Rekeying Our Financial Data Sheet

Andrea Taylor, CPA, MSA Wealth Management Advisor | Aubrey Brown, CFP®, EA, M.S. Wealth Management Advisor | March 12, 2026

Every year, Weatherly posts an updated Key Financial Data Sheet. While it may appear overwhelming at first glance, it remains one of our most frequently referenced tools as advisors.

In this blog, we provide a fresh look at the 2026 Key Financial Data Sheet and highlight several of the figures that can play an important role in planning this year. As tax laws continue to evolve (including recent changes introduced through the One Big Beautiful Bill) the U.S. tax code has only become more complex. Staying informed on these updates can help investors make more thoughtful decisions.

-

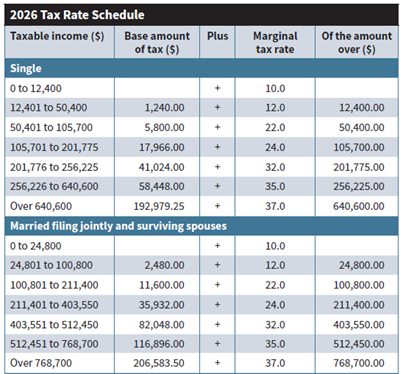

Personal Tax Brackets

Federal Income Tax Brackets make up the bulk of the annual revenue collected by the IRS each year. Determining your filing status and marginal tax bracket is the first step in tax planning. Majority of taxpayers file as Single or Married Filing Jointly (MFJ).

Source: Key Financial Data Sheet 2026

Individuals who are unmarried, have a qualifying dependent, and pay the majority of household expenses may qualify for the Head of Household (HOH) filing status. This status often provides more favorable tax brackets and deductions compared to filing as Single.

Married Filing Separately (MFS) is another option available to married couples. While many couples choose this status to keep finances separate, others may find tax advantages in doing so depending on their circumstances. Although the tax code generally favors joint filers, there are situations where filing separately may help maximize certain deductions or limit liability.

Strategies to Consider

- Roth Conversion – In years when taxable income is lower than usual, converting funds from a traditional IRA to a Roth IRA may allow you to take advantage of lower tax brackets.

- Engage a Tax Professional – A qualified tax professional can help determine the most appropriate filing status and assist with navigating complex tax planning considerations. Here at Weatherly, we often collaborate with our client’s CPAs to evaluate strategies to help manage taxable income such as splitting tax years and charitable giving.

-

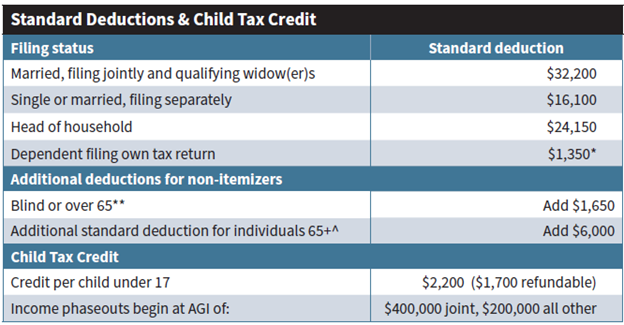

Standard Deductions, Temporary Changes & Child Tax Credits

Each year taxpayers must determine whether to itemize deductions or take the standard deduction. In 2017, The Tax Cuts and Jobs Act nearly doubled the standard deduction and put a limitation of $10K on State and Local Tax (SALT) for those who itemize. Because of this, the majority of American’s have been taking the standard deduction in recent years.

With the 2025 passing of the One Big Beautiful Bill Act, new legislation introduced several temporary changes that may cause more taxpayers to revisit itemizing. One of the most notable updates is the increase to the SALT deduction cap, which has been raised to $40K annually through 2029, subject to income phaseouts.

The bill also includes updates to the Child Tax Credit and introduces an Enhanced Senior Deduction of up to $6,000 for individuals age 65 and older. Similarly, this deduction is scheduled to remain in place through 2028 but phases out at higher income levels.

Source: Key Financial Data Sheet 2026

While many will continue to use the standard deduction, A bunching strategy (particularly around medical expenses and charitable giving) may allow taxpayers to benefit from itemizing in certain years.

Strategies to Consider

- A Donor Advised Fund (DAF) – can be utilized for a tax efficient way to derisk portfolios with flexibility to grant to charities over time. For those itemizing, a tax deduction can also be claimed, but now subject to a 5% AGI Floor.

- Qualified Charitable Distribution (QCD) – may be a great option for those over age 70.5 to give to charity directly from their IRA. The distribution is considered nontaxable and often utilized to help satisfy Required Minimum Distribution (RMD) obligations.

- For those claiming the standard deduction, you can now claim a small deduction for cash gifts directly to qualified 501(c)(3) charities up to $1,000 for single filers or $2,000 for married couples filing jointly.

-

Long-Term Capital Gains and Qualified Dividends

Weatherly’s investment philosophy has an emphasis on long term tax efficiency, particularly within our client’s taxable accounts. Key consideration goes to the federal tax treatment of long-term capital gains and qualified dividends, which generally receive more favorable tax treatment than ordinary income.

