From airline tickets and car prices to gasoline and commodities, consumers and investors have experienced pockets of inflation as the U.S. economy continues to recover from the COVID-19 pandemic. We saw the May Consumer Price Index (CPI) numbers reflecting the largest month-over-month gain since 2008, and subsequently the Federal Reserve began talking about potential changes to monetary policy and their expectations for increasing inflation. As we turn to the Federal Reserve for guidance, let’s look at the role the Fed plays and the key points made during the most recent Federal Open Market Committee (FOMC) meeting, specifically a deep dive into inflation and what that means for investors.

The Federal Reserve:

The Federal Reserve (Fed) is the central banking system of the United States and is used to promote a strong economy. The Fed uses monetary policy to support their primary goals:

- Maximum Employment

- Price Stability

The Fed hopes to maintain consistent price stability as they set their long-term annual inflation rate target to 2%. A modest inflation rate is generally viewed as healthy for the economy as it can coincide with wage growth and maintain consumer demand; alternatively, deflating prices (deflation) or hyperinflation can stress the economy. While moderate increases in price is the ultimate inflation goal, the Fed’s most common levers to pull include:

- Open Market Operations –

- Buy/sell securities in the open market to help control liquidity.

- Setting the Discount Rate –

- Short-term interest rates the Fed uses to charge commercial banks. This has a spillover effect on all interest rates.

- Adjusting reserve requirements-

- Amount of cash banks need to hold

Recent FedSpeak and New Challenges:

As evidenced by the recent Fed meeting, uncertainty is still present despite Federal Reserve Chairman Jerome Powell communicating that the recent bounce in inflation is transitory – or not permanent. The Fed is experiencing new challenges with the recent record-breaking Government spending, higher tax proposals, and pent-up consumer demand due to the pandemic. Even with soaring unemployment last year, we saw the household savings rate increase during global shutdowns. We now find Americans excited to spend and make up for the lost opportunities last year – particularly in travel, dining and experiences. The higher demand and lost production time with factory shutdowns has also caused supply chain constraints in several industries such as autos, lumber, and chips/semiconductors leading to higher prices. This was captured in the latest inflation report, with Fed officials signaling higher expectations for inflation, as well as an earlier time frame for interest rate hikes. The FOMC hinted at two hikes in late 2023 on the recent dot plot projection versus the previous projection of no rate hikes in 2023, in fact, 7 members expected a rate rise in 2022. If higher inflation numbers continue to roll in, the Federal Reserve may be forced to lift rates earlier than they anticipated to achieve its mandate of maintaining price stability and moving towards full employment.

Inflation and How It’s Measured:

Simply put, inflation is the rise in price of goods over a period of time. Or viewed differently, a decrease in purchasing power of a currency for the same good. An example, is a loaf of bread costing 22 cents in 1960, today costs $2.12 or more. This price increase is inflation. However, we indulge in more than just bread, so economists look to inflation indexes for a broader representation. The Fed views price stability as moderate inflation

The Consumer Price Index (CPI) is the most recognized way of measuring inflation in the US and is reported monthly by the Bureau of Labor Statistics (BLS). The index is calculated by analyzing the price of a basket of goods and services. This basket includes eight categories: food/beverages, housing, clothing, transportation, medical care, recreation, education/communication and other goods and services. The aggregate change in price of the basket is known as the inflation rate and can be used for Cost-of-Living Adjustments (COLA) in Social Security or applicable pensions.

A Quick Look Back in History:

The BLS has a record of CPI dating all the way back to 1913. When going back this far, the average annual inflation rate is slightly over 3.10%*. This is in part due to greater volatility in prices. Within the last few decades, inflation has become much more stable as the Federal Reserve has had better oversight and control of monetary policy. Additionally, globalization, new technology and supply chain success has aided in keeping the price of goods low. In fact, inflation over the last decade is much lower than the historical average as it has been around 1.76%**.

Inflation Today and Where It’s Headed:

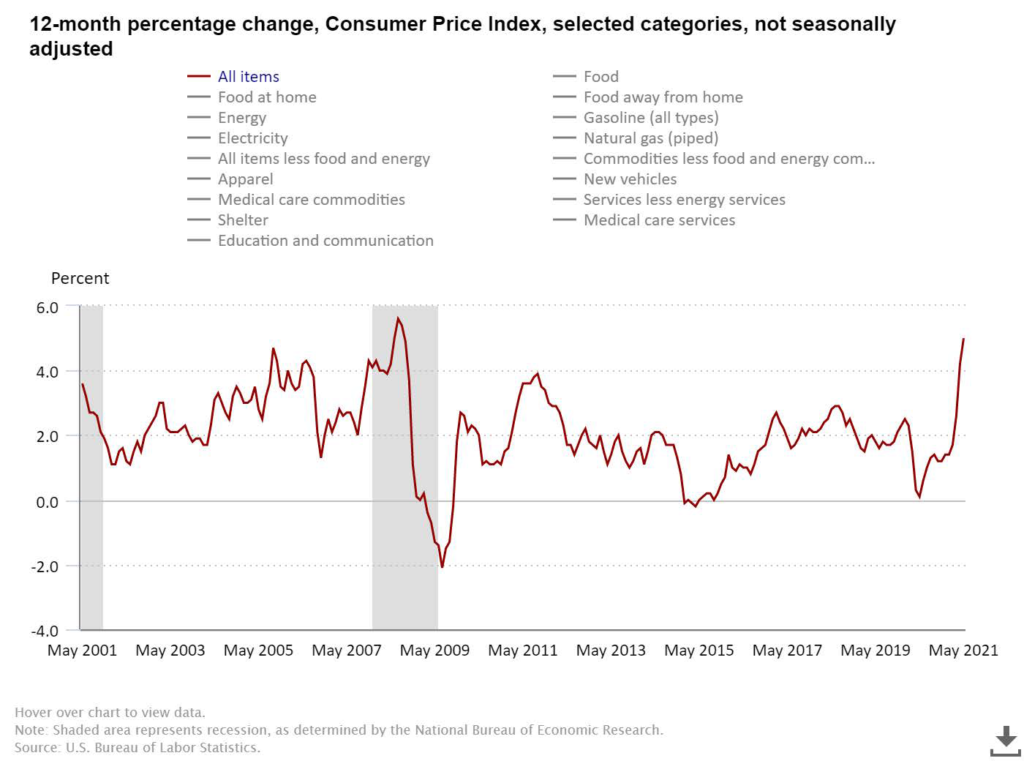

Inflation talks have taken over news headlines, Fed meetings and conversations with neighbors. And this should come as no surprise. When comparing to the prior year, the February inflation rate was up 1.7% and then April and May inflation rates rose to 4.2% and 5.0%, respectively. This dramatic jump can be attributed to the surge in demand for inputs and consumer goods as the U.S economy began to recover and grow at a larger than expected rate with gross domestic product (GDP) forecasts coming in at 7% versus 6.5% previously. Categories such as autos, airfares, and gas are seeing the biggest price increases as a temporary reopening demand surge.

