When it comes to life, few gifts are more valuable than financial advice. As young professionals and their families navigate the complexities of today’s world, financial planning is essential in helping them reach various milestones in life. Whether they are just beginning their career, starting a family, or beginning to plan for retirement, a financial advisor can be an invaluable asset.

“Industry studies estimate that financial advice can add between 1.5% and 4% per year to account growth over extended periods.” Source: Fidelity

For young professionals and new families just getting started, having an advisor who takes a holistic approach to your situation can add tremendous value and have a long-term impact. A good financial advisor will help create a plan that considers income, expenses, and long-term goals, to optimize cash flow. In addition, they will help identify areas where money can be saved or invested for long-term objectives, like retirement or college savings plans for children. An experienced financial planner can also guide clients through the nuances of tax mitigation strategies and estate planning considerations.

In this blog post, we will discuss these topics in more detail alongside the benefits of working with an experienced wealth management advisor on the journey to financial success.

Cash Flow Optimization:

For young professionals and families, financial planning can be one of the most intimidating aspects of life. One of the critical steps in achieving your financial goals is to understand how to optimize cash flow between discretionary and non-discretionary spending, 401K contributions, and 529 college savings plans. This can help provide clarity around how to achieve financial goals in the short term and long term.

Non-Discretionary vs. Discretionary Spending

When it comes to allocating a paycheck, there are several factors to consider. First, it is vital to set aside money for essential expenses such as rent or mortgage payments, insurance premiums, utilities, food, gas/transportation, and other necessary living costs. Additionally, it is prudent to establish an emergency fund with at least three to six months’ worth of expenses. These items should take precedence over any other form of spending or saving.

Retirement Contributions

After assessing the difference between non-discretionary and discretionary spending it is essential to think strategically about how the remaining funds should be allocated between retirement savings (401k) and college savings (529), as applicable. Through dialogue with a WAM advisor, we can offer tailored advice on what you should prioritize based on your individual goals.

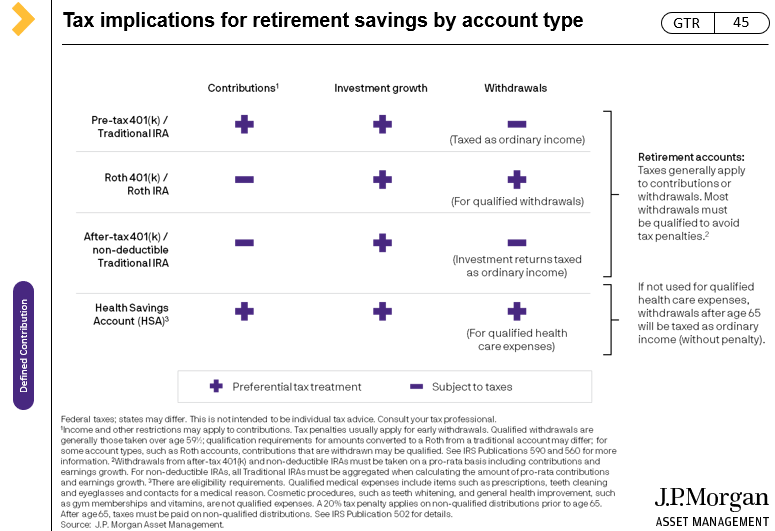

Contributing to a 401K is often a great idea because of its tax advantages and investment options available through employer plans. Often, 401K plans come in two forms: a Traditional or a Roth option. Traditional 401K contributions are made before taxes, which offers a tax deduction today, and grow tax-free until funds are withdrawn in retirement. Conversely, the Roth option consists of after-tax contributions, with no tax deduction today, but no taxes are owed upon withdrawal during retirement.

Source: JP Morgan Guide to Retirement (page 45)

Additionally, by working with one of our advisors, we can assist in recommending an appropriate asset allocation strategy for your retirement funds, based on your risk tolerance and investment goals. Another benefit of participating in a company’s 401K plan is that many employers will match contributions up to a certain amount – this provides an excellent incentive to save more and get the maximum benefits from the plan.

College Savings Plans

Regarding college savings plans, 529s are the most popular vehicles due to their tax advantaged nature. Contributions to these plans are made with after-tax dollars, but the earnings grow tax-free and can be withdrawn tax-free when used for qualified higher education expenses. Additionally, many states offer tax deductions or credits for contributions to a 529 plan, making it an even more attractive option for millennials looking to optimize their cash flow. The WAM team can help facilitate the establishment of 529 accounts to ease the burden of increasing educational costs.

Tax Mitigation Strategies:

Young professionals face unique financial challenges, and it is important to understand the best strategies for managing their money. One of the most important financial strategies for millennials is tax mitigation. Tax mitigation strategies include utilizing a Roth IRA, taking full advantage of their mortgage, and utilizing other applicable tax credits/deductions.

Roth IRA

In addition to the benefits above, if you have a Roth IRA for more than five years, there are no taxes or penalties when withdrawing earnings for a first-time home purchase, up to $10,000.

Tax Loss Harvesting

Tax loss harvesting is an effective way for investors to reduce their taxable income by selling investments at a loss in order to offset any realized gains from appreciating investments. In a year characterized by stock market losses, you may find that there are few opportunities to offset gains in your investment accounts. If that is the case, you can still utilize the lax loss carry-forward which will allow you to offset capital gains in future years. Alternatively, the IRS allows an individual to use $3,000 of capital losses per year to offset ordinary income. This technique can assist in tax mitigation throughout your lifetime if used properly.

Mortgage Deductions

Mortgage interest payments are deductible from your taxable income when filing taxes which can significantly reduce liability owed. This deduction applies to both primary residences (purchased or refinanced) as well as second homes such as vacation properties or rental properties that may generate rental income or be used for recreational use. If your home was purchased after December 15th, 2017 you are allowed to deduct interest on the first $750,000 of the mortgage. Additionally, if you have a HELOC you may deduct up to a max of $100,000 in interest.

Child Tax Credit

The Child Tax Credit is available for parents who have dependent children under the age of 17 living with them full time in the United States. The Child Tax Credit can be claimed up to $2,000 per qualifying dependent with half being refundable if certain criteria are met such as adjusted gross income (AGI). Additionally, if AGI exceeds certain thresholds, then this credit may be reduced or phased out completely.

Charitable Contributions

In a recent study conducted by Fidelity Charitable, they found that approximately 74% of millennials consider themselves philanthropists. With the future of philanthropy in the hands of the next generation, please refer to WAM’s Guide to Giving to learn about the most tax-efficient ways to maximize charitable contributions to influence the world in a positive way.

Estate Planning:

Millennials are the largest generation in the United States, and it is important for them to start planning for their future. An estate plan is one of the best ways to ensure their wishes are followed and their assets are handled appropriately in the event of their death or incapacity. A comprehensive estate plan should include a trust, will, power of attorney, and health care power of attorney.

Trust

A trust is an important document to have in an estate plan. It can be used to protect assets, provide for minor children, and manage assets in the event of incapacity or death. Assets that are listed within the trust will avoid probate court, saving your family members valuable time and expenses. There are several types of trusts all with varying implications.

Will

A will is another important part of an estate plan. It allows a person to designate beneficiaries, provide instructions for how and when beneficiaries receive assets, and can name guardians for minor children.

