Capitalizing On a New Year: 2026 Planning Opportunities

Stone Churby, CFP®, M.S.F. Wealth Management Associate | Brooke Boone Kelly, CFP®, MACC Wealth Management Advisor, Partner | February 12, 2026

The start of a new year gives individuals and businesses the opportunity for a good health check-up on their financial situation and to strategize for the year ahead. Cash flow needs, gifting strategies, philanthropic goals, estate plans and asset allocation may need to be updated depending on your financial needs and long-term planning goals. Additionally, with the new One Big Beautiful Bill Act (OBBBA) tax bill, this year offers a litany of legislative changes that may positively impact taxpayers. In this blog post, we explore the various planning opportunities 2026 has to offer.

Cash Flow Projection and Analysis

The first quarter of the new year is an ideal time to review ongoing cash flow needs and any new or one-time expenses. A cash flow projection, or mapping out income sources versus cash needs, can help evaluate any cash surplus or cash shortfall. It is important to identify any changes in recurring costs, like healthcare premiums, to ensure that the cash flow and withdrawals currently in place are sufficient for your lifestyle. Beyond recurring costs, it is also helpful to identify large, one-off expenses as early as possible. Whether it’s a vacation, remodel, life event, or a healthcare expense; eliminating as much of the surprise as possible may help mitigate the financial burden and capitalize on planning opportunities.

Your age and tax bracket may help dictate where funds are withdrawn from. Financial planning can help identify pre- and post-retirement strategies for saving and spending. The “gap years” of retirement, or years between retirement and the start of various retirement income sources, such as Social Security or Required Minimum Distributions (RMDs), may result in inconsistent income. RMDs, Social Security, pensions, and annuity payments may offer different starting points, pushing income up and down throughout the early stages of retirement. Roth conversions may make sense for individuals in a low tax year before fixed retirement income starts.

- Taxable accounts are often most flexible, given no age restrictions for withdrawal. Capital gains are taxed at a more favorable federal rate and can help bridge income gaps or cover larger one-time expenses.

- Tax-deferred accounts typically require minimum distributions starting at age 73. Individuals over the age of 59 ½ can avoid early withdrawal penalties on IRAs, 401(k)s, and 403(b) plans, however withdrawals are taxed at ordinary income rates.

- Certain IRAs allow for donations direct to charity via Qualified Charitable Distributions (QCDs) after age 70 ½. For philanthropic individuals, preserving funds in eligible IRAs until later in the tax year can give donors the opportunity to give via QCDs.

- Tax-free accounts such as Roth IRAs and Roth 401(k)s can be utilized in higher income tax years or as potential insurance for unforeseen expenses.

Asset Allocation Review

Asset allocation is the main driver of long-term investment performance. Another year passing offers an opportunity to check on the risk profile and asset allocation of your investment portfolio versus cash needs and your long-term financial plan. As time passes, the asset allocation of your portfolio may be adjusted, providing predictable streams of income during retirement.

The S&P 500 had an annualized returns above 20% from 2023-2025 (compared to the ~10% annualized, 100-year performance). This rapid market appreciation may have caused an overallocation to equities and specific companies within that sleeve. The start of a new tax year creates an opportunity to reduce overallocation to equities and single stock concentration across your portfolio.

Gifting to Next Generation and Philanthropy

Highly appreciated assets also create an opportunity to potentially gift stock or cash to the next generation and/or charities. For gifts to the next generation, the 2026 annual gift tax exclusion is $19,000 per person. Gifting appreciated securities to the next generation allows you to remove capital gains from your portfolio and estate while giving the recipient an opportunity to possess a growing asset.

We highlight philanthropic giving in the next section as there are some new charitable provisions for 2026 tax year.

2026 Strategies under the One Big Beautiful Bill Act (OBBBA)

The One Big Beautiful Bill Act (OBBBA) tax bill passed on 7/4/2025 offers some unique planning opportunities. Below, we highlight a few key OBBBA provisions that became effective in 2026 and strategies to consider this year.

Please reference our 2026 Key Data Chart with updated figures for this tax year.

Standard Deduction Versus Itemized Deduction

The OBBBA permanently coded the larger standard deduction that was introduced in the 2017 Tax Cut and Jobs Act (TCJA). With the larger standard deduction, as many as 90% of taxpayers will utilize the standard deduction over itemized deductions.