Chart Sourced From: https://www.bls.gov/charts/consumer-price-index/consumer-price-index-by-category-line-chart.htm

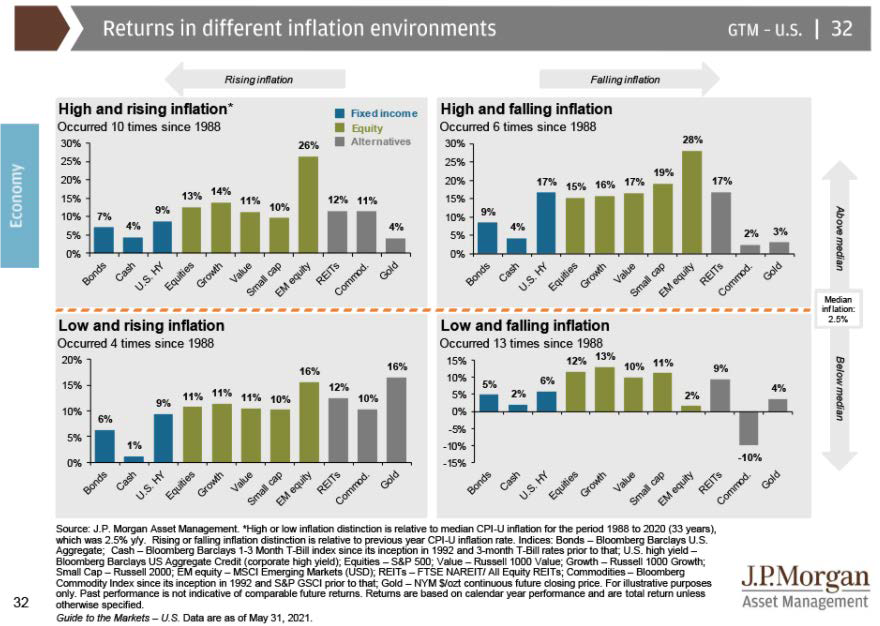

Impact on Portfolios:

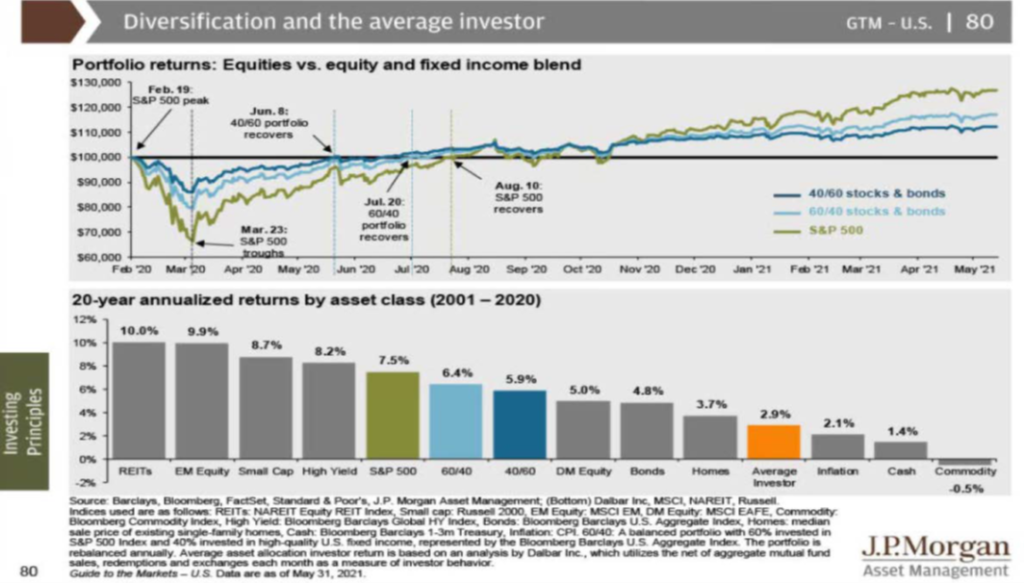

Whether inflation is here to stay or just a minor blip on the radar, it serves as a great time to review your asset allocation with your advisor. We believe a well-diversified portfolio tailored to your risk appetite is still appropriate to participate in market growth while limiting some downside risk. As discussed in our previous blog , it is also important to discuss concentrated positions with your advisor to evaluate risk in specific holdings or asset classes. Let’s take a look at how different asset classes may be affected by inflation:

Chart Sourced From: https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/

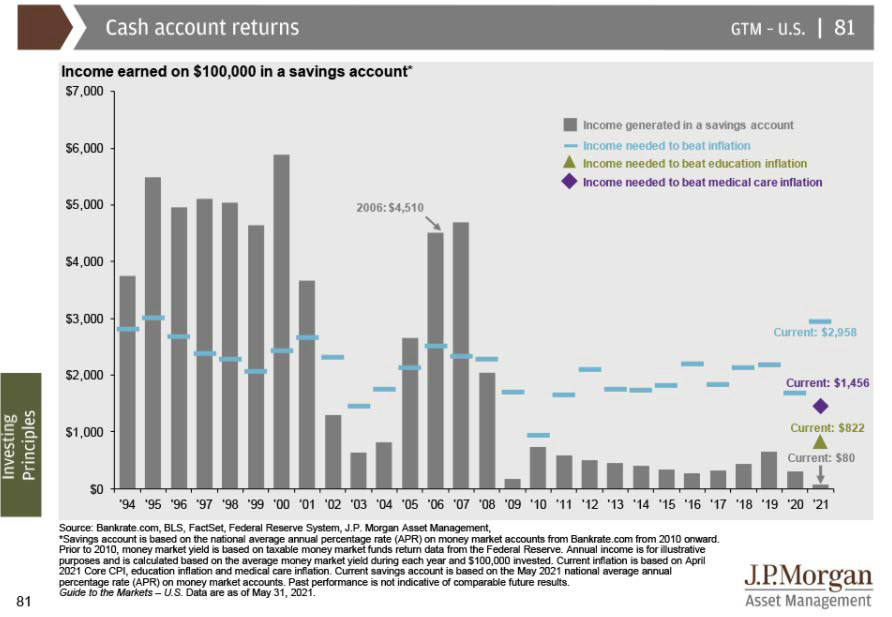

- Cash – is most vulnerable to inflation. While we still encourage holding an emergency fund and some cash for opportunities, the excessive cash held in a checking/saving account will lose purchasing power due to high inflation and little to no interest being earned. Cash enhanced short-term funds can be considered as a potential alternative as they yield higher returns while preserving liquidity.

Chart Sourced From: https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/

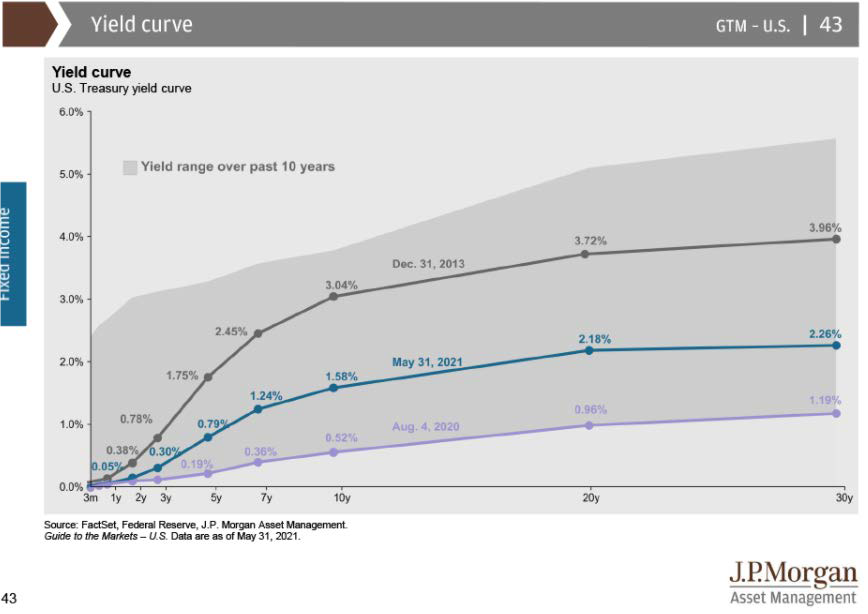

- Fixed Income – High Inflation can have a negative impact on real returns. Because of this the Fed will typically lift interest rates to combat higher inflation. When interest rates increase, bond prices typically fall. The idea is that bond investors may offload their current bond holdings on the secondary market and then purchase new bonds with a higher yield. Longer term and low-quality debt are most susceptible in this scenario. However, these interest rate changes do not impact the return of principal you receive at bond maturity. Treasury Inflation-Protected Securities (TIPS) provide protection against inflation by growing with CPI until maturity. Interest rates may be lower than other debt instruments given the attractive feature of increasing principal with inflation.

Chart Sourced From: https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/

- Equities – Stocks tend to be the best performing asset class with rising inflation. Since businesses are raising their prices, the benefits often flow through and benefit investors. Companies that require little capital, such as technology companies and communication services tend to do well in inflationary environments. Also, companies with a competitive advantage with high barriers of entry and strong consumer loyalty tend to well in this environment. However, high inflation and interest rate changes often increase volatility in the stock market. Equities undergo additional pressure as higher yields cause investors to reevaluate the risk/return relationship and may seek to invest in debt that pays some more in interest.

