yield (TEY) to compare a taxable bond to a tax-exempt bond to determine which offers the most attractive after-tax return per client account.

Tax brackets are also useful within financial planning to determine if it is a good year for a Roth conversion. This strategy can take advantage of a low-income year by leveraging current lower income tax brackets to enhance after-tax returns over time. Since Roth assets can grow tax free, they often become a desirable source of funds in legacy planning for beneficiaries.

This first page is also useful when onboarding new clients. It provides our team with your full name, Social Security Number, address, and lists any dependents you claim. This information facilitates us in filling out new client paperwork and expedites the client onboarding process. We also track your tax preparer as listed at the bottom of form 1040, as we may need to contact them with any questions that may come up regarding your tax situation and various tax strategies. With your consent, we can also contact them to directly and securely send your tax forms to assist them in filing your return.

Schedule 1

Schedule 1 outlines any additional income you earned throughout the tax year as well as adjustments to your income. Our team appreciates having a full outline of your revenue streams and how much you receive. It can be overwhelming to have to keep track of this information independently, so it is often easier to send this summary to your advisor to give them some context on your cashflow. We can also model the income into a financial evaluation and build out various scenarios.

Schedule A

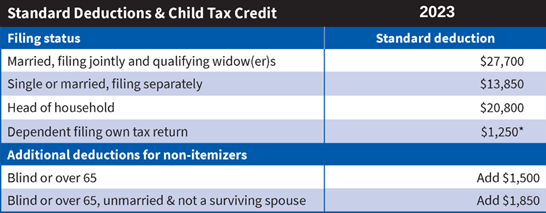

If you itemize your deductions, instead of taking the standard deduction, you will need to fill out a Schedule A. The Tax Cuts and Jobs Act (TCJA) in 2018 made significant changes to the deductions you can itemize. The main deductions are medical costs (that exceed 7.5% of AGI), state and local taxes (now capped at $10,000), mortgage interest and gifts to charities. The TCJA also significantly increased the standard deduction which dramatically reduced the amount of Americans itemizing their deductions. For the 2023 tax year, the standard deductions are mainly based on filing status but can also be affected by other factors. Please see the chart below for details:

Sourced from: https://www.weatherlyassetmgt.com/wp-content/uploads/2023/01/2023_KEY_FINANCIAL_DATA_CHART.pdf

Many of our clients itemize their deductions because their large donations to charities throughout the year frequently exceed the standard deduction. One of the strategies we utilize includes appreciated stock contributions to a Donor Advised Funds (DAF). If you have philanthropic goals, then our team can help evaluate timing and security selection for tax aware giving methods. Your generosity not only helps those in need but can decrease your taxable income for the year. It is important to note, if you do not itemize, your charitable contributions are not deductible but other strategies like Qualified Charitable Distributions (QCDs) may be an alternative.

Schedule C

If you are a sole proprietor, you should also have Schedule C included in your tax return. This form indicates any profit or loss your business experienced throughout the year. We use this to help us determine if it would be beneficial to take any gains or losses in your account to offset the profits or losses from your business. We can also incorporate the income streams and a future business sale into your financial evaluation. Seeing Schedule C typically leads into a conversation about retirement contributions and if a self-employed 401K or other retirement plan is appropriate.

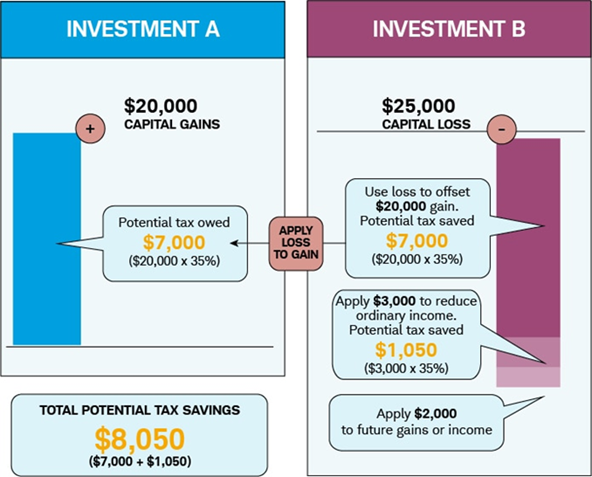

Schedule D

Schedule D reports capital gains and losses. Our team actively seeks to limit capital gains each year, through tax loss harvesting. This strategy includes taking losses (if available) to offset capital gains in taxable accounts. Occasionally, a client will have capital losses that exceed gains. In this instance you may deduct up to $3,000 ($1,500 if married filing separately) against ordinary income on your 1040 and carry forward the remaining losses to future years.

