Business Exit Planning: A Strategic Guide for Business Owners

Marty Rascon, CFA, Wealth Management Associate Advisor | Stone Churby, CFP®, M.S.F. Wealth Management Associate Advisor | June 11, 2026

For many business owners, a company is more than a source of income—it often represents much of their wealth and financial future.

Yet after years of effort and sacrifice, many owners are still unprepared for the day they step away. Whether the goal is retirement, a new venture, or realizing the value of years of hard work, exiting without a plan can be costly—in money, legacy, and peace of mind.

Exit planning also matters when life takes an unexpected turn. Death, disability, or market disruption can leave a business vulnerable if succession roles, key decisions, and financial contingencies have not been addressed in advance. A clear plan can help protect the business, support employees and family, and preserve value during uncertain times.

A thoughtful exit strategy turns a last-minute scramble into a deliberate transition. In this blog, we’ll cover how to build the right advisory team, key questions to ask, common exit strategies, and financial considerations for life after the sale or transition.

Assemble a Team:

Before you build an exit plan, start by assembling the right advisory team.  Exit planning touches multiple disciplines—including financial planning, tax strategy, legal structures, business valuation, and transaction execution—so it is rarely something one professional can manage alone. A coordinated team helps you protect the value you have built and make better informed decisions throughout the process.

Exit planning touches multiple disciplines—including financial planning, tax strategy, legal structures, business valuation, and transaction execution—so it is rarely something one professional can manage alone. A coordinated team helps you protect the value you have built and make better informed decisions throughout the process.

Core Advisor Roles

- Wealth Manager: A wealth management professional often serves as the central coordinator of the exit-planning process. They take a holistic view of both business and personal financial goals, act as a fiduciary in your best interests, and help ensure the strategy stays aligned with your broader objectives.

- CPA or Tax Advisor: Tax consequences can vary significantly depending on how an exit is structured. A skilled CPA or tax advisor helps evaluate those consequences, identify planning opportunities, and reduce the risk of unnecessary taxes.

- Certified Business Valuator: Before a transaction can move forward, you typically need an independent, defensible assessment of fair market value. A valuation provides a realistic pricing baseline, highlights strengths and weaknesses from a buyer’s perspective, and may be required for certain transactions, such as an ESOP.

- Investment Banker/Business Broker: A broker or transaction specialist can help execute the sale process. These professionals identify and qualify potential buyers, market the business confidentially, and support negotiations on your behalf.

- Legal Counsel: An attorney with business transaction experience can draft and review key documents, including letters of intent and purchase agreements, while helping protect your interests throughout the deal. They can also ensure that your business interest is represented in your personal estate planning documents.

The strongest exits are not just well timed—they are well coordinated. Each advisor plays a distinct role, and bringing the right people together early can help you avoid costly mistakes, communicate more effectively, and move through the transition with greater confidence. As you assemble your team, it is also worth stepping back to clarify what you want from the exit itself. That reflection lays out the groundwork for the key questions and decisions that follow.

Business Owner Considerations:

A successful exit strategy is the result of deliberate preparation. Before choosing a specific strategy, every business owner needs to take stock and lay the right groundwork. Some of the key elements and considerations of a successful exit strategy include:

- Know Your Stakeholders: A business exit affects more than just the owner. Partners, family members, employees, customers, and other key stakeholders may all be impacted by what happens next. Taking time to consider each group’s perspective can help you anticipate concerns, communicate more effectively, and make better-informed decisions throughout the transition.

- Get Your Finances in Order: A well-prepared financial record is essential to a smooth exit process and a credible business valuation. In most cases, buyers and valuation professionals will want to review at least three to five years of financial statements, though the exact requirements may vary. Keeping these records accurate, complete, and well organized can strengthen buyer confidence, support a more efficient diligence process, and help maximize the value of your business.