- Real Assets – Real estate and other tangible assets like commodities tend to do well in inflationary times. Historically, as inflation rises so does property values. This allows landlords to charge more for rent or homeowners to cash in more when they sell their property. Also, those who carry a fixed rate mortgage benefit from inflation since their monthly payment and outstanding debt does not grow.

Chart Sourced From: https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/

How WAM Can Help:

With inflation concerns and potential interest rate hikes on the horizon, we believe now is a great time to review your asset allocation with your advisors. Please reach out to our team and schedule a call to ensure your portfolio is positioned in accordance with your risk profile and the changing environment.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

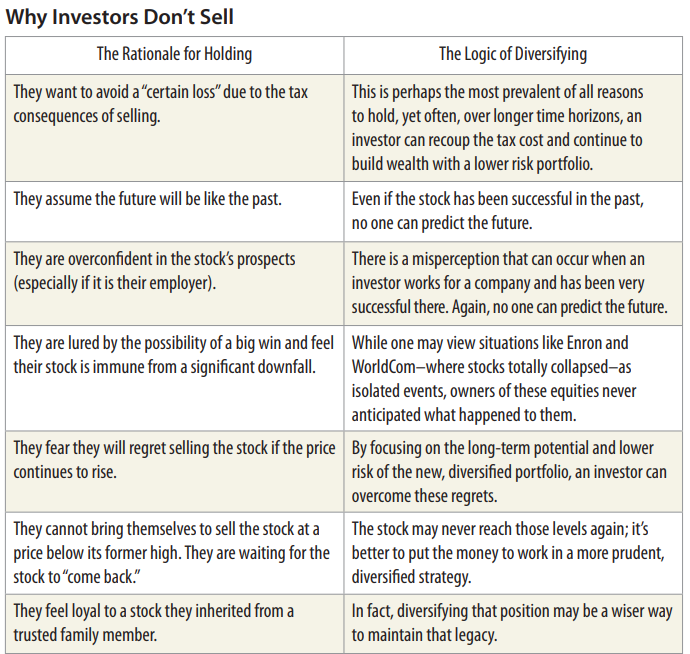

We all know the phrase “don’t put all your eggs in one basket” and there is one concept in the world of investing that universally applies to all individuals… diversification. Often, the very asset that has helped generate wealth over times poses the biggest risk to your financial future. We will be exploring highly concentrated positions and what this means to you as an investor.

Concentration occurs when an investor owns shares of a stock or other security type that represents a large portion of their overall portfolio or net worth. A position is typically considered to be concentrated when it represents 10% or more of the portfolio. Investors may understand the risk these positions represent but may choose not to take action for a variety for reasons including:

- Tax Ramifications – Often times, it’s as simple as not wanting to pay the capital gains tax associated with selling a portion of a highly appreciated security if held in taxable account. Alternatively, stock options awarded from employers can lead to significant tax liabilities due to supplemental income when exercised, highlighting the need for proper exercise strategies.

- Emotional Bias – Others may experience an emotional or behavioral connection to the company. This could stem from shares received from an employer and a sense of betrayal by selling these shares. Another emotional connection could arise from individuals who inherited concentrated positions from a loved one who felt strongly on the prospects of the company.

- Behavioral Bias – Lastly, investors may fall victim to a behavioral bias of a stock that has outperformed over time and believe past performance will continue into the future.

Chart Sourced From: https://content.rwbaird.com/RWB/Content/PDF/Insights/Whitepapers/Hidden-Cost-Holding-Concentrated-Position.pdf

Portfolios with large concentration in individual holdings can introduce risk that could otherwise be mitigated through proper diversification. Without proper planning, an investor’s overall portfolio performance can be driven by the heavily weighted security. There are copious factors that could put downward pressure on stock prices, such as a deterioration of company fundamentals, shift in public outlook or perception of the company/industry, regulation or change in key leadership to name a few. While not as common, black swan events can occur such as the well-known Enron scandal that evaporated wealth from shareholders and employees seemingly overnight. Additionally, changes in a company’s corporate structure may lead to unintended ramifications for shareholders. For example, Medtronic’s decision to change the location of their headquarters forced employees and shareholders to fully realize (pay tax on) their deferred capital gains without actually transacting the security. You can read more about it here.

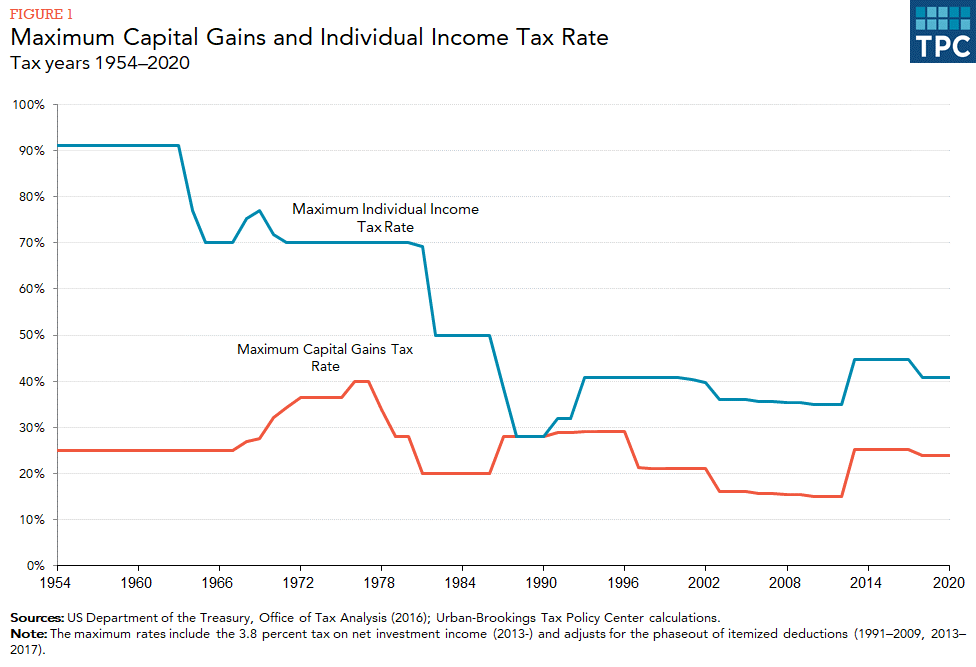

With a better understanding of some factors that lead to security concentration and associated risks, let’s circle back to the tax conversation. As of this posting, the Biden administration has proposed legislation to nearly double the top capital gain rate from the current 20% to 39.6%, excluding the additional 3.8% Medicare surtax. While this would only apply to those individuals with incomes of more than $1 million, current capital gains rates are historically low with most investors falling in the 0%-15% bracket. For context, top capital gain rates were roughly 40% in the late 1970s and have only decreased over the years. Whether the new legislation will be passed by Congress in its current form or if amendments to the rate and/or income limits is still unknown at this time. As a result of COVID-19, roughly $5.3 trillion of fiscal stimulus has been paid out to support the economy with trillions more on the table under the proposed American Families Plan and American Jobs Plan. This level of spending will need to be supported and as such we anticipate taxes to increase into the future. As the saying goes, “there’s no time like the present”, and certainly applies when looking to de-risk the portfolio and chip away at concentrated positions.

Graph Sourced From: https://www.taxpolicycenter.org/briefing-book/how-are-capital-gains-taxed

Aside from the capital gains we spoke to, another key aspect of tax legislation proposed by the Biden administration is the potential to limit the “step-up” in cost basis to the first $1 million of a deceased person’s assets and $2 million for married couples. This could lead to significant tax implications for the heirs looking to diversify concentrated positions as the original cost basis of the deceased will carry over to their beneficiaries.