Power of Attorney/Health Care Power of Attorney

A power of attorney and health care power of attorney are also important documents to have in an estate plan. A power of attorney allows a person to appoint someone to manage their finances and legal affairs in the event of their incapacity. While a health care power of attorney is a document that allows an individual to designate someone to carry out their health care directives in the event of incapacity.

These four essential documents are important because they allow you to specify what you want to happen to your property and assets after you pass away. These documents can also help to protect your loved ones and ensure that your wishes are carried out according to your specifications. Without these documents, your property and assets may be distributed according to state law, which may not be in line with your wishes. Additionally, estate planning documents can help minimize taxes and other expenses and can provide guidance to your loved ones during a difficult time.

Why Work with a Weatherly Advisor:

Younger investors are looking for ways to manage their cash flow, make sound investment decisions, and protect their wealth. Working with our experienced professionals at Weatherly can help achieve these goals efficiently.

Advisors can help young professionals optimize their budget, save and invest, and provide tailored advice on tax mitigation strategies, such as understanding deductions and knowing which tax credits apply in different scenarios. Financial advisors can also help young families create realistic estate plans that prioritize their goals while minimizing the potential impact of taxes or other liabilities.

Learn more about our services and how our customized approach may benefit you or your family:

https://www.weatherlyassetmgt.com/our-services/

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

As we welcome the beginning of fall with the start of September, here at Weatherly we are already sipping on pumpkin-flavored drinks and preparing for year-end planning conversations with our clients. To assist your team of advisors in giving the best advice as well as employing the most opportune investment strategies, we often request a few documents from you. In this month’s blog, we’d like to highlight important documents and how they help your advisors in tailoring advice specifically to you.

2020 Tax Return and Asset Allocation Review

- Having your tax return on file is helpful for many planning strategies but is especially important when factoring in any unrealized gains and losses for the year. As we look to de-risk portfolios, reduce concentration risk and rebalance taxable accounts, we like to account for capital gains and how this may impact your marginal tax bracket. Remember – capital gains are an indication your account has seen good growth and often are necessary to ensure we have room to incorporate new investment themes into your portfolios.

- We also welcome any other tax related items you think our team might find helpful for year-end planning – this could include a summary of your income year-to-date so we can offer advice on tax mitigation strategies like retirement and charitable contributions.

Charitable Opportunities

- There are many ways to give to charity with two-fold benefits – donating to organizations you are passionate about and reducing your tax liability. Your team of advisors can discuss what options are available to you each year given your unique circumstances.

- If any qualified chartable distributions (QCDs) still need to be made from your IRA or if you’d like to donate directly from your Donor Advised Fund (DAF), please let your advisor know which charity or charities you would like to donate to.

Contributions to Retirement Accounts

- Many retirement plans like employer-sponsored 401ks and self-employed 401ks have a year-end deadline for making contributions. You can view this year’s contribution limits on our Key Data Chart – our advisors are here to help you review your options and funding methods.

Updated Estate Documents

- Given the potential changes to tax and estate laws, this year provided many people the opportunity to update their estate documents, including trusts, wills, etc. We wrote about 5 estate planning strategies to consider earlier this year.

- If we do not have an updated copy of your estate documents, please post them to our secure portal for our records. If you are not sure whether we have your estate documents on file, please let us know and we will be happy to check our records for you.

Information to Update or Add Beneficiaries

- It is essential to have beneficiaries on all your accounts to avoid assets going through the cumbersome probate process if you were to pass, as highlighted in this article. Our team does periodic audits of our accounts to ensure there are beneficiary designations, and your designations should be reviewed annually or when you face big life changes.

- If you need to update your beneficiaries or add any beneficiaries, please email your advisor. If we need any birthdays or social security numbers, we ask you to please upload a document containing that information to our portal.

Year-End Gifting

- As your assets grow and accumulate, you may want to consider gifting to kids or grandkids. The annual gift limit for 2021 is $15k per person, per beneficiary; as a couple you can gift $30k per beneficiary.

- There are many ways to provide additional gifting above the annual exclusion – the blog post we highlighted above touches on these alternatives. You may want to talk to your advisor about strategies that pique your interest and how we engage in the family conversation.

Documents Supporting Upcoming Transfer of Asset (TOA) Opportunities

- We provide our best advice when we have your full financial picture available. If you have any large asset transfers in your immediate horizon, such as a home sale, an inheritance, or wish to transfer a significant amount of money into or out of your portfolio, please provide that information to your advisor and post any related information to our portal. This information also helps us to provide guidance on how to invest future assets and implement tax planning strategies like those outlined above.

CIRAL – Client Information Release Authorization Form

- Our team is working towards acquiring all our clients’ personal and professional contacts in preparation for an unexpected event. We request our clients to fill out and return our Client Information Release Authorization Letter (CIRAL). This form, which can be downloaded here, outlines the contacts whom we can reach out to in the event it is necessary. If you have already submitted your CIRAL but wish to change your contacts, we welcome an updated version at any time. Similar to your beneficiaries, this should be reviewed annually.

Cyber security is always top of mind here at Weatherly. When supplying our team with forms and documents, please utilize our secure portal. You can also use our portal to view your accounts and statements at any time, anywhere.

If you do not currently have a portal and would like to get set up with one, please email us and we will be happy to do so. If you need assistance downloading documents from our portal or posting documents, please see our handy portal help PDF that will walk you through the steps. We are also available to answer any questions as they arise via phone or email.

The holidays can be stressful and year-end planning can seem overwhelming, but your Weatherly team is here to help make your financial picture something you do not need to worry about. Cheers to a pleasant autumn and a festive fourth quarter of 2021!

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

Over the past year we’ve had many phrases added to our lexicon – social distancing, flatten the curve, Zoom fatigue, and many others.

For every “can you hear me?” or “you’re on mute” we’ve heard, we’ve also felt concern and hope for our collective communities.

In March of 2020, we were told to shelter-in-place and now twelve months in, we are optimistic about broader re-opening in the near future while the WAM team continues to operate in a hybrid model. The rapid rate at which governments, businesses and scientists worked together to develop and administer a global vaccination is unparalleled.

We wanted to share this blog to keep you up to date on Spring happenings at Weatherly.

Updates on Taxes:

2020: The recent 2020 tax year was unlike any other, with strategies like Roth Conversions and skipping Required Minimum Distributions applying to many of our clients. We’ve found this tax guide as well as this article helpful in highlights the changes that may apply to your unique situation.

The IRS extended the deadline to file for the 2020 tax year to May 17th; taxpayers do not have to take any action to take advantage of the extended deadline. The deadline to make a Q1 estimate remains April 15th.

Prior to filing, you may be eligible to contribute to IRAs (Traditional, Non-deductible, SEP and Roth) or make an employer contribution to a Self-Employed 401k. Our 2020 and 2021 Key Data Chart may be useful in determining the limits that apply to you.

Custodians have rolled out most tax forms at this juncture, and our team has been providing to clients and tax professionals securely. Please let us know if there is anything we can provide for your tax filing, and as always we appreciate a secure copy when completed.

2021: The Biden Administration has been busy working on the $1.9 Trillion stimulus plan, known as the American Rescue Plan passed last week, to aid in boosting the economy and supporting those most impacted by the pandemic.

The American Rescue Plan outlines short-term solutions to aid the economy, however President Biden is now focusing on long-term economic plans and modifying the tax code to help close the funding gap. Bloomberg highlighted the first major tax hike since 1993 in this article, with a focus on raising the corporate tax rate, raising the income tax rate on those earning more than $400,000 and expanding the estate tax reach.