Sourced from: https://www.schwab.com/learn/story/how-to-cut-your-tax-bill-with-tax-loss-harvesting

In periods of extreme volatility, this strategy can be used proactively so unused losses can be used to offset future gains when the market recovers. This method along with other tactics are used to successfully reduce concentrated positions over time while limiting adverse tax consequences. As part of our ongoing investment management services, we actively seek to buy and sell securities with a tax conscious approach.

Schedule E

Many of our clients own rental properties, receive royalties, own S corporations, or receive income from estates and trusts. Schedule E is where the income and losses from those avenues are reported. Our advisors review this form to gain better understanding of your financial situation and can work different scenarios into financial evaluations.

1040-ES and Vouchers

These vouchers help our team plan out cash flows throughout the year. Understanding your cash needs allows our team to accumulate cash and send funds to your bank proactively to help cover quarterly tax estimated payments.

How Weatherly Can Help

The Weatherly team takes pride in our ability to create tax efficient strategies specific to each client so they can ultimately keep more money in their pockets. Each client not only has their own unique situation, but tax and estate laws can change. A current tax return allows us to identify any new planning opportunities for the year and assists in our tax conscious investment approach.

If you haven’t already done so, please send us your tax return by utilizing our secure portal or another secure method. If easier, feel free to connect us with your tax preparer and we can request the return directly from them. We work closely with many tax professionals to securely share tax documents and to collaborate on any tax planning initiatives.

As always, we welcome your questions and look forward to saving you money!

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

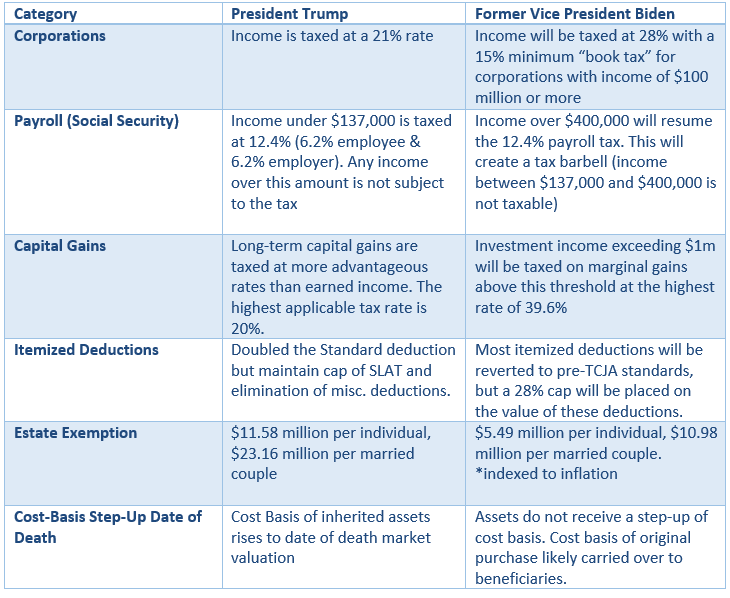

Not much is normal these days – political conventions are virtual, major sports are played in empty arenas, and classrooms are remote. One thing that seems to remain a constant are the proposals being put forth by Presidential Candidates in the upcoming election to outline their goals, objectives, and strategies and the corresponding action by advisers to prepare their clients.