How WAM Can Help

Through continuous collaboration with our clients, we help identify areas of concentration across your managed accounts in conjunction with your entire investment portfolio, including assets held away, as appropriate. With tax mitigation at the forefront, we can help create a plan of action to strategize the timing of de-risking the portfolio in low tax years or reducing concentration within tax deferred accounts, allowing the funds to be re-deployed into our new thematic ideas. We will continue to work alongside your trusted professionals to explore additional strategies such as tax loss harvesting and potential gifting scenarios for each client’s unique situation.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

Brooke Boone Kelly, CFP® also contributed as a co-author on this month’s blog.

The effects of the COVID-19 pandemic are far-reaching, as witnessed by major shifts in how we live, work, socialize and educate. The impact on the educational system in America is profound, as school districts juggle with how to both protect teachers and students from transmission of the virus, particularly as new strains are emerging, and how to protect the integrity of learning in a remote environment.

Getting kids back in school has been a priority of the Biden administration, with a goal of K-8 returning to in-person learning within 100 days if his Inauguration, right around mid-April. According to yesterday’s episode of The Daily Podcast (NY Times), about 1/3 of children are remote learning and 1/3 are hybrid, which may work for some students. However, remote learning tends to be subpar to in-person, and the disadvantaged suffer the most – particularly those effected by cost (hardware, software, wifi), learning disabilities or those that need help from adults who are also working remotely.

While challenging, COVID-19’s impact on education also brings a growing universe of technology, terminology, and metrics; balancing synchronous learning (real time, face to face, in person or video chat if available) vs. asynchronous (blogs, discussion boards, electronic text). While college-aged and postgraduate learners may have experienced asynchronous learning, most traditional experiences consist of a blend. Once a group of mainly in-person learners, now have a whole growing population of 5–12-year-olds evolving into sophisticated consumers of changing technology. The change in the traditional higher education business – which some argue was long overdue – highlights pricing pressures as universities move to a more digitally-driven model and students have more postsecondary educational options.

What this means for our clients:

Parents and grandparents alike want the best possible future for their families. The WAM team saw a boost in gifting in 2020, from family members that have been impacted by COVID-19 and to national and local charities. While there are shifts in the educational system underway, 529 college savings plans and custodial accounts can create a future benefit for young children.

As mentioned above, there has been over a decade of growth in “massively open online courses” (MOOCs), industry-driven certification programs, coding bootcamps, two-year associate degree programs, trade schools and vocational schools. While 529 plans are commonly used to cover costs associated with 4-year universities, there is a good chance many of the alternatives are also covered. As part of the TCJA of 2017, up to $10,000 can also be used annually on elementary, middle or high school tuition.

We’ve touched on the impact of “supercharging” or gifting 5 years upfront to 529 plans in a previous blog. Educational planning opportunities are just as important in a post-pandemic world and can provide an estate planning benefit if there is a change to the current estate tax exclusion amount.

What this means for our team:

We pride ourselves on a culture that values education, continued learning and problem solving. WAM has team members that regularly pursue master’s degrees, certifications, online training, and licensing to elevate their skill set and the client experience. During the last year, our team has shifted to remote learning when appropriate.

We continue to work with our clients in a hybrid remote capacity and strive to bring new investing and planning ideas to our dialogs. With the change in how we work with clients, we often utilize screen sharing capabilities, our secure portal and e-signature as we work together. We’ve taken the opportunity to not only educate ourselves, but often to walk through new tools and systems with our clients too.

What this means for the world:

Over the past two decades, access to 3 meals a day, internet service, and technology hardware have been growing challenges faced by a large percentage of the learning population. Public K-12 schools traditionally have had to combine fundraising, and donations with grant money to outfit the technology learning curriculum, and have comprehensive meal assistance programs. Private institutions may have historically had larger budgets and greater resources, but diverse income levels amongst the student body still posed challenges. The present concerns are mounting, and many nations are gauging the impact on future economies too.

According to a study published by the Organization for Economic Co-operation and Development (OECD), “existing research suggests that students in grades 1-12 affected by the closures might expect some 3% lower income over their entire lifetimes. For nations, the lower long-term growth related to such losses might yield an average of 1.5% lower annual GDP for the remainder of the century.” The effects of lost in-person learning aren’t only economic, the school closures expect to also disrupt emotional, social and motivational development especially in younger children. The impact will fall mainly to disadvantaged students and vulnerable populations. The K-shaped recovery in America will only deepen as the gaps in the educational system widen.

The pandemic has accelerated many trends already in place and disrupted many industries. How people are able to choose to pursue education in the future for work related training, higher and lower education and all age groups, young and old, will influence how we emerge.

How WAM can help:

Our advisors are here to discuss opportunities in the educational space including college funding and estate planning, how we can learn together remotely, or charitable giving. Please contact the team to discuss your unique situation and how we might be of assistance.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

The novel Coronavirus has dramatically disrupted lives on a global scale. As businesses and individuals attempt to adapt to a post-COVID world, a series of new trends and opportunities have emerged. We have observed a shift away from major US cities to more affordable communities outside of traditional metropolitan areas. Clients transitioning to new living spaces have capitalized on the low interest rate environment and explored multi-generational gifting strategies or intra-family loans with our team. As we all continue to battle the pandemic, we welcome you to lean on your trusted Weatherly advisors to safeguard your financial assets and uncover potential planning opportunities.

White Picket Fence Comeback –

A trend the Weatherly team is following closely has been the exodus of some Millennial and Generation X populations from cities to suburbs. As real estate prices and rents have skyrocketed in major metropolitan areas, like New York and San Francisco, young adults have looked for relief in less expensive pastures as they start families and settle in their careers. Outside of monetary factors, recent concerns over COVID-19 infection and social turmoil have also augmented the migration to suburbia. Homeownership in the United States rose to 67.9% in the second quarter, its highest level since the housing peak in 2008. Conversely, the number of renter households fell by 7.2%. Owners under age 35 have been the leaders in driving this trend as the group’s home ownership rate is now at 40.6% [1]. Skilled workers that previously may have been required to work on-site, may now have the flexibility to stay with their current employers, but resettle to a different location and work remotely. We may see a lasting impact on commercial properties as businesses move away from shared workspaces and offices as a heightened focused is placed on social distancing and telework.

Zero-Interest Rate Policy (ZIRP) –

When the markets took a downturn in late February and early March 2020, the Federal Reserve acted quickly and provided a safety net for the domestic economy by lowering the Fed Funds rate to near 0%. This paramount move was in hopes to add liquidity by allowing businesses and consumers to borrow money at favorable rates and spur investment activity. The Fed Funds rate has had a spillover effect on the broader fixed income market as interest rates across the board came down in tandem. Included in this, is the 10-year treasury yield which is largely tied to mortgage interest rates. This has sparked a fury of homeowners looking to refinance their mortgage at lower interest rates. You can check today’s current interest rate estimates via sites like bankrate.com . With unemployment skyrocketing, refinancing has been a silver lining for Americans to maintain cashflow needs or provide the ability to invest extra funds into a deflated stock market. The historical low rates have also created an opportunity for the first-time homebuyer looking to enter the residential real estate market.

Gifting Outside the Box –

The simultaneous decline in real asset values and volatility in financial markets have created a gifting opportunity for high-net worth clients interested in advanced estate planning. Depressed assets, that may appreciate significantly following the COVID-19 pandemic, could possibly be transferred earlier than anticipated through a direct cash gift, sale by installments, or transfers in an intra-family loan. In these scenarios, assets can be passed or purchased at a depreciated market values with interest payments at modest levels due to historically low interest rates. Below we’ve outlined some strategies we’ve reviewed with clients assisting the next generation with first-time home purchases.

- Direct Cash Gift – We’ve recently worked with clients to assist their heirs through a one-time gift or periodic gifting schedule. Parents can also offer to co-own or purchase a home outright with a child as the parent, with a longer credit history and greater asset base, can often qualify for a lower interest rate than the child could on his or her own. Although this is the simplest method of transferring wealth, it’s important to be mindful of the annual gift tax exclusion, $15,000 per person as of 2020, given that any gifts above this amount can result in a decrease in your lifetime exemption and a gift tax return filing.