Our team of advisors are available to discuss planning opportunities and how the potential tax bill may impact you and your family.

Updates on Our Team:

The Weatherly team continued to learn and grow over the last year, despite the challenges that were presented working and living in a remote environment.

Aubrey Brown, one of our Wealth Management Associate Advisors, completed his Master of Science Degree in Personal Financial Planning through the College for Financial Planning (CFFP) in 2020. Aubrey continues to develop his expertise in planning for clients.

Yoshi Brownlee, our Team Administrator and Marketing Specialist, obtained a Professional Certificate in Marketing offered through SDSU’s College of Extended Studies and One Club San Diego in September 2020. Yoshi continues to work with the Partners to develop the Firm’s marketing initiatives.

We also onboarded Andrea Taylor as a Wealth Management Associate in February. Andrea’s 4 years with Ernst & Young in audit and accounting coupled with a Masters of Science in Accountancy will augment our team of professionals.

Weatherly in the News:

We have many exciting updates on our the Weatherly Newsroom.

In the March 13th edition of Barron’s, Carolyn was named as a Top 1200 Advisor. She was also listed as one of Forbes 2021 Best-in-State Wealth Advisors.

Carolyn, Brent Armstrong, Kelli Ruby and Ryan Richardson were also named 2021 Five Star Wealth Managers.

Our team is proud of what we have accomplished over the past 26+ years and being able to serve our clients during a global pandemic. Weatherly also surpassed $1 Billion in assets under management at the end of 2020.

ADV and Privacy Policy:

On an annual basis Weatherly Asset Management (WAM), as an SEC Registered Advisor, is required to deliver the following documents to all of our clients either electronically or by US mail; please see attached:

Part 2A of Form ADV (the Firm Brochure)

Part 2B of Form ADV (the Brochure Supplement)

If you have opted for hard copy delivery of compliance communications, you will be receiving these in the mail in the coming weeks. These documents have also been posted to all client portals for future reference.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

Daily life changed globally and permanently due to the COVID-19 virus, and at Weatherly we have adapted to the dynamic landscape in multiple ways. While our team has been mostly working remote since mid-March, we are still running business as usual and are implementing a variety of tools to make Weatherly a safer and more socially responsible workplace.

During this uncertain time, we know that communication is paramount which is why we have increased our email blast frequency to twice a month to capture ongoing strategy changes, as well as market updates. If you are not already included on our email list and would like to be, please sign up for our mailing list by filling out this contact form.

Like many businesses, we transitioned to calls and virtual meetings in March for the safety of our clients and team. While in-person meetings are not a possibility at this time, WAM has utilized GoToMeeting for video conferencing for a number of years. This tool not only allows us to communicate more effectively while in different locations, we also have the added benefit of using the screen sharing and presentation capabilities. Our advisors can walk through your client reports with you by page, access your custodian’s website, or demonstrate how to get onto your secure Weatherly portal. This is especially useful during tax time, when you or your CPA upload tax documents for your advisor to analyze. Whatever the task, our advisors can virtually be right by your side to accomplish it. If you are interested in setting up a quarterly review, or secure portal training session via GoToMeeting, please do not hesitate to reach out to our team. We would be happy to help you get set up.

Working remotely has given us the opportunity to tap into the depth of Microsoft’s productivity software offerings. Microsoft’s secure remote access and communication tools have been crucial for our team internally. Through the security and usability of Teams, SharePoint and other communication software, our team has been able to stay on the same page while also providing service in a timely manner. Another tool that has made remote work possible is the secure utilization of DocuSign. We have been diligent in using DocuSign whenever possible for its environmental and convenience benefits, but it has now become essential in allowing business to continue seamlessly while also remaining distant.

One thing that hasn’t changed throughout this transition to remote work is Weatherly’s commitment to protecting your data. Cybersecurity has and always will be a main priority of our business. Our client and team communications remain secure with the use of the Weatherly portal, DocuSign and apps that encrypt and password protect physical documents. We have increased our use of apps like GeniusScan to allow for secure scanning and sharing of internal records. As more innovative technologies emerge, we are continuously evaluating which tools offer our clients the most optimized experience.

In preparation for our team’s gradual return to the Weatherly office, we are focusing on safety first by implementing more extensive safety measures. We have added hands-free soap and hand-sanitizer dispensers and increased frequency and depth of our cleaning program. We are also in the process of installing tempered glass barriers between workspaces to create more physical boundaries once we can work in the office together safely. While we are not resuming in person meetings at present, we hope these changes will make you feel more comfortable coming into our office when it is safe to do so.

Under normal circumstances, our team prides itself on our boutique atmosphere and face-to-face communication style. The quarantine has provided us with a unique opportunity to discover new ways to connect with each other and our clients. To maintain our spirit of team collaboration, we participate in daily team video calls to touch base on day-to-day activities as well as ongoing projects and progress on larger firm strategy initiatives. Now more than ever, the importance of staying connected is critical.

As we navigate this new “normal,” we work hard to remind each other that while times are uncertain, we can be confident in our ability to adapt and remember to have a laugh or two as we grow in this new environment. While nothing can take the place of sitting right across from a coworker and catching up, we work to bring our workplace culture into our remote environment through weekly team-building activities, exchanging songs we are listening to and sharing recipes tried over the course of the stay at home order. We are excited to share our team cookbook and quarantine playlist with you. We hope this inspires you and your family to find creative new ways to stay connected while staying at home. Check out the links below for our collaborative playlist and cookbook!

Read our Weatherly Cookbook here

Listen to our WAM Quarantine Playlist here

While the crisis is ongoing and our interactions may look a bit different these days, the team at Weatherly remains committed to providing an elevated client service experience for you and your family. We look forward to seeing you in the office again soon but for now please stay healthy and stay safe.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

There seems to be a new pattern emerging, another year and another tax overhaul. On December 20, 2019 President Donald Trump signed into law the Setting Every Community Up for Retirement Enhancement Act, better known as the SECURE Act, as part of the government’s new spending bill which will inevitably affect most retirement savers for better or worse. While the Act is quite extensive, we plan to focus on the key provisions most likely to affect you and your loved ones effective January 1, 2020:

- Changes effecting retirement plan beneficiaries

- RMD pushed to age 72

- Traditional IRA Contributions

- Qualified Charitable Contributions (QCD)

Removal of the “Stretch” Provision

Perhaps the most impactful change resulting from the SECURE Act is the elimination of the “stretch” provision for most non-spouse beneficiaries of inherited IRAs and other retirement accounts. Under the prior law, for those account owners who passed away prior to December 31, 2019, their non-spouse beneficiaries were able to “stretch” Required Minimum Distributions over their life expectancy, or in the case of a qualifying trust, over the oldest applicable trust beneficiary’s life expectancy.

Moving forward, for most non-spouse beneficiaries who inherit a retirement account in 2020 and beyond, the “10 Year Rule” applies. This new rules states that the entire inherited retirement account must be emptied by the end of the 10th year following the year of inheritance. Beneficiaries do have flexibility as to the timing and quantities of the distributions to help with the tax impact as long as the account has been depleted by the end of the 10th year.