Former Vice President Joe Biden, now the Democratic Party’s official nominee for President, recently released his tax policy proposal for his administration should he win the White House in November. Key provisions in the 2017 Tax and Jobs Cuts Act (TCJA), set to expire in 2025, are now at stake of being eliminated early. President Trump’s communication has alluded to making the TCJA permanent. Below are the respective Candidates’ tax policies for their administrations:

Recently passed legislation in the SECURE and CARES Acts has created an opportunity for Weatherly clients in their “gap years” with large amounts of tax-deferred assets to potentially utilize a Roth Conversion in 2020 to lower personal taxes in future years and alleviate the tax burden for their heirs.

- CARES Act – As Required Minimum Distributions (RMD) have been waived in the 2020 calendar year, IRA owners have the flexibility to entirely skip their distributions or selectively withdrawal for Qualified Charitable Distributions or Roth Conversions. Both strategies can help reduce RMDs in future years without generating as large of a tax bill this year. Additional information on Qualified Charitable Distribution strategies to help reduce RMDs in future years. We will discuss the Roth Conversion strategy in more detail below.

- SECURE Act – Certain non-spouse beneficiaries are now required to fully withdraw the balance of an Inherited IRA within a 10-year window. Previously, these heirs could distribute the balance based on their life expectancy, a significant advantage for individuals at a young age with a long life ahead of him or her. Reducing the balance of non-Roth IRA assets will allow for greater tax flexibility for the ultimate recipient of the assets as distributions from Inherited Roth IRAs are not taxable.

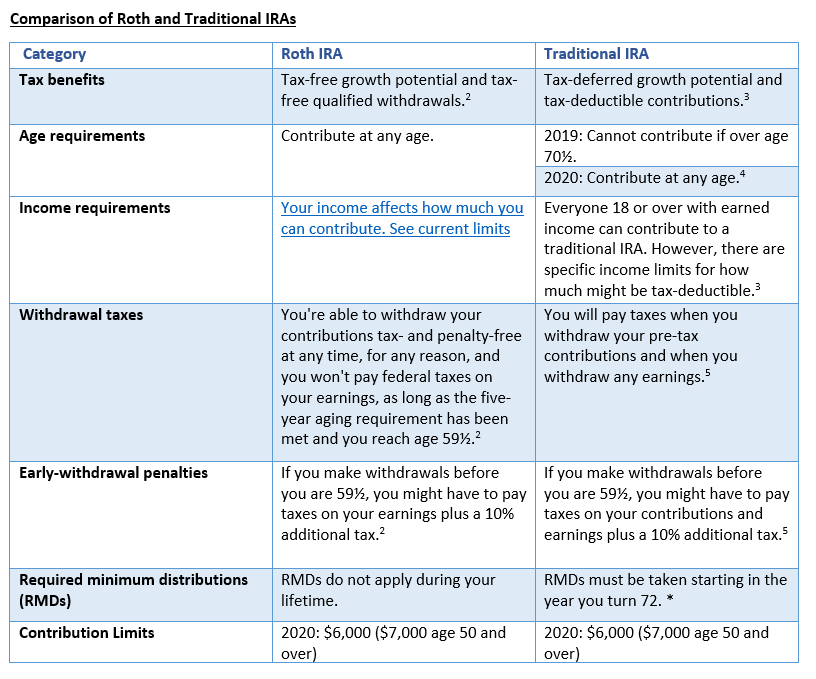

For many individuals a Roth conversion is somewhat of an unfamiliar concept. In order to understand this concept better, let’s look at a comparison between key features of a Traditional IRA and a Roth IRA, how they came to be an effective financial planning tool, how they work, and why they may make more sense than ever to do in 2020.

The Roth IRA was introduced as part of the Taxpayer Relief Act of 1997, but the Roth Conversion didn’t get its start as an effective financial planning tool until 2010, when limitations from the Tax Increase Prevention and Reconciliation Act of 2005 were removed. The removal of the limitations allowed individuals with a Modified Adjusted Gross Income (MAGI) over $100,000 to fully utilize the capabilities of a Roth Conversion.

How does a Roth Conversion work?

A Roth conversion allows individuals to take pre-tax money (cash or securities) from a Traditional IRA or 401(k) and reinvest those funds into a Roth IRA. The distribution from the traditional IRA will be included in gross income and subject to income tax at the time of conversion.