- Installment Sale – An Installment Sale is a transfer of property where at least one payment is made in a tax year different from when the sale is agreed upon. Breaking up the sale allows for the seller to piecemeal the capital gain realized from selling the asset, which may have appreciated significantly from purchase date or feature cost basis reduction from depreciation. The buyer also doesn’t have to come up with the full payment amount right away and can chip away at the purchase price over time.

- Intra-Family Loan – A loan, with the proper documentation, can be a great way to provide liquidity to younger family members with a purchase of an asset that would normally be out of their price range. Starting with a promissory note that outlines the loan amount, term, and an appropriate interest rate is the best practice to ensure that an audit down the line won’t result in any tax consequences. Here’s a link to an Index of Applicable Federal Rates (AFR) to use as a baseline for the stated interest rate.

How Can WAM Help?

We invite you to leverage us, as your trusted advisors, to run financial planning scenarios to determine housing affordability, suggestions to estate plans and connections to mortgage professionals. We can help streamline the mortgage process by providing necessary documentation to lenders in a secure format. For those new to the residential real estate market, we suggest reviewing our First-Time Home Buyer’s Checklist which provides a step-by-step guide to home ownership. Please contact us with any questions or to continue the conversation.

Sources and Further Reading –

https://www.thebalance.com/treasury-note-and-mortgage-rate-relationship-3305734

https://www.nerdwallet.com/article/mortgages/closing-costs-mortgage-fees-explained

https://www.chase.com/personal/mortgage/home-mortgage/getting-started/mortgage-prequalification

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

There’s a common thought in investing – put your money to work in companies that produce the products you use or in management that you believe in. Well, why not align your investments with your principles? Recently, we’ve seen massive inflows to a theme known as Socially Responsible Investing (SRI). There are two ways to utilize SRI principles – either by screening for or avoiding certain industries (ex: tobacco, firearms, oil, chemicals) or by selecting companies through specific criteria known as “ESG” factors, which broken down are:

Environmental Effect – How does a company impact the environment through direct or indirect externalities and how will the company fare as the effects of climate change take hold? Often clean-energy industries get an A grade in this factor, while polluting sectors often score poorly.

Social Stances – How does the organization treat the impact of its operations on all stakeholders? This includes gender equality, benefits to workers, and charitable activity in the community. We’ve seen numerous companies like Target, Wal-Mart, and Amazon raise wages for workers above the federal or state minimums.

Good Governance – How does the company operate through its board and management decisions? Independent directors and auditors that monitor managers are key to the longevity of the organization, just ask shareholders in Enron and Lehman Brothers.

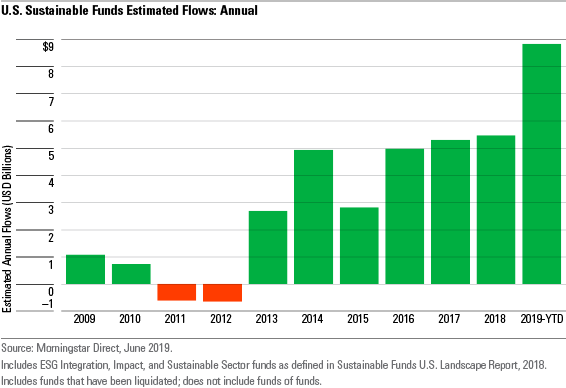

Demand for funds that satisfy ESG metrics is rising, mostly in part to a growing millennial investor base, many of whom demand social responsibility when making investments. The chart below from MorningStar highlights the estimated $8.9b in net inflows into sustainable funds held in the United States in the first six months of 2019.

Socially responsible investing in International markets is not far behind as sovereign wealth funds must look to make “financial flows consistent” with lower-carbon emissions and sustainability in accordance with the 2015 Paris Climate Agreement. Expectations for more growth in the ESG space can be attributed to new offerings for this option in employer-sponsored 401k plans, as only 5% of 401(k)s offered a dedicated ESG fund for employees in 2018.

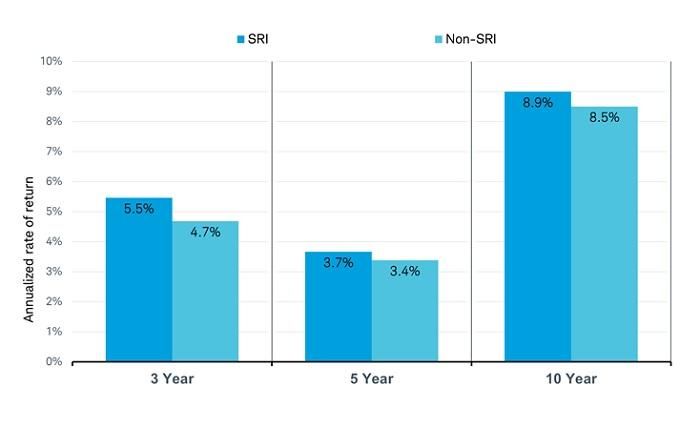

Although performance considerations may have kept some investors from utilizing socially responsible investing funds in the past, they’ve outperformed their non-SRI peers over a few different timelines as shown in the chart below.

When looking at the broader market, Vanguard’s Social Index has returned 4.3% vs. the S&P 500 return of 5.5% since the social index’s inception in 2000.

SRI funds may also have expense ratios (fees) that are higher than their counterparts given the specific criteria that a fund manager must follow. Interestingly, 53% of the available mutual funds that Morningstar highlights as socially responsible had lower expense ratios than the non-SRI funds in the same category.

Weatherly works closely with clients to attain their investing goals through the screening of unwanted holdings and creation of customized portfolios. Our team has restricted industries or companies at the requests of clients through our portfolio management system to notify our investment team of any specific sectors to avoid for each client or account. Alternatively, advisors will note when a client wishes to only invest in companies that promote ESG traits and ethics. When investments are made, a detailed background review is completed for each equity or fixed income position to ensure that the investment is made within SRI guidelines and principles as outlined per client.

We’d suggest speaking to an advisor to see if utilizing ESG metrics in your investments is appropriate. Additionally, Fidelity and Schwab both offer exchange-traded fund screeners to narrow the scope of available funds to fit ESG characteristics.

In addition to socially responsible investing, Weatherly prides itself on implementing sustainable practices throughout all areas of our business. Whether it be hosting a local beach clean-up , providing re-usable cutlery and dishes for employee lunches, or implementing electronic signature software to cut down on paper, Weatherly is passionate and dedicated towards doing what we can to create a leaner, greener future – and we want to help you do the same!

When exploring options of moving towards a sustainable lifestyle, it can sometimes be overwhelming. With so many options in just about every aspect of life, it is often hard to know where to begin. Below are some small and easy changes that can have big impact on reducing our environmental footprint.

On the go:

– Eliminate plastic bottles – Carry a re-fillable water bottle for any hydration needs. We proudly welcome all new clients with a reusable Weatherly water bottle. Please don’t hesitate to contact us if you would like one, as we would be happy to send!

– Avoid plastic bags – Keep cloth/canvas tote bags in the trunk of your car so you never forget them when going to the store to buy groceries or other goods.

– Consolidate errands – Plan/map out errand runs to save money on gas and reduce carbon emissions. Or even better, walk, bike, and/or carpool if possible.

At home:

– Know the rules of recycling in your area – Check out “What Goes Where” for San Diego county residents.

– Stop junk mail – Unsubscribe from those pesky marketers and save paper while doing it. View the New York Times article with helpful tips here.

– Compost – It is estimated that food scraps and yard waste together currently make up to 30% of what we throw away and should be composted instead. DIY compost bins can be made for as little as $10, and many communities host free workshops to help get you started.

At work:

– Eliminate take out containers – Bring your lunch from home in a re-usable lunch box. Even better, bring your own re-usable cutlery and napkin too!

– Reduce paper – Make conscious choices around the office to use less paper. Re-purpose no longer needed one-sided sheets into scratch paper before recycling or shredding.

– Unplug Electronics – Even while turned off, electronics still use energy as long as they are plugged in. Save energy by unplugging applicable electronics before leaving the office for the evening.

It is important to remember patience when transitioning towards greater sustainability. Even the smallest changes, whether in an investment portfolio or in a daily routine, can go a long way to make our world a better place.