While the elimination of the “stretch” provision will affect a significant portion of beneficiaries, there are a few groups deemed “Eligible Designated Beneficiaries” that will not be subject to the new legislation:

- Spousal Beneficiaries

- Disabled Beneficiaries

- Chronically Ill Beneficiaries

- Individuals who are not more than 10 years younger than the decedent

- Certain minor children of the original account owner, but only until they reach the age of majority. Age of majority follows state rules and thus will vary.

For these “Eligible Designated Beneficiaries”, the same rules that applied prior to the SECURE Act will continue.

The SECURE Act has not only changed the rules and requirements of individual beneficiaries but may also lead to significant changes where trusts are named as the beneficiary of a retirement account. In general, there are two different types of trusts that would be set up as a beneficiary of a retirement account, a Conduit “See-Through Trust” or a Discretionary Trust, and both types could have unfavorable outcomes as a result of the Act.

Many Conduit trusts are drafted in a manner that only allows for the RMD to be disbursed from an Inherited IRA, with a subsequent amount passed directly to the trust beneficiaries. With the amendments made by the SECURE Act, for those beneficiaries of trusts who do not fall under this new classification of “Eligible Designated Beneficiaries” and thus subject to the 10-year rule, there is only one year in which there is an RMD, the 10th year. This has the potential to lead to an unfavorable tax situation in which the entire account balance is ultimately distributed to the beneficiaries in the final year.

On the other hand, Discretionary Trusts don’t fare any better than the Conduit Trust. The reason for this is because Discretionary Trusts are typically drafted in such a way as to retain a portion if not all income and distributions within the trust. As such, any income or distributions that are retained in the trust are taxed at the maximum rate of 37% after just $12,950 of income. So, there is the possibility of not only the entire account balance having to be distributed by the 10th year but also the unfavorable trust tax rates if not distributed to the beneficiaries.

Now we intentionally said, possibility , because the IRS has not clearly outlined whether the Conduit or Discretionary Trusts that have an “Eligible Designated Beneficiary” of a spouse, minor child, or beneficiary within 10 years will “See-Through” to these beneficiaries and not be subject to the new SECURE Act rules. The Act does specifically provide guidance that such trusts can be treated as an “Eligible Designated Beneficiary” when the beneficiary of the trust is a disabled or chronically ill person. We will need to await further guidance from the IRS for a final ruling on other groups of “Eligible Designated Beneficiaries”.

Most retirees will not be affected by the change in Required Minimum Distribution (RMD) starting age, however, it is important to mention for those who are about to take their first RMD. The SECURE Act has changed the age an individual must begin taking RMD’s from 70 ½ to 72. So how do you know when you are supposed to begin taking your RMD if you turned 70 ½ in 2019 or will turn 70 ½ in 2020?

2019

For those individuals who turned 70 ½ years old in 2019, you will be required to take your first RMD by April 1, 2020. If you have already begun taking RMD’s in previous years, these changes will have no material effect on your RMD withdrawals.

2020 and beyond

For those individuals who are turning 70 ½ on January 1, 2020 and beyond (i.e. those individuals born after June 30th 1949), will not be required to take their first RMD until April 1 of the year following the year in which they turn 72. This isn’t a huge change but even one or two years of additional growth and contributions can be quite impactful on retirement accounts.

Another major change resulting from the SECURE Act is the elimination of the age limit for traditional IRA contributions. Under current law, Traditional IRA contributions are NOT allowed after 70 ½. However, the new act lifts this age limit and allows contributions past 70 ½ if there is earned income (Roth IRA’s have never had contribution age limits). With the new change, Traditional IRA’s are now aligned with the rules for Roth IRA’s and other retirement accounts.

Married couples filing their taxes jointly, can continue to contribute to their Traditional IRA as well as continue to make spousal IRA contributions for a spouse that is no longer working.

Qualified Charitable Contributions (QCD)

With RMD’s being pushed to age 72 and extension of IRA contributions, it would seem that QCD’s would follow suit, but in fact there were no changes to the rules. Individuals will continue to be able to utilize their IRA or Inherited IRA to make a QCD beginning at age 70 ½ and gift up to $100k per year. This will allow the individual to make the charitable contribution directly on a pre-tax basis. Beginning in the year an individual turns 72, any amounts given to charity via a QCD will reduce the then necessary RMD as well.It is important to note that post 70 ½ contributions will reduce any future QCD’s by an equivalent amount.

Additional Changes

In addition to the changes that we have covered thus far, below are a few other notable changes that have been introduced as part of the SECURE Act.

- A penalty-free distribution from a retirement plan prior to age 59 ½ for a qualified birth or adoption up to a lifetime limit of $5,000

- Medical expense deduction AGI hurdle rate of 7.5% extended for 2019 and 2020

- A repeal of the TCJA-introduced Kiddie Tax changes (reverting away from a requirement to use trust tax brackets and back to using the parents’ top marginal tax bracket).

- Reintroduction of the qualified higher education tuition deduction. Allows for up to $4,000 of qualified tuition to be used as an above line deduction

- Mortgage Insurance Premium Deduction: May continue to deduct premiums. AGI phaseouts begin when AGI exceeds $100k MFJ or $50k MFS

- 529 plans are now permitted to use up to a $10k lifetime amount for apprenticeship and repayment of student loans

- Employers may adopt plans that are entirely employer funded, such as stock bonus, pension plans, profit sharing plans, and qualified annuity plans, up to the due date (including extensions) of the employers return

How Weatherly can help:

- Review your beneficiaries

- Discuss your RMD distribution schedule

- Estate planning considerations for IRA beneficiaries

Useful links

https://www.irs.gov/pub/irs-drop/n-20-06.pdf

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

According to a 2018 study conducted by Personal Capital, the top two stressors in relationships were: 1) Money at 54% and 2) Communication at 26%. Money was at the top of the list across Millennial, Gen Xers, and the Boomer generations. With these stats, we have created a “How to Navigate Finances as Yours, Mine, and Ours” guide when broaching the topic of finances in a relationship.

Monthly Nut

Our Monthly Nut Chart serves as a great conversation starter on the taboo topic of money for couples navigating joint finances for the first time. We suggest each partner complete their separate Monthly Nut to grasp where each other financially stands before tackling your joint financial picture. The “Yours and Mine Monthly Nut Charts” helps shed light on spending or savings habits, debt to asset ratios, and earnings potential of each party. You may find that one individual has more debt than the other. This scenario is not uncommon and may make combining finances even more challenging or in some cases, less appealing. We encourage couples to come up with a plan to pay down that debt by considering: Who is responsible for paying down the debt- the individual, jointly, a combination of both? The charts can also assist couples explore their tax filing options. Married couples may find their state taxes may be lowered by filing separately even if they file jointly at the Federal level. Weatherly is here to help navigate this conversation with your CPA as appropriate.

Once you have a better understanding of each other’s financial situation, you can better focus on building out your financial plan as a couple.

Prioritize for Progress

Create a list of items, big or small, you would like to accomplish with your finances in the short-term, mid-term, and long-term. Your list might include: pay the rent, travel once a year, pay off an auto loan or student debt, buy a home, save for a child’s college or your retirement, have $1mm to pass to the next generation. Once you have your list, sit with your partner and prioritize for progress. If you and your significant other do not see eye to eye on a specific goal or it is specific to you personally- come to an agreement that works for both parties. Maybe you have your own separate debit card/credit card, bank account or investment account to utilize for your specific goal and joint accounts to accomplish your goals as a couple. Please reference this Wall Street Journal article that addresses these topics in further detail.