Why consider a Roth Conversion?

The decision to complete a Roth Conversion primarily comes down to deciding to pay taxes today or at retirement, with the intention to pay taxes at a lower tax rate today than you would in future years. This strategy can be especially effective for those expecting to be in a higher marginal tax bracket in the future and if you can afford the tax bill generated by the conversion.

With the amount of fiscal stimulus recently pumped into markets to combat COVID-19, along with the current low tax rate policies, there is a large likelihood that taxes will increase in the foreseeable future. If an individual believes they will be in a lower tax bracket during retirement, a Roth Conversion may not make sense.

What does this mean for your beneficiaries?

One of the major changes to retirement accounts under the SECURE act was the removal of the “Stretch” provision for IRAs inherited in 2020 and after. Certain non-spouse beneficiaries are now required to fully withdraw the balance of an Inherited IRA within a 10-year window.

Because of the removal of the “stretch” provision, it may be beneficial to use a specific Roth Conversion strategy that is referred to as the “amortization table approach.” This approach focuses on lowering the income tax liability for individuals who inherit a Traditional IRA. This can be done through the conversion of a higher annual dollar amount to a Roth IRA during the original IRA owner’s lifetime, in order to minimize the tax burden beneficiaries will face when taking their Required Minimum Distributions (RMDs) within the required 10-year window.

Read more about this approach here.

Why is now the time to consider this?

With the current backdrop of the COVID-19 pandemic, many individuals have seen a reduction of hours or a wage decrease, which may mean they are in a lower tax bracket this year than in previous or future years. Individuals who took advantage of the CARES Act ability to skip their required minimum distributions may also be in a significantly lower tax bracket in 2020. The additional unknown surrounding what taxes will look like in 2021 and going forward makes this year an ideal time to explore Roth Conversions with your advisor.

Caveats:

It is important to consult with a financial or tax professional when considering a Roth conversion to make sure that the conversion does not push the client into a significantly higher federal income tax bracket. Additional information regarding the 2020 Tax Rate Schedule can be found here.

For Example: A married couple filing jointly with taxable income of $60,000 can convert up to $20,250 to a Roth IRA while still staying within the 12% tax bracket. The 22% tax bracket starts at $80,251.

Additional Resources:

https://www.barrons.com/articles/trump-biden-and-taxes-what-to-expect-51596843040

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

“…In this world nothing can be said to be certain, except death and taxes.” -Benjamin Franklin 1789

What Benjamin Franklin said so many years ago still stands true today. There is no escaping death and taxes. While the individual tax filing extension date just passed on October 15th and as we gear up for our year-end tax planning strategy, we felt it would be a good opportunity to review the history of income taxes and role of the Internal Revenue Service (IRS).

As we all know, it is our civic duty as Americans to pay our fair share of taxes. Although tax is such a broad category including sales tax, state and local tax, property tax, excise tax, estate tax and much more, for purposes of this blog post we decided to focus our attention on federal income taxes. These taxes carry the majority share of the IRS revenue each year.

The IRS recently released data for the 2017 tax year. Although this was before the passage of the major tax reform bill in late 2017, The Tax Cuts and Jobs Act (TCJA), we wanted to analyze the numbers. Most taxpayers played their part as over 143 million tax returns were filed with individual income tax collections totaling $1.6 trillion dollars. Due to the progressive nature of the tax brackets, the average effective tax rate for 2017 was 14.6%. However, certain US citizens carried the bulk of the tax burden. The top wage earners are often scrutinized for utilizing various tax strategies to lower their amount of taxable income. So, let’s examine the top 1% of taxpayers and their impact on the IRS revenue.