We continue to educate ourselves on how to better our community and plan for a future in a world limited by finite resources and talent. Our team persistently researches and uncovers new trends to capture cultural and social movements in thematic investments for clients. Please free to reach out to Weatherly with any questions or suggestions to assist with your journey towards a sustainable future, we are all in this together.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

The Bull Market Turns Nine, What’s Next?

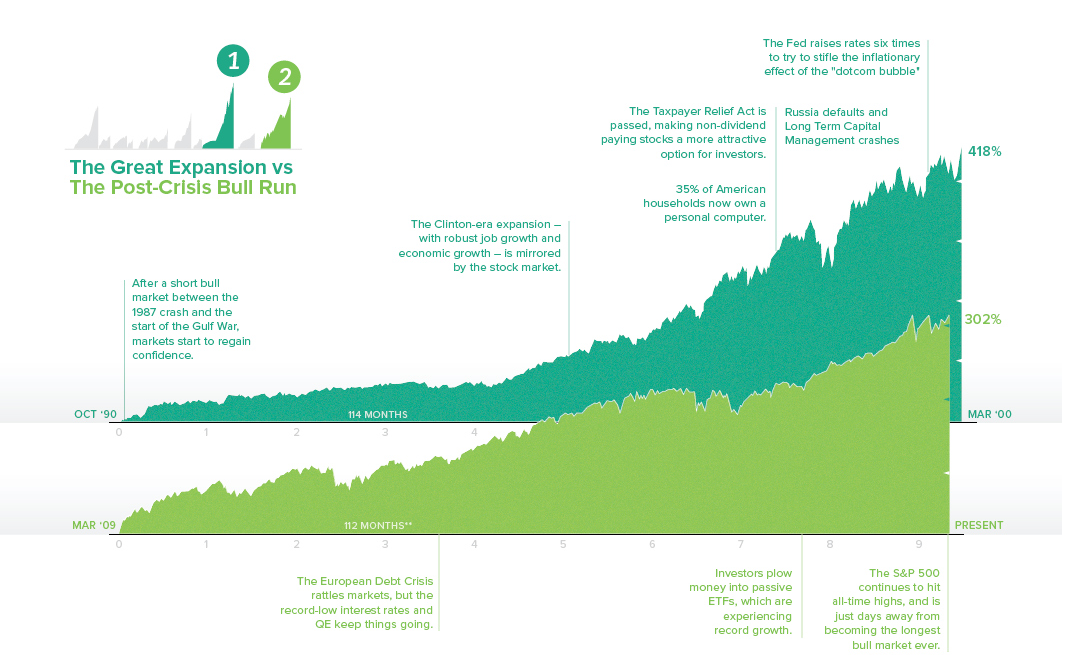

The media and investment community have recently focused attention on the length of the current U.S. bull market with great speculation on sustainability of positive returns. The Post Crisis Bull Run is now the longest bull market in history as of August 22, 2018. However, in our view market outlook should not be based solely on length but rather formed through a well-researched understanding of fundamental macroeconomic indicators, US consumer health, corporate valuations, and the geopolitical landscape.

Context

The Great Expansion, now the second longest bull market, lasted approximately 114 months, from October 1990 to March 2000. During the 114 months period, the S&P returned 418%.

The Post Crisis Bull Run, from March 2009 to present, returned 302% on the S&P 500. In both 2011 and 2015 the market corrected due to concerns regarding the European debt crisis and global debt levels. In both cases, the market rallied and continued its upward trend.

*All figures are as of June 30, 20181

What is best? A long term view

Portfolio management and appropriate overall strategy is an ongoing and iterative process. We strive to collaborate with our clients to ensure changes to your individual situation are incorporated with our outlook to best address opportunities and risks. A steady hand and focus on the long term are key to our client’s success. JP Morgan completed a study that illustrates the importance of a consistent investment approach through volatility and the precarious challenge timing the markets. For further information, reference this link.

Weatherly takes a long term fundamental view to best position client portfolios in all market environments. Many market participants don’t know that strategic asset allocation is the primary driver of portfolio returns. A Financial Analysts Journal study found that active asset allocation accounts for approximately 93% of investment performance2. Our team analyzes markets with a top down and bottom up approach within a macroeconomic framework. We deploy tactical asset allocation decisions to make incremental changes that are consistent with each client’s unique goals, risk/return profile, and our economic outlook.

Where We’ve Been and Where We Are Now

In 2018, we have seen a disparity in investment performance across sectors. The technology sector has led the way returning approximately 21% year to date vs the S&P 500 returning 10.4% YTD. There has specifically been a tilt towards Facebook, Apple, Amazon, Netflix, and Google, commonly referred to as FAANG in 2018.

It is also important to highlight a few economic indicators to fully understand the current business cycle and 2018 market.

- U.S. Employment Rate: In May of 2018, we saw the unemployment rate reach an 18 year low of 3.8% (and 3.9% in July 2018), which suggests that we are at full employment levels. Wage growth, however, has remained low at a 2.7% rate year over year.

- Inflation Target: the early stages of inflation rising is a bullish or positive indicator for the economy as demand for products has grown and prices are increasing. The Federal Open Market Committee’s (FOMC) target inflation rate is 2% and the current annualized U.S. inflation rate is 2.9% as of July 2018.

- Interest Rates: Given the uptick in inflation, we’ve seen the Federal Reserve methodically raise short-term rates with plans to continue at the next FOMC meetings in a response to rising inflation.

- Gross Domestic Product (GDP): known as the output of a country’s economy. We have continued to see steady GDP growth with an annualized growth rate of 4.1% as of June 30, 2018. Approximately 70% of the GDP growth is due to consumer discretionary spending, which suggests that consumers are spending money, a positive economic indicator.

- Corporate Earnings: In Q1 2018, we saw corporate profits increase by 8.7% (or $153 billion) to an all-time high mainly due to the decrease in corporate tax rates to 21% from 35% under the Tax Cut and Jobs Act. The increase in corporate earnings has enabled corporations to invest funds in stock buyback programs and implementation of or increasing their dividend payouts.3

These indicators suggest that the economy is healthy, consumer spending remains steady, and we are in the late expansionary period of the business cycle. Weatherly has implemented specific strategies to position client portfolios for the current market environment, but recognize how far certain asset classes have appreciated, and are working to position clients for additional volatility in the coming years.

Strategies Implemented in 2018

- Tactical Asset Allocation and Options Strategy- Based on each client’s unique goals and risk/ return profile, Weatherly has begun to proactively shift client portfolios to asset allocation neutral in response to the rise in equities as we potentially near the end of the bull market. Our tactical asset allocation approach is two- fold. First, we have shaved down stocks that have appreciated significantly. Second, we have rotated out of specific sectors that may be negatively impacted by the current economic environment. For clients with concentrated positions, we have also utilized our covered call options strategy to reduce single stock exposure and opportunistically increase income in portfolios. Reference our covered call write-up here for further details.

- Fixed Income Strategy- The current flattening of the yield curve makes short term debt instruments attractive as investors can capture a reasonable rate of return, while reducing exposure to interest rate risk, credit risk, and inflation rate risk. Given these factors, we have proactively put funds to work in short to intermediate-term corporate and municipal bonds with maturities of 1-7 years.

- Collaborate with Your Designated Professional Advisors- We also work directly with clients’ designated professional advisors- CPAs, attorneys, other financial advisors – on tax loss harvesting strategies and giving strategies via Donor Advised Funds (DAFs) and/or Qualified Charitable Distributions (QCDs) via client’s IRA Minimum Required Distribution (MRD). These strategies can also reduce equity exposure in portfolios.

- Tax Loss Harvesting- At the end of the third and fourth quarters, we work directly with clients and their CPAs on tax loss harvesting for clients that may have a large tax bill following a high-income tax year or realizing large capital gain. This strategy involves selling securities at a loss, which allows the client to reduce capital gains tax and offset up to $3,000 of ordinary income.