- Set Personal Goals: Before choosing an exit strategy, define what a successful outcome looks like for you personally and financially. Start by identifying your income needs, ideal timeline, and the role—if any—you want to play after the transition. You should also consider what matters most in the long term. For example, do you want a quick sale and immediate liquidity, or would you prefer to stay involved in an advisory capacity? Are you seeking an outright sale to a third party, or is preserving a family legacy more important? Because every business exit is unique, answering these questions can help clarify your priorities and shape a strategy that aligns with your goals.

- Set a Timeline: A successful exit rarely happens overnight. Establishing a realistic timeline—often three to five years—gives you time to prepare the business for transition, strengthen weak areas, and make decisions with intention. A clear timeline also helps you break the process into manageable milestones, for example:

-

- Year 1: Organize financial records, obtain a business valuation, and identify operational weaknesses.

- Years 2–3: Address gaps, reduce owner dependence by building management independence, and assemble a team of professional advisors.

- Year 4: Begin marketing the business or start implementing the transition plan if the exit will be internal.

- Year 5: Execute the exit.

Although a timeline provides a useful structure, it should not be overly rigid. Personal circumstances can change, and economic or market conditions may shift over time. Building some flexibility into your plan can help you adapt as needed without losing sight of your broader exit goals.

Working through these considerations helps create a clear framework for your personal goals, financial priorities, and long-term aspirations. Once you have assessed the broader picture of your exit, the next step is to understand the range of strategies available and determine which approach best aligns with those objectives.

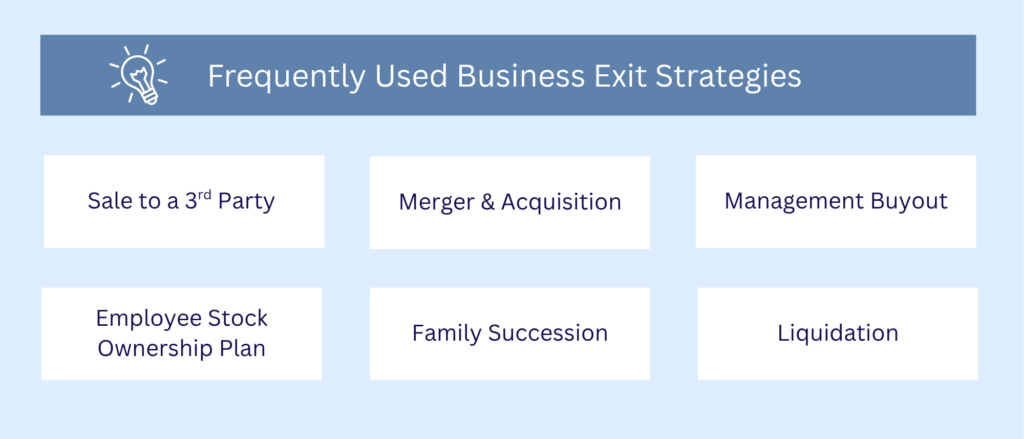

Types of Exit Strategies:

Business owners have several exit strategies to consider, and the right choice depends on both the structure of the business and the owner’s personal goals. While the most common options share a few broad themes, each can be tailored in different ways depending on the company’s circumstances, timeline, and priorities. The section below outlines several of the most frequently used approaches.

- Sale to a 3rd Party: A third-party sale is one of the most common and straightforward exit strategies for business owners. In this approach, the business is sold to an outside buyer, such as a competitor, private equity firm, or individual investor. It is often appealing to owners who want a relatively clean break and quicker access to liquidity. Maximizing sale price and profit is also a key driver to sell to a 3rd party.

- Merger & Acquisition (M&A): An M&A deal may look similar to a third-party sale, but the buyer’s goals are usually more strategic. Acquirers often seek synergies, greater market share, a stronger customer base, or valuable assets such as technology, intellectual property, or specialized expertise. Because of these benefits, M&A transactions can command higher valuations in the right circumstances. For example, a larger firm may acquire a smaller business to add a complementary product line or enter a new market.