Charitable Provisions

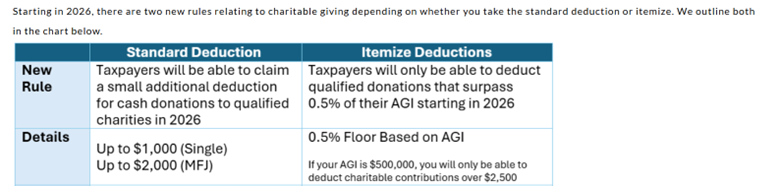

Depending on whether a taxpayer takes the standard deduction or itemizes, there are a few unique charitable planning provisions that begin in 2026. Please reference the following chart from our OBBBA blog post:

For taxpayers who itemize, consider bunching a few years’ worth of appreciated stock donations in one tax year. This can help get donors over the 0.5% floor and potentially reduce equity allocation and concentration in taxable accounts.

For individuals who take the standard deduction, consider making cash donations direct to eligible charities. Please note cash donations to Donor Advised Funds (DAFs) and foundations do not qualify for the additional deduction outlined in the chart above.

Additionally, for those 70 ½ and older, a Qualified Charitable Distribution (QCD) strategy allows individuals to donate up to $111,000 directly from their IRA to a charitable organization. The donation is excluded from Adjusted Gross Income (AGI) and can potentially put individuals into a lower tax bracket.

State and Local Taxes (SALT)

For taxpayers who itemize and qualify with the income phaseouts, the State and Local Tax (SALT) deduction has been temporarily increased from $10,000 to $40,400 in 2026, set to sunset in 2029. For individuals who can itemize, be aware of income phaseouts and when possible, consider deferring taxable income to maximize the SALT deduction.

529 Accounts

Starting in 2026, the withdrawal limit for Kindergarten- 12th grade doubled from $10k to $20k per year for qualified education expenses under Federal law. Please check your state laws for 529 qualified expense withdrawal rules. The OBBBA also made 529 accounts much more flexible and broader with qualified expenses. Unused funds can be utilized for other beneficiaries or potentially rolled to a Roth IRA.

Trump Accounts

Parents or guardians with eligible children born between 2025-2028 can elect to open Trump accounts via Form 4547 when filing their 2025 Tax Return or online. The $1,000 government seed money is expected to be deposited in July 2026.

Health Savings Accounts (HSAs)

As of 1/1/2026, Bronze and Catastrophic Affordable Care Act (ACA) plans are now HSA eligible accounts even if they do not meet the formal definition of a High-Deductible Health Plan. This change may create a unique opportunity for more individuals to save in HSA accounts and maximize triple tax benefits.

Taxpayers who itemize and are in the 37% income tax bracket will be limited to 35 cents on the dollar for their deductions starting in 2026 tax year.

Alternative Minimum Tax (AMT)

The AMT phaseout limits reverted to 2018 levels starting in 2026.

Qualified Business Income (QBI)

The 20% Qualified Business Income (QBI) deduction was made permanent under OBBBA. The QBI codification allows eligible self-employed and small-business owners to claim an income deduction from a qualified trade or business (up to 20%). In 2026, the income phase out limit increased from 2025.

Other changes under the OBBBA are explored in more detail in our previous OBBBA Blog.

Estate Plan Check Up

A new year always presents an opportunity to review your estate plan and beneficiary elections. We urge clients to check how their real estate assets are titled through their local county recorder or assessor’s office. Life changes may also create the need for beneficiary updates or a trust review.

Building upon the direction of assets, there are four key estate plan documents that most adults should have, including: a revocable living trust, will, power of attorney (POA), and advanced health care directive (ACHD).

How WAM Can Help

The Weatherly team welcomes the opportunity to connect and capitalize on 2026 planning opportunities, such as cash flow projections and analysis, asset allocation review, gifting to next generation and philanthropy, 2026 strategies under the One Big Beautiful Bill Act (OBBBA) and estate plan checkup.

As tax season approaches, Weatherly is also happy to coordinate document exchanges with your tax professional. Please reach out to our team to coordinate.

*Disclosures:* The information provided should not be interpreted as a recommendation, no aspects of your individual financial situation were considered. Always consult a financial professional before implementing any strategies derived from the information above.