Giving and Gravy

Aubrey Brown, CFP®, EA, M.S. Wealth Management Advisor | Brooke Boone Kelly, CFP®, MACC, Wealth Management Advisor, Partner | November 21, 2024

November brings colder weather, fantastic food and attention to GIVING. While the centerpiece at the Thanksgiving table may be a gravy dish, the conversations around the table may focus on Giving.

Giving can be categorized in three main areas.

- Thanks – There’s a whole day dedicated to giving thanks, which gives us the opportunity to recognize and reflect on the important things in life. As Weatherly celebrates our 30th anniversary this year, we would like to express a warm “Thank you” to all our clients who make what we do so special.

- Time – Volunteering at charitable organizations is a great way to give back without dishing out money. This act of kindness can be highly personal and can strengthen communities. By year end, our team will have supported 30 local causes- either by volunteering time or philanthropic and industry sponsorships. See some ways WAM has supported areas in need in our Culture & Community page.

- Assets –There’s often a funding shortfall that charities could use to purchase products and services to support their mission. The rest of this blog will focus on strategies for giving financial assets to charity.

When it comes to giving assets, there are several ways to give in a tax advantaged way. Our prior blog – WAM’s Guide to Giving, goes into detail on some of the strategies but we highlighted a few of the most common ways below:

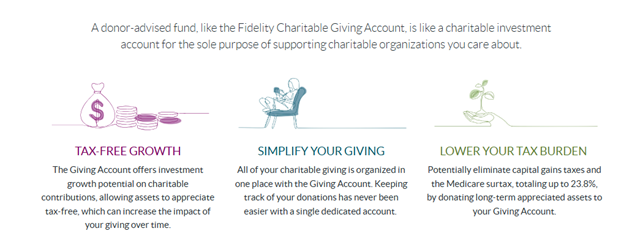

Donor Advised Fund (DAF) – Is a tax efficient charitable account designed to simplify giving to 501c3 organizations on a centralized platform.

Tax Efficiency – Contributions to the fund may be tax deductible in the current year for those who itemize deductions on Schedule A. Furthermore, if contributing long term highly appreciated stock, then the capital gains are eliminated instead of taxable if sold in a brokerage account.

Flexibility – While some donors choose to grant the proceeds in the DAF out to charities immediately, others chose to wait for a future year(s), allowing for tax-free growth.

Simplify – A centralized platform allows quick reference for giving history and makes it easy to track down tax documents for deduction purposes.

Qualified Charitable Distributions (QCD) – allows individuals over the age of 70.5 to send up to $105K (limits for the 2024 calendar year) directly to a qualified charity (or charities) through their IRA. These distributions are not included in taxable income and can be beneficial for those taking Required Minimum Distributions (RMD) and/or claiming the standard deduction.

Estate Planning and Charitable Giving

There are a few strategic ways to leave money to charity as part of an estate plan. One potential option is listing a charity or Donor Advised Fund as a beneficiary to a retirement account. Prior to the SECURE act that passed in 2019, IRAs and other qualified retirement plan beneficiaries that inherited an account could take their mandatory Required Minimum Distributions (RMD) throughout the rest of their life – known as a Stretch (inherited) IRA. Beginning in 2020, the new law states that most non spouse beneficiaries that inherit a retirement account must deplete the account within 10-years. With distributions taxable at your income bracket and consolidated into only 10-years, many individual beneficiaries are pushed into higher tax brackets than before the SECURE act, which may greatly deteriorate the inherited assets. For those who are philanthropic that would like to give money to charity at their death, may consider listing a charity or Donor Advised Fund as a beneficiary to a retirement account rather than in a trust or other nonretirement account. Charities pay no income tax so 100% of the IRA value is retained by charity. Individuals that have nonretirement assets like a living trust, may consider listing human beneficiaries rather than charities given the potential step up in cost basis at death. The beneficiaries would benefit from a tax perspective receiving these assets instead of an IRA.

Those who wish to set aside larger sums of money for charities, may consider using a charitable trust as a planning tool. While this requires some upfront costs and an attorney, a charitable trust can provide a current year tax deduction, fulfil charitable intentions and remove assets from a taxable estate. Two of the more common charitable trusts are Charitable Remainder Trust (CRT) and Charitable Lead Trust (CLT). While both these types of trusts benefit charities in some form, we see CRTs as a popular option when interest rates are higher as it can generate a higher current deduction than CLTs. A Charitable trust strategy pairs well in a high-income year, such as a sale of a business or home. We also see opportunities in CRTs for those with concentrated securities that have a large taxable estate but would like to retain an income stream during their lifetime. Unless the Tax Cuts and Jobs Act (TCJA) receives an extension under the new administration, we may see an uptick in CRTs with a lower estate exemption amount starting in 2026.

Giving Together

While a lot of the strategies around giving focuses on individuals, we have seen an emergence of family giving. This allows families to support organizations that they believe in together while also exposing the next generation to philanthropy. Some families choose to allocate a dollar amount to each family member and a DAF can help streamline the process. Programs like Fidelity’s Gift4Giving, makes it easy for others to participate giving from your DAF even from afar. Family philanthropy is a great way to keep the family connected and involved in the community.

In Summary –

Thanksgiving brings to light the importance of giving in a number of areas. While giving is a year-round activity, Giving Tuesday on December 3rd 2024 gives donors an opportunity to support charities and satisfy their gifting before the end of the year.

Our team of advisors are here to explore which giving strategy may be most appropriate for your philanthropic goals.

Wishing you and yours a Happy Thanksgiving!

** The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.