- Management Buyout (MBO): In a management buyout, the existing management team or employees purchase the business from the owner. This option can appeal to owners who want continuity in leadership, operations, and company culture, since the buyers already understand how the business runs. Transactions are often financed through a mix of outside funding and seller-supported terms, though the exact structure can vary. In some cases, the owner may also remain involved for a period of time in a limited role, such as serving as an advisor or retaining a small ownership stake.

- Employee Stock Ownership Plan (ESOP): An ESOP allows a business owner to sell all or part of the company to employees through a trust structure. Depending on how the plan is designed, it can provide either immediate liquidity or a gradual transition over several years. Because employees earn ownership interests over time, an ESOP can also support retention and help align the team with the company’s long-term growth. In some cases, the business structure may create potential tax advantages, but these plans can be complex to establish and administer. For that reason, owners should work closely with qualified professionals—such as a CPA, attorney, or transaction advisor—before moving forward.

- Family Succession: Family succession transfers ownership to one or more relatives, such as children, siblings, nieces, or nephews. It appeals to owners who want to preserve a family legacy and keep the business under familiar leadership. A successful transition usually requires identifying the successor early, obtaining an independent valuation, and selecting the right transfer structure—such as a sale, gift, or installment sale. In some cases, more advanced tools like Family Limited Partnerships (FLPs) or Self-Cancelling Installment Notes (SCINs) may be worth exploring with professional guidance. Even within a family, the transition should be handled formally and documented carefully to reduce the risk of misunderstandings or future conflict.

- Liquidation: Liquidation is typically considered a last resort exit strategy. In this approach, the owner winds down the business, sells its assets, and uses the proceeds to satisfy outstanding liabilities. It is most often used when there is no clear successor, no viable outside buyer, or the business is no longer sustainable as an ongoing operation.

Each of these exit strategies offers a different mix of liquidity, control, timing, tax consequences, and business continuity. The right path depends not only on the business itself, but also on what you want your life to look like after the transition. A sale, succession plan, or gradual handoff can reshape your income, responsibilities, family priorities, and long-term financial plan. With that in mind, choosing an exit strategy is also the beginning of a broader conversation about how the value you have built can support your next chapter.

Life After the Sale: Planning for the Next Chapter

After the sale closes, many owners expect the hardest part to be over. In reality, the next phase can be just as important. A business sale often turns years of illiquid business value into a large, concentrated pool of cash, marketable securities, seller notes, or structured equity compensation.

After the sale closes, many owners expect the hardest part to be over. In reality, the next phase can be just as important. A business sale often turns years of illiquid business value into a large, concentrated pool of cash, marketable securities, seller notes, or structured equity compensation.

That shift can create several new planning priorities at once, including:

- Tax planning to manage the impact of the sale and future income.

- Investment decisions about how to reinvest or allocate proceeds.

- Retirement income planning to determine how much can be spent sustainably.

- Estate and legacy planning to reflect family priorities and long-term wishes.

- Lifestyle and risk management decisions involving debt, healthcare costs, and future financial needs.

These are not small decisions, and many need to be addressed at the same time. This is where a wealth manager can add value. By taking a broad view of your finances, a wealth management team can help connect the business transition to your larger personal goals, including retirement income, investment strategy, risk management, family priorities, and legacy planning. Rather than treating the sale as a stand-alone transaction, they can help you build a coordinated plan for what comes next so the value you created in the business supports lasting financial independence and a confident next chapter.

How Weatherly Can Help:

Weatherly has a strong history of working with small business owners as they transition from active owners to retirement. Our team understands and has direct experience with individuals who are looking to start building an exit plan, have executed their exit, and are now enjoying their retirement. Often the conversation about selling a business starts with us. Our team also understands that your business exit is not an isolated event and is here to help craft a roadmap for financial success into your retirement years.

** The information provided should not be interpreted as a recommendation; no aspects of your individual financial situation were considered. Weatherly is a registered investment advisor and does not provide legal advice. Always consult your trusted financial and legal professionals before implementing any strategies derived from the information above. This blog was developed with the assistance of artificial intelligence (“AI”) tools. These tools were used to help generate initial outlines, organize ideas, and improve efficiency in communication and grammar.