Retirement Planning

Saving for retirement poses several challenges as some individuals tend to view this bucket of money as yours or mine strictly because of who earned it. To better accomplish your retirement goals as a couple, it is important to:1) understand each other’s views on retirement and 2) recognize that earnings potential may fluctuate as life changes. As highlighted in the “Yours and Mine Monthly Nut Charts”, one partner may be inclined to maximize retirement while the other prefers to spend. Alternatively, one individual’s earnings potential may change because they stay home with the kids, which decreases their ability to save for their own retirement. Viewing retirement savings as “Ours” versus “Yours” or “Mine”, couples typically avoid unnecessary conflict and can focus on saving for Their retirement.

Investments

It may take time to establish an investment philosophy as a couple and that is okay. The key is to build and evolve it into what works for you together. Some items to consider in formulating your investment approach:

- Different Risk Tolerances: Consider separate accounts with each other named as the beneficiary for differences in risk tolerance.

- Who will manage investments and bill pay: Designating one partner as the sole investment manager, can feel like a loss of control for the other. Consider separate individual accounts “Fun” accounts to accommodate.

Estate Planning and Community Property

You know the old joke for married couples – “what’s mine is mine and what’s yours is mine?” While the intent is for this to be humorous, it can be true for assets and debt accumulated during marriage in states that adopt community property laws, like California. It’s important to consider assets that each individual acquired prior to marriage, earnings and income potential and future inheritance; and if individual assets should be designated as Separate Property. This is seen commonly with inherited assets, when a parent designates their individual child (not the couple) as a beneficiary.

There are complex situations that should be addressed prior to marriage – for example, if one spouse owns and runs a business and the other stays home to run the household. While the contribution to the family is similar, the earnings potential varies greatly.

With an increased focus on the value of intangible assets – like intellectual property – new business ideas and student debt among the Millennial Generation, attorneys are seeing more young couples request a pre-nuptial agreement. While it’s a tough discussion to have, the conversation prior to marriage could alleviate stress and attorney fees down the line if divorce occurs. Recall in Community Property states, debt accumulated during marriage can be a 50/50 responsibility even if divorce occurs.

Beneficiary Updates and Wills/POAs

There are 3 basic estate documents that every adult, regardless of marital status, needs:

- Will – designates who will get your assets upon your passing

- Financial Power of Attorney – designates who can access your financial records and bill pay

- Healthcare Power of Attorney and HIPAA Waiver – designates who can speak with your doctors and access your healthcare records

Newly married couples should review these documents – or work with an attorney if they haven’t already created them – to determine who should be named.

Beneficiary reviews are also important – you may have a sibling, family member or friend listed as the beneficiary of old workplace 401ks, current retirement plans or IRAs. Any pension plans should also be reviewed; most offer survivorship benefits to spouses.

As your assets and estate grow, you may consider creating a Family Trust for Community Property assets and/or a Separate Property Trust for individual assets.

Families with young children should also have the discussion of who would take care of your children or act as custodian of your assets if something happens to you. We touched on other considerations for young families in a previous blog post.

How Weatherly Can Help

Marriage is exciting and these areas of discussion shouldn’t feel daunting. Talking through tax, estate and financial discussions and recommendations with your advisor can alleviate concern and “what if” scenarios so you and your spouse can focus on building your lives together. We welcome a dialog on how we can provide guidance on a successful financial future for your family.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

In the world of Wealth Managers, Stock Brokers, Robo-Advisors and Financial Planners, investors are often left wondering which one is right for them, and why? Each individual, family or business’ situation is different and the goals unique. So where does Weatherly fit in? Weatherly would fall into the category of ‘Wealth Manager’ and our goal is to positively influence your financial life through dialog and collaboration. The more we learn about you, the more we adapt and customize our advice for impact.

The two main pillars of our mutual success are Financial Planning and Investment Management. Financial Planning is the foundation of our relationship where we learn what makes you tick both personally and professionally. Those fascinations and desires shape your goals and how you would like your money to work for you. Armed with this information we can strategize prudent asset allocation, timing of retirement, make estate planning decisions, provide for beneficiaries or charities to name a few.

Click here for more information on our services

Investment Management is the implementation of what we learn through the Financial Planning process. There is no point trying to fit a square peg through a circular hole, or utilize a ‘cookie cutter’ approach. We want to make sure your portfolio aligns with your long-term plan with tax and fee efficiency. This is the stuff that we wake up in the morning for.

In this blog, we explore the diverse personalities and expertise on our team, and how we most enjoy working with clients. While everyone has their core day to day functions in how they help the team, and ultimately you, we will also shed some light on how they contribute in a more non-conventional fashion as well. Feel free to click on any team member’s name to check out their biography. Welcome to behind the scenes at Weatherly!

The first smiling face you see when walking into the office or joyful voice that greets you over the phone is none other than Yoshi Brownlee. Yoshi plays an integral role at the firm facilitating organizational efficiencies and administrative support for both clients and advisors. She also helps the firm with its philanthropic initiatives by identifying where a need in the community is and organizing the logistics to get the team together to help out. This can be seen on our Culture and Community page of the website that she helps maintain for us. One item you can’t quantify is her positive attitude and overall demeanor that keeps the office morale high, even during tax season…

The first smiling face you see when walking into the office or joyful voice that greets you over the phone is none other than Yoshi Brownlee. Yoshi plays an integral role at the firm facilitating organizational efficiencies and administrative support for both clients and advisors. She also helps the firm with its philanthropic initiatives by identifying where a need in the community is and organizing the logistics to get the team together to help out. This can be seen on our Culture and Community page of the website that she helps maintain for us. One item you can’t quantify is her positive attitude and overall demeanor that keeps the office morale high, even during tax season…

Chrissy is a little more behind the scenes, but her work is definitely felt throughout the entire ecosystem. Her primary roles include working on client onboarding systems, internal reporting, and automation of workflow. As you know, we are always trying to make sure we have your most recent tax documents and Chrissy is the one who makes sure that they accurately stored and that we capture any important data such as loss carryforwards so they are utilized for tax efficient investing. She makes sure to be a team player and will actively look to anticipate needs not just for the office as a whole but her fellow team members.

Chrissy is a little more behind the scenes, but her work is definitely felt throughout the entire ecosystem. Her primary roles include working on client onboarding systems, internal reporting, and automation of workflow. As you know, we are always trying to make sure we have your most recent tax documents and Chrissy is the one who makes sure that they accurately stored and that we capture any important data such as loss carryforwards so they are utilized for tax efficient investing. She makes sure to be a team player and will actively look to anticipate needs not just for the office as a whole but her fellow team members.

Sally has been instrumental in leading the push toward creating a more efficient workflow process including the firm-wide adoption of DocuSign and draws upon her educational background to help teach the team and clients new efficiencies in the technology we utilize. DocuSign has greatly increased execution time on client accounts, led to a more secure form of communication, and is more easily tracked. She was probably more excited with the amount of paper that we are savings rather than the efficiency created. Sally is very passionate about sustainability and never misses an opportunity to remind us about the silverware in the cupboard or compliment us when using it.