For 2026, long-term capital gains tax rates fall between the 0%, 15%, and 20% brackets as shown below based on taxable income.

Source: Key Financial Data Sheet 2026

Strategies to Consider

- Tax Loss Harvesting – As we review and rebalance portfolios throughout the year, we look for opportunities to realize losses that may help offset capital gains. We also review prior year tax returns for any loss carryforwards that can reduce current year gains. For clients in the 15–20% long-term capital gains bracket, this approach can allow us to raise cash for spending needs, reduce concentrated positions, and maintain diversification while helping limit overall tax liability.

- Tax Gain Harvesting – When taxable income falls within the 0% long-term capital gains bracket, investors may be able to sell appreciated assets and realize gains without incurring federal capital gains tax.

-

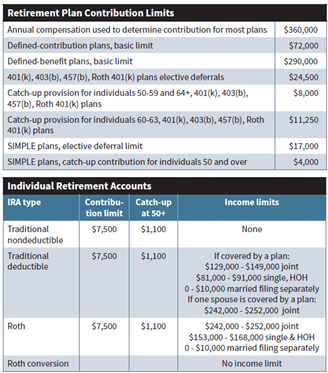

Retirement Contributions

Source: Key Financial Data Sheet 2026

For our clients earning income, strategizing retirement contributions is an effective way to build long term wealth while potentially reducing current taxes. Many taxpayers have access to employer sponsored retirement plans, such as a 401(k), 403(b), or 457 plan. In addition to such plans, individuals may also be eligible to contribute to Traditional or Roth IRAs (depending on their income and other factors).

This time of year, it is important to review annual contribution limits with your advisor to ensure you are taking full advantage of these tax-advantaged opportunities.

Strategies to Consider

- Traditional vs Roth Contributions – For high earners, contributing to a tax deferred retirement plan would allow more money saved given their current high tax bracket. For those in low tax brackets, contributing to a Roth account could limit higher taxes in the future. If you currently have earned income, certain prior year contributions can be made up until the tax return deadlines.

- Self-Employed 401K – Small business owners have an opportunity to significantly increase annual retirement savings through a self-employed 401(k). These accounts allow both employee and employer contributions to maximize retirement contributions year over year. Small differences will go into effect in 2026 for all 401(k) employee contributions- individuals may defer up to $24,500 as the employee, with an additional $8,000 catch-up contribution for those age 50 or older or $11,250 for those 60-63.

-

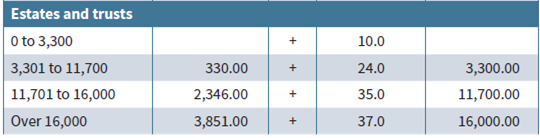

Estates, Trusts and Planning for the Future

Individuals and families often use trusts and estate planning documents as part of a broader strategy to transfer assets to the next generation. While these tools can be powerful, they also introduce additional tax considerations.

It is important to understand how income taxes apply to your specific trusts and estate plan. Certain trusts have compressed tax brackets in comparison to individual tax brackets. In 2026, the top 37% federal tax bracket applies to trusts and estates once income exceeds just $16,000 (vs $768,700 for MFJ in 2026). Intentional planning around trust distributions and asset locations can help reduce unnecessary tax exposure.

Source: Key Financial Data Sheet 2026

While the above tax brackets are a major factor, it is not the only consideration when it comes to wealth transfer. A question we get often- what is the annual gift tax exclusion amount? For 2026, it is $19,000 (the same amount as 2025). This is how much one person may gift to another person without needing to file a gift tax return (Form 709) and reduce their Lifetime Gift Exclusion Amount ($15M). Annual gifting can be a simple yet effective way to gradually transfer wealth to the next generation while reducing the size of a future taxable estate.

Source: Key Financial Data Sheet 2026

In addition to the annual gifting allowance, individuals also have a lifetime estate and gift tax exemption. For 2026, the federal lifetime exemption is $15 million per person. Recent legislation, including provisions discussed in our blog 10 Ways the OBBBA Could Affect You made significant changes to the estate’s exemption landscape. As tax policy evolves, these thresholds will continue to shift, which makes proactive and ongoing planning an important consideration.

How Weatherly Can Help

Given the complexity of today’s tax code, understanding how these numbers apply to your personal financial situation is important. Here at Weatherly, we are here to support you in the journey by regularly reviewing tax returns and financial information to help identify planning opportunities.

Using the updated 2026 Key Financial Data Sheet, we work with clients to evaluate strategies around taxes, retirement contributions, charitable giving, investment management, and estate planning. By combining this data with ongoing conversations about your goals and circumstances, we can help determine which strategies may be most impactful for you.

With the tax deadline approaching and new changes to estate and tax laws, it is a great time to revisit your financial plan, gifting goals, and overall tax strategy. Please reach out to schedule time with your advisor if you would like to review how the 2026 Key Financial Data Sheet may apply to your financial situation in the year ahead.

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.