- Giving Strategies- With large unrealized capital gains in client accounts, Weatherly has incorporated Donor Advised Funds (DAFS) and Qualified Charitable Distributions (QCDs) to strategically shave down these positions in client accounts. Given the unique tax implications of contributing via a DAF vs a QCD, Weatherly consults your CPAs and team of professionals to determine the appropriate giving strategies and vehicles for 2018. Please reference of Charitable Giving blog post and this link for further information on DAFs and QCDs.

Weatherly has proactively put these strategies into action based on each client’s risk-return profile and unique financial goals. Please feel free to contact us to discuss our strategy, market outlook, and your specific situation in more detail.

References

- https://www.businessinsider.com/heres-what-the-longest-bull-runs-of-the-modern-era-have-looked-like-2018-6

- http://www.grbestpractices.org/sites/grbestpractices.org/files/Determinants%20of%20Portfolio%20Performance%20II%20An%20Update.pdf

- https://tradingeconomics.com/united-states/corporate-profits

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

Ordering supper, listening to music, arranging transportation, banking and socializing can now all be handled electronically, efficiently, and oftentimes without any human interaction. While this frees up time to be with those we love, explore new places, and dedicate to our communities, increases in data sharing and accessibility present both risks and opportunities for consideration.

A recent Wall Street Journal* article highlights just how much information we share with high-tech companies when doing something as simple as planning pizza delivery and at home movie night with a friend. Ordering online, paying through the Alexa app, and using Google Maps for directions to the friend’s house resulted in two women sharing over 50 pieces of data with tech companies including Apple, Amazon, Google, and Facebook.

Ongoing news about Facebook and Cambridge Analytics illustrates some of the risks associated with data collection. The EU’sGeneral Data Protection Regulation (GDPR) will go into effect May 25, 2018; this law on data protection and privacy for all individuals within the European Union will be enforced internationally, as it addresses the export of personal data outside the EU. Businesses are being held accountable for adhering to their privacy policies. At Weatherly, we have a strict privacy policy and comprehensive data security program addressing our perpetual commitment to securing our network infrastructure and client privacy.

How many devices do you and your family use on a daily basis? There are currently 20.8 billion devices compromising the Internet of Things (IoT) and Cisco predicts by 2020 this will increase to 50 billion. Two of the most valuable components within the digital domain are privacy and quality of service. Technology used well can help streamline our lives, but take care to guard your personal information with best practices.

Given the remarkable amount of data that is being generated by our digital footprint, Weatherly looks to capture that trend by investing in companies leveraging the information we knowingly, or unknowingly make public. Have you ever searched for a product on Google or Amazon and decided not to buy it? The next day, have you logged into your web browser and viewed an advertisement for the exact product, but now for a slight discount? Your search queries, purchase habits, and geolocation are all being analyzed to provide you with relevant advertisements. Companies like Amazon, Google and Facebook have been generating millions in revenue allowing advertisers to leverage the data they have on your behavior. These providers also remind you of recurring purchases (dog food, diapers) or search pattern.

Intelligent interaction with machines, the web and the cloud is another space that is evolving, often called Web 4.0. With cameras for facial recognition and digital breadcrumbs to accurately predict your behavior, our interactions with technology will become more and more intuitive, helpful and in some ways creepy. Imagine you wake up and your bed tells you, “Coffee is ready in 3 minutes, traffic is already looking bad, so leave 7 minutes earlier than you normally do to make it to work on time. You have enough milk for one bowl of cereal, so I’ve ordered milk to be delivered by this evening. Don’t forget to exercise, you told me last week to remind you even if you tell me not to because you’ve gained 4 pounds since last month.” These types of interactions will only become more commonplace as you get ready for your day and before you get into your self-driving car and listen to music recommended to you by Spotify based on your previous listening.

Another way to capture this data splurge from an investment standpoint is by protecting it. Cyber security from hacking is paramount to our data being contained. Companies providing solutions for consumers, corporations or government are ripe for growth as bad actors around the world work to undermine security practices. Beware of fraud via phone, phishing, and email links.

Finally, blockchain technology is being adapted to a variety of industries to improve efficiency and increase transparency. Most simply, blockchain removes the human middle-man and allows processes to occur faster with fewer errors. The goal is also to eliminate the opportunity for fraud. Some applications are found here:

At Weatherly, our modus operandi is to guide our clients’ financial lives to meet goals, and a large part of achieving those goals is through the investment process. By identifying and capturing trends, we hope to generate value for our clients by investing in the companies best adapting to the new world.

*The article referenced requires a paid subscription to WSJ. Please contact us for further details.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

The exchange of services and goods has existed in economies since the creation of civilization, although the method of payment has transitioned over time from a barter system to mediums of exchanges such as coins and banknotes. More recently, electronic exchanges have revolutionized the way consumers, producers, and service providers transact. Credit cards and other loaning mechanisms have given individuals and small organizations the ability to take on more credit, allowing for jumps in consumer spending and economic activity. New types of exchanges and currencies have rapidly innovated and transformed established financial industries and practices, although they each feature their own concerns over privacy, security, and valuations that users should consider.

Institution Disruptors

- Payments – PayPal (PYPL) has revolutionized the e-payment space with its online transaction platform by offering secure transactions between individuals and businesses, notably for international payments and currency conversions. Its consumer application Venmo, has fit in perfectly in today’s sharing economy by fusing social media with peer-to-peer transactions so friends can share their payment history. PayPal also recently confirmed that major retailers will begin accepting Venmo.

- Lending – LendingClub (LC), SoFi, and UpStart are online lending applications that allow individuals to access private markets for mortgages, student loans, and personal loans that would historically only have been available through large creditors. Traditional creditors without efficient digital platforms are facing an existential threat from new lenders that ease the financial process for customers comfortable with online applications.

- Raising Capital – GoFundMe and KickStarter give individuals the ability to raise large amounts from many small donations for social entrepreneurship, business ventures, or charitable causes. These crowdfunding platforms appear ripe to delve into the space previously ruled by venture capitalist and private equity firms and allow smaller investors to make impactful contributions.

“Moneyless Money”

What is it? – Digital currencies, such as Bitcoin and Ethereum, utilize block-chain technologies to track and validate each piece that is owned, spent, or sold in decentralized exchanges.

- Blockchain – digital ledger of transactions

- Decentralized exchange – transactions occur on a peer-to-peer basis and do not flow through a central location where the value of the money is defined and controlled

What are the effects on markets? – Digital currencies have exploded in value as investor exuberance has reached all-time highs. The popularity of the currency could lead to the diminished use of standard money (i.e. banknotes and coins) and therefore present difficulties for central banks to influence financial markets through the use of monetary policy. Opinions of the currency concerning valuations differ across many industry leaders, even Jamie Dimon of JPMorgan weighed in by recently referring to Bitcoin as a fraud..

What is the legal status? – Bitcoin has been legal in the United States since 2013 and is classified as a commodity by the CFTC. Critics however have noted that Bitcoin is solely used for the purchase of illegal goods or criminal activities. Supporters will respond that because the address of each transaction is tracked, authorities will be able monitor these transactions and thwart the perpetrators more efficiently.

Can’t get enough? Follow a few links below for further reading!

- Cryptocurrency 101

- The Truth About Blockchain

- Blockchain: A Better Way to Track Pork Chops, Bonds, Bad Peanut Butter?

Digital Marketplace Concerns

The opportunities and benefits of technical innovations in payment systems, lending platforms, and raising capital come accompanied by certain risks related to data privacy and human error. Protecting personal information will need to remain paramount during the evolving use and implementation of such tools. Consumers and businesses will need to prioritize their focus on data security, cyber hygiene, and education.

While the overall market for digital currencies estimated worth has been valued at $160 billion (CoinMarketCap), these currencies present a unique set of concerns and risk. The SEC has succinct bulletins outlining risks related to bitcoin and initial coin offerings. Some risks investors interested in the space may want to consider are: being targets for fraudulent or high-risk investment schemes, lack of insurance and recovery options, exchange rate volatility, and a volatile regulatory environment, like recent news in China and Japan (Ripple).