Sally has been instrumental in leading the push toward creating a more efficient workflow process including the firm-wide adoption of DocuSign and draws upon her educational background to help teach the team and clients new efficiencies in the technology we utilize. DocuSign has greatly increased execution time on client accounts, led to a more secure form of communication, and is more easily tracked. She was probably more excited with the amount of paper that we are savings rather than the efficiency created. Sally is very passionate about sustainability and never misses an opportunity to remind us about the silverware in the cupboard or compliment us when using it.

Ryan’s time and experience here with the firm has allowed him to gain exposure to just about all aspects of the business. He has fulfilled many roles within the company over the years and is very flexible in his capabilities. You may have had the pleasure of speaking with him if you were moving some accounts over as he has taken on the Transfer of Assets process. He obtained his CFP® designation last year so make sure to congratulate him on this amazing accomplishment as he sacrificed many weekends to achieve this.

Ryan’s time and experience here with the firm has allowed him to gain exposure to just about all aspects of the business. He has fulfilled many roles within the company over the years and is very flexible in his capabilities. You may have had the pleasure of speaking with him if you were moving some accounts over as he has taken on the Transfer of Assets process. He obtained his CFP® designation last year so make sure to congratulate him on this amazing accomplishment as he sacrificed many weekends to achieve this.

One of Brooke’s many duties is helping clients accomplish their charitable goals, which includes analyzing and helping clients understand which account and position is best suited for gifting along with the taxable implications coming from such gifts. As some of you may have had the privilege to work with Brooke you will notice she is an incredible teacher and has a way of breaking down material into simplified pieces that are easy to understand. Her charitable work is a perfect role for her as she also assists with the firm’s initiative to be more involved in the community though philanthropic events such as beach cleanups, Feeding San Diego, and the Susan G. Komen breast cancer walk, which she has personally participated in. Another congratulations is due for Brooke as she too recently obtained her CFP® designation.

One of Brooke’s many duties is helping clients accomplish their charitable goals, which includes analyzing and helping clients understand which account and position is best suited for gifting along with the taxable implications coming from such gifts. As some of you may have had the privilege to work with Brooke you will notice she is an incredible teacher and has a way of breaking down material into simplified pieces that are easy to understand. Her charitable work is a perfect role for her as she also assists with the firm’s initiative to be more involved in the community though philanthropic events such as beach cleanups, Feeding San Diego, and the Susan G. Komen breast cancer walk, which she has personally participated in. Another congratulations is due for Brooke as she too recently obtained her CFP® designation.

You may know or think of Cole as the money man and is often times the one you speak to when you request some cash as he handles a majority of the firms cashiering requests. He also ensures that you get your money even when you don’t ask for it by running Required Minimum Distributions or Qualified Charitable Distributions analysis so that you can maximize tax efficiency. As for professional milestones, he recently passed Level III of the CFA Program in 2018B03. Outside of work he has been steadily training for the Orange County Marathon that he completed last week. This was a huge personal accomplishment for him and now he sets his sights on competing in a triathlon.

You may know or think of Cole as the money man and is often times the one you speak to when you request some cash as he handles a majority of the firms cashiering requests. He also ensures that you get your money even when you don’t ask for it by running Required Minimum Distributions or Qualified Charitable Distributions analysis so that you can maximize tax efficiency. As for professional milestones, he recently passed Level III of the CFA Program in 2018B03. Outside of work he has been steadily training for the Orange County Marathon that he completed last week. This was a huge personal accomplishment for him and now he sets his sights on competing in a triathlon.

Chase is the newbie to the Weatherly team and comes from a nationwide financial planning software company. He was there for about 5 years and primary dealt with helping advisors model out their strategies and plans for their clients. He will draw largely on this background as he helps with building and presenting the financial plans here at the firm. This will be an exciting new perspective to work first hand with both the advisors and clients alike. He looks forward to officially introducing himself to you all and working side by side in the coming future.

Chase is the newbie to the Weatherly team and comes from a nationwide financial planning software company. He was there for about 5 years and primary dealt with helping advisors model out their strategies and plans for their clients. He will draw largely on this background as he helps with building and presenting the financial plans here at the firm. This will be an exciting new perspective to work first hand with both the advisors and clients alike. He looks forward to officially introducing himself to you all and working side by side in the coming future.

The team here would certainly not be able to run as smoothly as it does if it wasn’t for the resourcefulness of Lindsey. She wears many hats here including HR, IT, and security, to name a few, all while having a very calm and laid-back attitude, which is hard to fathom with all those responsibilities. On top of all of these items here in the office she is also a mother of two young beautiful children. We are certainly thankful for all her efforts here and being able to wear so many different hats. Her capabilities allow us each to focus on our unique expertise with clients and keep client data safe.

The team here would certainly not be able to run as smoothly as it does if it wasn’t for the resourcefulness of Lindsey. She wears many hats here including HR, IT, and security, to name a few, all while having a very calm and laid-back attitude, which is hard to fathom with all those responsibilities. On top of all of these items here in the office she is also a mother of two young beautiful children. We are certainly thankful for all her efforts here and being able to wear so many different hats. Her capabilities allow us each to focus on our unique expertise with clients and keep client data safe.

Kelli recently passed an amazing milestone and is the newest partner here at the firm. Outside of meeting with clients, she also helps assist in the marketing effort of the firm. This consists of helping create our own story here at Weatherly along with listening to you, the client, for new ideas as to what type of educational blog posts we should explore. She also assists with the firm in staying compliant by updating any related documents or disclosures we have and working with the other partners to develop company strategy.

Kelli recently passed an amazing milestone and is the newest partner here at the firm. Outside of meeting with clients, she also helps assist in the marketing effort of the firm. This consists of helping create our own story here at Weatherly along with listening to you, the client, for new ideas as to what type of educational blog posts we should explore. She also assists with the firm in staying compliant by updating any related documents or disclosures we have and working with the other partners to develop company strategy.

Brent’s role as partner includes oversight of investment implementation and he prides himself on being able to simplify and synthesize complicated matters into digestible pieces for clients and fellow team members to understand. He plays an integral role on the investment committee and handles a majority of the firms trading and analysis. His laid back attitude and sense of humor makes him a joy to work with and somehow he maintains this even when taking care of the newest addition to his family throughout the night.

Brent’s role as partner includes oversight of investment implementation and he prides himself on being able to simplify and synthesize complicated matters into digestible pieces for clients and fellow team members to understand. He plays an integral role on the investment committee and handles a majority of the firms trading and analysis. His laid back attitude and sense of humor makes him a joy to work with and somehow he maintains this even when taking care of the newest addition to his family throughout the night.

Candise has been with Weatherly for over 19 years and we’re sure you either know her well or have spoken with her in the past. She continues to bring a tremendous amount of value through her past experience in the industry and particularly in cases involving estate matters and guiding clients through what can be a difficult process. Through open dialogue, it sets the stage for all parties involved to feel included and heard regardless off the outcome. As partner, she is an amazing educator and when answering questions she certainly makes sure you get all the information you were looking for… and even some you didn’t even know you needed!

Where do we begin. All of the different responsibilities that you have read prior to this are somehow touched and filtered through Carolyn. Her genuine and empathetic personality allows for her to connect to whoever she is speaking to and regardless of the situation. She spends most of her time meeting with clients and building relationships but coincides that with developing firm direction and strategy. It’s remarkable how much she can remember and is always able to ask specific details about how the family is doing or any exciting developments that have occurred. She continues to lead by example and make sure all clients and team members are looked after and treated with care.