To put things in perspective, to be a top 1% taxpayer, you would need income in excess of $515,371 (as of 2017). Although the top tax bracket for the 2017 year was 39.6%, these top 1% of taxpayers had an average individual effective tax rate of 26.76%. This is partially due to portfolio related income taxed at the preferential qualified dividend/long-term capital gains rates of 20% (highest capital gains tax rate). However, the top 1% of taxpayers accounted for 38.47% of the total income tax revenue collected by the IRS. Furthermore, the amount paid by the top 1% is greater than the amount of tax paid by the bottom 90% of tax payers combined (29.92% of total tax share). As these top earners pay much of the total share of income tax, we wonder if this will change in the future. This largely depends on the state of the economy and political landscape. Before predicting where we are headed with the 2020 election on the horizon, we wanted to look back at how taxes changed through different presidential administrations.

Abraham Lincoln 1861- 1865

Although short lived, the Revenue Act of 1861 imposed the first tax on the American people. The tax was 3% on income over $800 and it was used to pay for the Civil War. To enforce collection, the Internal Revenue Service (IRS) was created on July 1, 1862. This tax was repealed by Congress in 1871.

Grover Cleveland 1885-1889, 1893-1897

In 1894 Congress tried to enact a federal flat rate income tax but the U.S. Supreme Court ruled it unconstitutional because of the varying population in each state. What a time to earn money!

Woodrow Wilson 1913- 1921

In 1913, The IRS created form 1040 for better tax reporting and record keeping. Additionally, the 16th Amendment was changed so taxes did not need to be proportionate to state population. Then a 1% tax was placed on income over $3,000 and 6% on income over $500,000. In 1916, the tax was increased to 2% to aid in World War I expenses. Taxes changed yet again in 1917 by placing the 2% tax on all income over $1,000 and the surtax increased to 63%. By 1920, taxation revenue was up to $6.6 Billion, but fell to $1.9 Billion by 1932 as a result of the Great Depression.

Herbert Hoover 1929-1933

The Revenue Act of 1932 ended up being a major tax reform in US history. The bill caused increased tax rates across the board with the lowest rate starting at 4% and gradually increasing to the highest rate of 63%. This greatly impacted high earners and caused the affluent to explore various tax strategies to reduce income. Corporate taxes also increased by nearly 15%.

Franklin Roosevelt 1933-1945

With the wealthy uncovering several tax loopholes, President Franklin Roosevelt sought out to tax the rich to offset the large deficits created by the New Deal. In 1944, he raised the top marginal tax rate to its highest rate ever, 94%, to help fund the war. And then in 1945, he lowered the rate down to 86.45%. By 1945, yearly tax revenue was $45 billion, up from $9 billion in 1941. Much of this increase was required to fund Social Security which was established in 1935.

Harry Truman 1945-1953

Although Republicans in the Senate and House were able to cut rates in 1948, President Truman increased taxes in 1950 to raise money for the Korean War. The lowest and highest tax brackets increased to 20% and 91%, respectively.

Lyndon B. Johnson 1963-1969

The Revenue Act of 1964 was initially pushed for by President John F. Kennedy but implemented by President Lyndon Johnson. The idea was to cut tax rates to increase job growth. This act cut the top rate to 70%. Furthermore, the standard deduction was initiated and set at $300. Then, in 1965 Medicare was introduced. Similar to other social programs like Social Security, Medicare made it more difficult to lower taxes without running large deficits.

Ronald Reagan 1981- 1989

President Ronald Reagan’s Economic Recovery Tax Act of 1981 greatly reduced the top tax rate from 70% to 50%. The law also indexed tax brackets for inflation. His hope was to encourage savings and investments to stimulate economic growth. Then again in 1986, Ronald Reagan created the Tax Reform Act to further cut taxes and simplify the tax code. The top rate was lowered to 28%, and the standard deduction and personal exemption were increased. This favored many but was extra beneficial to low-income households.

George H.W. Bush 1989- 1993

President George H.W. Bush passed the Omnibus Budget Reconciliation Act of 1990. This raised the top rate to 31% in efforts to reduce the federal deficit.

Bill Clinton 1993-2001

Bill Clinton raised the top tax bracket to 39.6% in 1993. He also increased the taxable portion of Social Security benefits. In 1997, President Bill Clinton signed the Taxpayer Relief Act. The act introduced new tax breaks for families with dependent children and education costs. It lowered the capital gains tax rates to 10-15% to encourage investments. The Roth IRA was born.