As new financial practices and mediums of exchange flood our economies and marketplaces, investors can be sure of one thing – innovations in financial technologies will continue to revolutionize institutions and processes critical to our daily lives. Weatherly’s team has taken note of these rapid changes and will continue to strenuously monitor new industries mentioned in this article, specifically mobile payment systems through blockchain technologies, to capitalize on new opportunities at the company level.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

As growth and inflation expectations have risen over the past several months, stocks and bonds have had very different reactions. Let’s look at some principles of bond investing to shed some light!

Bond Mechanics

Bonds can be offered by many different types of agencies, including federal governments, municipalities, and corporations. These securities have five inherent components:

- Maturity – how much time is left until the bond expires and the principal is returned to the lender. The longer the maturity of a bond, the more sensitive the bond market price is to changes in prevailing interest rates.

- Duration – the maturity of an investment based on weighted cash flows. If the majority of a bond’s cash flows are attributable to the final principal payment, then the duration will be closer to the bond’s maturity.

- Coupon/interest rate – the stated amount that the lender will be compensated on a regular basis for providing the loan to the borrower. The amount is typically paid on an semi-annual basis and is based on a percentage of the par value of the bond. For example, a bond with a coupon rate of 5%, paid on a semiannual basis, and $1,000 par value will receive coupon payments twice a year of $25.

- Yield – the annual return, in percentage terms, the investor will expect to receive by investing in the bond if held to maturity. Yield is inversely related to price; the higher the yield, the lower the price, and vice-versa. Yields can be stated as return within a certain time period such as yield to maturity or yield to call. If a bond’s price is greater than its par value, the bond is stated to be priced at premium and the yield to maturity will be lower than that of the par priced bond. The opposite of a premium is a discount, and occurs when the market price is lower than par price.

- Credit rating – is an assessment of the likelihood that the borrower will repay the borrowed principal and meet scheduled interest payments. The lower the credit rating, the less likely that the borrower will meet these payments. There are two tiers to credit ratings, investment grade and speculative (junk) grade.Weatherly limits its fixed income investing to bonds with investment grade ratings.

Fixed income valuations are derived from the characteristics listed above, but are responsive to universal market risks. Investors are compensated for taking on additional risk through a higher coupon payment or higher yields/lower prices. The following risks are common in bond investing:

- Interest Rate Risk – As interest rates rise, newer issues of bonds will have higher yields that compensate lenders at a higher amount. Now that these “new” bonds with a higher compensation rate and lower priced bonds are available in the market, bond buyers will have less of an appetite for the previously issued bonds with a similar risk profile, but lower interest/coupon rate. Therefore, these “old” bonds will experience a decline in market value and rise in yield until there is an equilibrium in the marketplace.

- Credit/Default Risk – The greater the likelihood that an interest payment or repayment will not be met by the borrower. As with most other risks, the investor will be compensated with a higher coupon rate or higher yield for taking on the higher risk.

- Maturity Risk – In a vacuum, a bond with longer maturity has a greater risk than a bond with a shorter maturity purely because the lender is required to wait a longer period of time to receive the principal repayment amount. This is featured on the upward sloping yield curve, as investors are compensated with a higher yield on their investments, the longer the maturity of the bond.

- Inflation Risk – Traditional bonds will repay principal at the maturity date and pay the stated coupon at the regularly scheduled date. The inherent risk to lenders is that these payments are not indexed for inflation and will therefore not rise in value with the inflation of a given currency, negating the real return of the investment.

If rates do rise, how will that affect fixed income investing for Weatherly clients?

Investments with longer maturities such as 30 year or even 50 year investments experience a more dramatic drop in price compared to similar shorter maturity investments as rates rise. Speculative grade investments with lower credit quality also respond with a larger depreciation in market value in a rising rate environment in juxtaposition to investment grade bonds. Weatherly strategically invests in high-quality (investment grade) and short to medium term (generally <7 years to maturity) investments with values that are marginally less affected by interest rate changes risk to avoid a steep drop in portfolio returns. Duration is generally much lower than average maturity in Weatherly portfolios.

How will the new administration’s policies affect bond values and availability?

The new administration has advocated for widespread tax reform, most notably the decrease of marginal tax rates for individuals and increased infrastructure spending. Municipal bond income is untaxed for individual bondholders and boost after tax yields for high-net worth individuals. Marginal tax rates would be required to drop significantly to equalize the current after-tax yields of municipal bonds with comparable U.S Treasuries and corporate bonds. The current administration has also proposed infrastructure spending in many districts that would boost municipal bond issuances and a potential offering of a Build America Bond replica. Build America Bonds, created under the America Recovery and Reinvestment Act in 2007, are taxable municipal bonds that carry federal subsidies for the bond issuer, who can then pass on the subsidy to bond buyers. Build America Bonds are often attractive for individuals with minimal difference between their pre-tax and after-tax yields, but a desire for high quality credit ratings, low duration, and high yields. Government spending could also be advantageous for TIPS and convertible debt holdings, as the stimulus could drive inflation in the economy, benefiting holders of investments that keep pace with inflation.

As the domestic fixed income investing environment dynamically changes, Weatherly continues to be a stalwart investor for our clients to find securities that boost yields, while maintaining risk/return profiles.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.

Weatherly Asset Management’s Option Strategies

Weatherly Asset Management has the ability to utilize multiple option strategies for our clients, dependent on their individual needs, financial situation and equity holdings. We implement covered call strategies for clients to generate additional income and add to the total return of portfolios. For clients with concentrated stock positions, we mitigate the downside risk with covered put options. We also employ covered collars, at either no cost or minimal cost to the client. Weatherly feels these strategies are valuable when the stock market or a particular equity holding is experiencing high volatility or trading at a range.

Covered Calls – Used to generate additional income for total return of portfolios

- Strategy – An individual writes (sells) a call option contract while at the same time owning an equal amount of shares of the underlying long equity position. The call option contact gives the buyer the right the purchase the shares at a set price and pays the seller a premium for this right.

- How we implement – We looks to generate 3-5% of annualized income premium using this strategy. We analyze positions on a weekly basis and generally write covered call contracts 10-15% above current market prices to allow our clients to enjoy a reasonable level of price appreciation; we write calls on only a portion of the position, so if the option is exercised, the portfolio still holds some of the stock. We use covered call positions to generate income in during periods of market volatility to capture income as prices fluctuate.

- Advantages –

- Call options help generate income in uncertain times

- Clients reap the benefits of owning the equity position (voting rights, dividends) unless the position is called

- Covered calls allow for reasonable stock appreciation while adding cash to the portfolio to implement alternative buying opportunities

- The client has the option of buying back the call option and retaining the shares before the strike price is met

Covered Puts – Used as a protective strategy for concentrated stock positions

- Strategy – An individual purchases a put option while at the same time owning an equal amount of shares of the underlying long equity position. The put contract gives the buyer the right to sell the shares at a set price and pays the seller a premium for this right.

- How we implement – We utilize covered puts as a method of providing protective portfolio insurance for clients with concentrated stock positions. This strategy helps to mitigate the effects of downside momentum and provides protection against loss of total return. We generally employ puts when a client has an unrealized profit accrued from the increase in value of the underlying stock and wants to limit the downside loss from any large decline in the stock price.

- Advantages –

- There is no limit to the gain on the underlying stock

- Upon reaching the expiration date, the client has the option of selling the contract to regain some of the premium paid

- The put option guarantees the right to sell shares at the specified price, no matter how much the underlying stock declines in value

Covered Collars – Used as an alternative to covered puts for additional protection for concentrated stock positions, can be costless or obtained at a minimal cost

- Strategy – An individual writes (sells) a call option while simultaneously purchasing a put option on an equal amount of shares of the underlying long equity position.

- How we implement – We implement covered collar strategies on concentrated stock positions while considering cost basis and holding periods. The collar essentially places a floor on the stock price while simultaneously placing a ceiling on the appreciation, allowing us the ability to manage risk and reduce volatility for clients.

- Advantages –

- There is a limit on the amount of capital gains the client can incur

- The put option allows the client to retain any unrealized accrued gains

- The covered call portion of the collar helps to compensate for the risk of downward price pressure

*Options strategies contain varying degrees of risk. You should carefully consider whether it is appropriate for your situation in light of your experience, objectives and other relevant circumstances.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.