Where do we begin. All of the different responsibilities that you have read prior to this are somehow touched and filtered through Carolyn. Her genuine and empathetic personality allows for her to connect to whoever she is speaking to and regardless of the situation. She spends most of her time meeting with clients and building relationships but coincides that with developing firm direction and strategy. It’s remarkable how much she can remember and is always able to ask specific details about how the family is doing or any exciting developments that have occurred. She continues to lead by example and make sure all clients and team members are looked after and treated with care.

We hope this sheds some light on our team and provides context on what goes on behind the walls at Weatherly.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

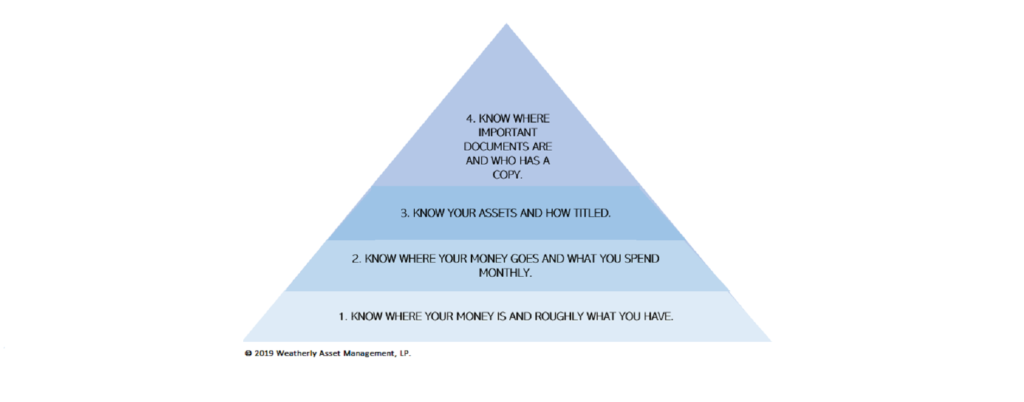

Over the course of working with clients for many years, we often get the question, “What are the most important financial elements you think we should know?” Although no two client situations are the same, clients often need a fundamental starting point to build their financial future upon. In the interest of starting the year off right, we want to highlight what we call “The Four Financial Basics” and important action items you can’t afford NOT to know for a healthy financial future.

“The Four Financial Basics” and considerations as you establish your financial base:

- Most importantly, know where your money is and roughly what you have.

Ask yourself the following questions:

- What are your sources of income and savings? What amount do you have of each?

- Income sources may include: pensions, social security, investment income, rental income, business income, salaries and wages, IRA distributions

- Where are your investment and retirement accounts held? How much do you have of each?

- Do you give to charity? Do you have a Donor Advised Fund (DAF) or another source you use?

- After considering these questions, Weatherly is able to provide guidance and strategies specific to your financial situation and to help maximize your after-tax income, savings, and investment.

- Know where your money goes and what you spend monthly.

- According to a recent Gallop study, approximately 67% of Americans do not keep a formal budget for their household spending (1). We recommend that clients track what they spend in various categories to avoid overspending. First add up the necessities, include housing costs, debt, other items such as car, insurance, utilities, savings. Then compare that to your income number to see what you have remaining. We have included a worksheet to help you track here.

- By gathering this information, we can better develop your financial plan and evaluate the amount of income you have left for discretionary spending on items such as: travel, entertainment, and hobbies to name a few- as well as better estimate what you will need throughout your life.

- Know Your Assets. How are they titled, where are they held?

- The title and type of asset determines how it is treated. A common example is your home- if you have a living trust, but your home is not in trust title, then your home will not be treated as being held in trust. This oversight may lead to a probate issue at death. Have you refinanced recently? Check your title is correct.

- Consider: Where is the title document for the asset? What does it say? Who has a copy of it? Have you developed a list so an executor would know where everything is?

- This exercise is akin to a good financial health checkup. Weatherly encourages clients to “Know Your Assets” to avoid unnecessary pitfalls, such as the probate example outlined above.

- Know where important documents are and who has a copy.

- Important documents typically include your durable power of attorney, durable power of attorney for health care, trusts, wills, list of assets, insurance policies, benefit information, and tax returns.

- Use a simple checklist to track the documents you have and who has access to them. Review this list: 1) at least annually, 2) when you acquire new assets, or 3) if there are changes in family status due to birth, marriage, death, and divorce to name a few. Weatherly is available to help complete your checklist and collaborate with your team of professionals- CPAs, estate planning attorneys, a trusted family member- to implement or obtain copies of these documents on your behalf.

- Provide the important documents and completed checklist to your executor, trusted professional, or keep a copy in a known place “in case of emergency”.

- Completing our Family Conversation Card with a family member or significant other, can serve as an evaluation and accountability tool that helps track your documents and progress. You can also utilize the card as way to educate and start the family conversation about wealth, family values, philanthropy, and financial goals and wishes.

- For more detailed, complex lists we recommend storing on a secure thumb drive that is password protected, or a cloud-based storage system- such as Dropbox, Keeper, or Amazon Drive-which is accessible from anywhere. Some if these data storage systems also have legacy options for data recovery.

So, how did you do? Do you generally know the Four Financial Basics? Excellent! Does your spouse… your executor or trusted family member?

Similar to the start of a new year, establishing your financial base can present a plethora of emotions, challenges, unknowns, some anxiety, and excitement. The Weatherly crew is here to assist you with the Four Financial Basics and provide guidance as you seek to put your financial house in order and plan for the future.

Resources:

Resources:

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

One of the most exciting events in human life is the birth of a child or grandchild. While we can’t prepare you for the challenges of parenting, we can help with ways to get a head start on the financial and legal considerations that come with being a parent, grandparent or significant contributor to the family unit. In this month’s blog, we’ll outline some of the important steps that can be taken to promote a healthy financial future for young families.

1) Obtain Birth Certificate and Social Security Number (SSN): These documents are important and are required for some of the activities outlined below. They are typically received within a few weeks of birth and are important for enrolling in health insurance. For world travelers, getting a jump start on a US Passport or Global Entry identification as early as possible helps save stress and time before your next vacation. More information on obtaining a SSN can be found here.

2) Add your child to your health insurance: Most insurance companies will automatically cover your child for the first 30 days, but beyond that, you typically must add them to your plan. If you are a resident of California, you can find additional information here. If you are a resident of another state, take a look here.

3) Set up a will or trust: Wills and Trusts are already great tools to avoid probate and taxes, but they play an increasingly important role as the family grows. If something happens to you and your partner, the Trust will define both financial and legal guardianship for your child, and they don’t need to be the same person. For example, one party could become custodians and daily caretakers for the child, while another party could manage the finances for the child’s benefit. Trusts (such as a sprinkling trust) can also set parameters on what assets the child can access while a minor, or even as an adult as necessary. We have discussed wills and trusts in our previous blog post and the importance of each.

4) Review and change beneficiaries on your financial accounts: This is particularly important for retirement accounts where you typically name people, rather than a trust, as beneficiaries. A typical scenario would be to name your spouse/partner as the primary beneficiary, with your trust as the contingent to care for young children. We recommend checking with your advisor or estate planning attorney to see if you need to make changes to your current beneficiaries.

5) Adjust your W-4 form with your employer: The W-4 form lets you take allowances which adjust the tax withholding from your paycheck. The more allowances you take, the more take home pay you will receive. Often, children open up new tax breaks and you may not need to have as much money withheld from your paycheck as prior years. We suggest using budgeting tools like www.mint.com as a way to understand your current finances and where you might need to make changes.