George W. Bush 2001-2009

President George W. Bush implemented The Economic Growth and Tax Relief Reconciliation Act of 2001 to lower tax rates and drop the top rate to 35%. A new 10% tax was imposed for the first $6,000 of income for individuals ($12,000 for married couples). Bush also initiated The Jobs and Growth Tax Reconciliation Act of 2003. This act cut taxes again and lowered capital gains rates. This greatly benefited high earners.

Barack Obama 2009-2017

The Obama American Taxpayer Relief Act of 2012 and Obama’s Affordable Care Act of 2010 increased the tax rates with the top rate being 39.6%. It also placed additional taxes relating to health care. The Net Investment Income Tax (NIIT) was also created which imposed a 3.8% surtax intended to tax portfolio income over a certain threshold. Learn more about NIIT here.

Donald Trump 2017- Present

President Trump pushed the Tax Cuts and Jobs Act of 2017 through Congress, with numerous changes to the tax law. To highlight a few, the standard deduction nearly doubled, various tax deductions were eliminated, estate tax exclusion nearly doubled, individual tax rates were lowered, and corporate tax rates dropped significantly to a flat 21%. The top individual rate is currently at 37%. A Sunset provision was also enacted which would cause some of the changes to revert to prior law in 2026.

To review details of the current tax law, please reference our 2019 Key Financial Data Sheet.

When reflecting on our country’s long history of taxes, it is evident that we have come a long way since 1861! As the 2020 election nears, discussions about expanding social programs and health care reform polarize political debates. As we do not have a crystal ball to see into the future, we will reserve judgement on what will happen with the tax code going forward. However, we believe it is important for investors to focus on what they can do today.

Although income taxes are often the highest tax US citizens pay, capital gains tax from investment portfolios can also be costly. As we are in the longest bull market to date, it is becoming more challenging to offset gains. Many investors face a difficult question when seeking to rebalance or de-risk their taxable investment accounts. Do you sell investments to reach your target allocation and incur additional taxes OR pay no taxes (by making no changes) and have a higher risk exposure to equity investments? As this can be a costly question, investors can look to tax strategies in other areas to help limit the total liability.

Some of these tax strategies include-

- Contributions to retirement accounts

- 401Ks and self employed 401Ks (by year end)

- Traditional IRAs and Roth IRAs (by April 15th of 2020)

- SEP IRA (by April 15th or October 15th if filing an extension)

- Donations to Charities

- Qualified Charitable Distribution (QCD) through IRA

- Donations to Donor Advised Fund (DAF)

- Tax Loss Harvesting

- Utilizing Old Tax Loss Carry Forward or Net Operating Losses for businesses (NOL)

As your trusted advisors, we are happy to elaborate on the strategies above and explore potential opportunities. As the bulk of this planning needs to be completed PRIOR to yearend, it is important to take action sooner than later. To allow us ample time to review and make recommendations to your specific situation, please provide us with your 2018 tax return at your earliest convenience.

As opinions vary around the topic of taxes, we hope to find common ground by concluding with a quote from famous historian, Albert Bushnell Hart, – “Taxation is the price which civilized communities pay for the opportunity of remaining civilized.”

Further Reading:

https://www.gobankingrates.com/taxes/tax-laws/biggest-tax-reforms-in-us-history/#10

https://www.irs.gov/pub/irs-pdf/p1304.pdf

https://www.history.com/news/why-we-pay-taxes

https://www.forbes.com/2010/04/14/tax-history-law-personal-finance-tax-law-changes.html#5dad45da1cf8

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

The TCJA that was signed into law on December 22, 2017 made significant changes to the tax code. The changes were broad and sweeping which leads to questions about what changed and what we can do to mitigate taxes under a new code. While the increase in the Standard Deduction has some individuals moving away from itemizing, there are still ways to decrease tax liability with “above-the-line” deductions, business and charitable planning and investment strategies. Our Key Data Chart outlines the main figures to focus on for tax planning. Read on to see our Top 5 strategies that might make a positive impact on your tax situation.

![]()

The What: Retirement plan contributions, an above-the-line deduction

The How: The most common way to reduce taxable income is a contribution to an eligible retirement account. This strategy is beneficial for two reasons – you can lower your tax bill now and access tax-deferred growth for the future.

This chart highlights the allowable deferrable amounts for various types of retirement plans, depending on your business structure and compensation. These contributions are “above-the-line” and directly reduce your Adjusted Gross Income (AGI), even if you are not itemizing deductions on Schedule A.

Retirement plan contributions not only reduce your taxes now, but also grow tax-deferred until you are required to take a distribution (RMD) at age 70.5. This graph notes the benefits of tax-deferred growth.

![]()

The What: Business structure, how the change in tax rates can impact your deductions

The How: C corps and qualified pass-through entities, including sole proprietorships, partnerships, S corps and LLCs benefit from the TCJA. C corps saw a reduction in tax rates from 35% to a flat 21%; pass-through entities with qualified business income are able to take a 20% tax deduction.

We’ve been encouraging our clients with business income of any sort to consult with their CPA on what business structure is appropriate for them and eligibility for the deduction. Similar to above-the-line contributions, you can take the 20% tax deduction, even if you aren’t itemizing under the new tax law.

![]()

The What: Charitable deductions, QCDs and bunching donations

The How: If you are over age 70.5, own a retirement account and are taking a Required Minimum Distribution, consider a Qualified Charitable Distribution. You are able to donate directly from an IRA up to $100,000/year. These donations are not included in taxable income on your 1040 and offer a tax benefit, even if you aren’t itemizing.

If you have a larger than usual tax year, consider “bunching” charitable donations to maximize your Schedule A deductions. With the TCJA reform, we’re seeing more individuals utilizing the standard deduction over itemizing. We’ve reviewed frontloading charitable funds on our blog, along with the advantages of donating stock and QCDs.

![]()

The What: Taking advantage of “gap years” with low income

The How: Financial planning is a tool most often used to visualize a path to retirement, but these plans are also helpful in identifying when you might have “gap years” of income in retirement. If you have a couple of years between retirement and collecting Social Security or RMDs, you might be able to take advantage of strategies like Roth IRA Conversions or even an IRA withdrawal to a taxable account. You might benefit your future self by removing assets from a Traditional or Rollover IRA in years when the tax rates are lower due to the TCJA versus having a higher RMD in later years when tax rates are less certain.

![]()

The What: Investing, utilizing tax-efficient stocks and bonds to maximize returns

The How: Although tax rates are lower, the limitation of itemized deductions, particularly in high tax states, makes tax-efficient investing even more attractive. Weatherly primarily utilizes individual stocks and bonds in our investment portfolios. Municipal bonds remain attractive, paying tax-free income at the federal level, and depending on the state of issuance and where you live, the income may be tax-free on your state return too. Qualified dividends and capital gains are taxed at a more favorable rate, and even in some of the “gap years” identified above we’ve seen individuals fall into the 0% bracket – you can offload low basis stock without the tax burden if planned appropriately.

Investment Management Fees and Tax Deduction

Prior to the TCJA, investment management and professional fees were tax deductible if they exceeded 2% of AGI. You can still pay investment management fees, as applicable, from a Traditional or Rollover IRA. This is a tax-free “withdrawal” which can help lower RMD impact in the future.

Some states conform to the TCJA at the federal level, mirroring the itemized deduction schedule. Others, like California, do not adhere to conformity and may still allow for deduction of investment management fees on your state return. You can check here or ask your CPA what you are eligible for at the state level.

Resources:

https://www.fidelity.com/viewpoints/personal-finance/taking-tax-deductions

https://www.nerdwallet.com/blog/taxes/pass-through-income-tax-deduction/

https://www.taxdebthelp.com/blog/pass-through-tax-deduction

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

With the holidays and year end quickly approaching, ’tis the season of detailed tax planning and gift giving! While tax planning and gift giving don’t always get a seat at the same strategy table, we encourage clients to consider their charitable endeavors as a critical piece of the overall tax and financial planning process. A yearend conversation with your CPA and Weatherly provides an excellent opportunity to maximize efficiency while accomplishing charitable goals. In addition, many clients utilize charitable planning as the beginning steps of the family conversation with their heirs, specifically to communicate family values and begin the legacy planning process. Giving funds to those less fortunate or causes you are passionate about, while capturing a tax benefit offers a winning combination for our clients.