6) Budget: While you may get some new tax breaks, one thing we can guarantee is that raising a child will cost money. The government recently released a report that estimates it costs $233,610 to raise a child born in 2015 to age 18 without taking into account tuition or inflation. Cost of living varies around the country and some regions may carry higher costs than others. Make sure you plan for these costs and increase your emergency fund to have at least 3-6 months’ worth of liquid living expenses.

7) Start saving for the future: 529 plan college savings accounts are one of the most popular ways to save for your child’s future. Money is gifted to the account where it grows tax-free for the purposes of education. These accounts can also be transferred to other family members. There is the option to ‘supercharge’ your 529 contribution by placing 5 years’ worth of gifts into the account. We often see grandparents looking to reduce the size of their estate utilize a supercharged 529 account for gifting. UTMA accounts are also great ways to save for a child, but keep in mind, these accounts will be considered assets of your child for college financial aid purposes. With the recent tax changes, an additional benefit is that 529 funds can be used for high school tuition. We’ve included some useful tools below to help you decide which savings account is right for you and your family.

Consider a Term Life Insurance Plan: Term life plans for younger parents can be relatively cost-effective ways to ensure that your child or partner have sufficient assets to sustain their quality of life should something happen to you. Many young families use these tools to bridge the gap from their asset accumulation years to when they have built up sufficient net worth later in life.

Considerations for grandparents: Beyond utilizing a supercharged 529 account for gifting, grandparents can utilize annual gifting to each beneficiary. For 2018, gifts of up to $15,000 can be given to each beneficiary without chipping away at lifetime gifting amounts or filing a gift tax return. In addition, gifts above the exclusion amount can also be made for tuition as long as they are made directly to the institution.

How WAM can help: We work with both parents and grandparents of young children who may be considering the planning strategies we outlined above. We welcome a time to have a dialogue about your family’s unique needs and how we can help to plan for a successful financial future.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

Congratulations! You’ve completed your undergraduate or graduate courses and are now moving on to the next phase in your life. Working and living on your own is exciting, with fresh opportunities and challenges, including taking responsibility for bills or loans and beginning the savings process for major purchases (car, home, or trips) and retirement. While this may seem overwhelming at first, having a Dialogue for Impact now to solidify your present financial standing will exponentially benefit you in the long run. We’ve developed a check-list for young professionals to reference when beginning their careers to Prioritize for Progress by strengthening their current situation, and simultaneously planning for their futures.

Savings & Expenses

The first question each graduate should ask is what cushion do I have in the case of a job loss, devastating injury, or unexpected life event. An emergency fund is critical to ensuring that, in a worst-case scenario, you aren’t stressed for cash. The balance of this account should typically reflect 3 months to 6 months of living expenses or the time it would take to find new employment.

An important piece of establishing a savings routine is understanding what current expenses total and what your overall financial picture looks like. A neat tool to use is Mint – a website that tracks all transactions for debit & credit cards and aggregates daily balances. Graphs and charts detail how much is spent in each category so users can determine if they are overbudget for restaurant spending or if they have the financial stability for upcoming vacations, philanthropy, or concert tickets. Checking Mint on a regular basis will also alert you to any discrepancies in your inventory of digital assets that may be related to fraudulent activity and increases the protection of your personal identifiable information (PII). An online password manager like Keeper is also useful for safeguarding online log-ins.

Once the emergency account has been appropriately funded with monthly income and expenses in mind, another great way to save is through the deferral of your paycheck into an employer-sponsored retirement plan, the most common being a 401(k). More details below:

401k

The 401(k) is a retirement plan that you contribute to with income from your paycheck on a pre-tax basis. Some employers offer matching contributions, usually up to 3% or 4% of what you defer. It would behoove employees to take advantage of this extra compensation that is essentially free money by contributing at least the matching rate.

A key component of 401ks and other retirement pans is the tax-deferred nature and inherent compounding interest. Compound interest is the idea that because capital gains and dividends are not taxed on an annual basis, they are able to be re-invested at a higher rate than if the gain or income was taxed. This is very beneficial for young investors with a long time-horizon to retirement. The chart below and the Khan Academy video explain compounding interest in greater detail. Another retirement account available to investors is the Roth IRA, explained more in the next section:

Chart: https://investor.vanguard.com/retirement/savings/when-to-start

Roth IRA

The Roth IRA is a tax-exempt retirement account, meaning that because the dollars you contributed have already been taxed, and will not be taxed again. Once you reach a certain age specified by the IRS, currently 59 ½, all funds in the account can be withdrawn without penalty. If an investor will be in a higher tax bracket later in life, then contributing to this account each year is very advantageous due to compounding interest and tax savings. The IRS specifies that qualified withdrawals for a first-time home purchase and certain medical/educational expenses and are not penalized if distributed from the account before 59 ½.

As of this writing the maximum contribution to the account is the lessor of earned income or $5,500. Investors should only make contributions to retirement accounts after accounting for all other bills as poor credit can negatively affect future purchases, which is addressed below:

Building Credit & Paying Off Debt

Anyone that has applied for a rental, car lease, or credit card knows that adequate credit is a critical piece of securing a satisfactory transaction. Poor credit can either cause the disqualification of a rental application, as most landlords will not rent to individuals with poor credit, or force home buyers to take on loans with excessively high interest rates. Effective steps to build credit are:

- Paying 100% of your bills on time, including utilities.

- Keeping lines of credit open, but with manageable balances (usually less than 30% of max credit)

- Always making the minimum payment on credit card bills on time to minimize interest charges.

- Monitoring your credit report for any irregularities.

- Organize student loans by interest rate and payoff the highest interest rates first. Refinancing student loans may also be an option

For those with minimal credit history, signing up for a credit card is a good start to build a credit profile. While access to credit may create budgeting risks, maintaining a consistent strategy for purchases and balance reduction is key to building your profile effectively. Your first credit card will most likely be with your current banking relationship, but subsequent cards may offer perks such as airline points, cash rewards, or retail partnerships.Nerd Wallet’s 2018 list of top credit cards is a great place to begin the search for a card outside of your normal bank to take advantage of category-specific cards like no annual fee, airline miles, and relationship rewards.

You can access your credit report free of charge annually at any of these sites:

Estate Planning

Young professionals may think that estate planning is reserved for high-net worth individuals or older generations, but every adult with meaningful assets should maintain some sort of documentation to describe how belongings will be distributed upon death.Trusted advisers can be leveraged to ensure the appropriate documents are drafted and then updated to reflect life changes. Declaring the recipients of your assets in a will or trust and electing beneficiaries for retirement accounts is a great start.

- A will is a broad document that directs the disbursement of your assets to friends, family, or charities at your death There are some brief requirements to validate the will at time of its writing: the individual must not be under duress, be of sound mind, and had two witnesses present.

- Naming beneficiaries to retirement accounts is another key estate planning tip to ensure assets are directed to the appropriate person or entity. Primary and contingent beneficiaries can often be named on accounts to provide some layering.

Young adulthood is not a cake-walk by any means, but by ensuring critical financial matters are addressed now, you allow yourself greater financial flexibility in future decisions. The Ripple Effect of establishing a solid financial base now will allow you to shift your attention to more enjoyable aspects later in life.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.