We have outlined two efficient approaches below:

Donor Advised Fund

A Donor Advised Fund (DAF) is a philanthropic account that allows a donor to make charitable contributions, receive an immediate tax write-off and subsequently grant funds out to charities over time. DAFs are available for clients at most community foundations and large brokerage firms. Weatherly can facilitate opening a DAF at either type of institution and will assist in selecting securities for donation.

What can be donated?

The donor can of course contribute cash, however, one of the main benefits of a donor advised fund is your ability to contribute appreciated securities, both publicly traded and some privately held securities.

- The donor receives a deduction equal to the fair market value (FMV) of the securities on the day the shares are contributed to the DAF and does not have to pay tax on the unrealized capital gain.

- The contribution is considered an irrevocable gift and cannot be reclaimed by the donor, this allows the donor to claim the FMV as a deduction on their tax return in the current tax year.

- The securities are immediately converted to cash by the custodian and held in the account awaiting the donor’s instructions.

- The DAF provides an opportunity to decrease a low basis concentrated position while accomplishing charitable donation goals.

Example here: https://www.fidelitycharitable.org/giving-strategies/tax-estate-planning/appreciated-securities.shtml

Investing the funds in a DAF

- Once the donation is made to the DAF, the donation can grow tax- free. Custodians typically offer model portfolios invested in exchange traded funds or mutual funds at reasonable management fees. The end charities benefit from more dollars available to the donor to grant out.

- Once over a certain dollar amount many custodians allow the funds to be managed by an Advisor with broader investment choices – individual stocks and bonds, mutual funds, exchange traded funds, alternatives etc. Fees and threshold vary per custodian.

Estate and Legacy planning

- The DAF offers a convenient way to leave funds to charity in your estate. Instead of naming specific charitable organizations in your estate plan you can simply name the DAF – during your lifetime if you want to change the dispersion of funds to the charities listed or change the selected organizations receiving funds you can make this edit simply via the DAF at no cost versus paying an attorney to amend your estate documents.

- The donor can also select a successor on the DAF so the account can continue under direction of the selected individual after the donor has communicated their charitable values and vision for the funds.

- In our experience, clients find this vehicle an excellent way to start the family conversation surrounding values, charitable goals, wealth transfer, and legacy planning. A discussion with heirs and other family members to collectively select causes and organizations that represent family values is a meaningful exercise for teamwork and family unity. This may make the transition to a broader conversation regarding estate planning smoother if and when it is appropriate for your family. See a link to Weatherly’s family conversation assessment card here.

Example #1: Concentrated Position – Donating Stock versus Cash

A couple in their early 60’s both worked for a technology company, ABC inc., for 20 years. While working they received compensation via incentive stock options that they exercised over time. They now have a concentrated position of the company stock equal to 30% of their overall net worth and would like to diversify out of the position over time to decrease risk as they near retirement. The shares have a very low cost basis, and therefore large capital gain tax if they were to liquidate shares. They are both still working and adding to their portfolio via 401(k) and Trust contributions annually. They are charitably inclined and donate on average $25,000 annually to organizations supporting foster youth programs. They have been completing these donations with cash from annual income.

Mike and Susan’s advisor recommends they open a DAF and utilize the ABC Inc. stock to complete their annual gifting. They will transfer shares from their Trust account to the DAF and receive a deduction on their tax return equal to the Fair Market Value of the stock. The shares will be immediately converted to cash and Mike and Susan can grant out the funds to the charities they regularly support.

They did not pay any capital gains tax and can now add the $25,000 cash they would have used for the charitable donation to their Trust account for investment in other sectors, ensuring diversification over time.

Example #2: Small Business Sale – Frontloading a DAF